Basically, a participating whole life insurance policy is designed to provide you with financial protection for life. Additionally, a whole life insurance policy accumulates a cash value that is set to grow over time. Given that lifelong insurance protection, it appeals to consumers who require financial protection for as long as they live. With this in mind, let’s learn the basics of a participating whole life insurance policy in this post.

Table of Contents:

- Participating Plan

- Insurance Coverage

- Insurance Policy Cash Value

- Insurance Premium

- Participating Whole Life Insurance Policy Features

- Conclusion

One Minute Summary:

- On the whole, the insurance premium in a participating whole life insurance policy is invested into the insurer’s participating fund.

- Thereafter, the participating fund is responsible to meet the insurance policy’s financial obligations, e.g. to issue a claim payout, to generate a return for its policyholders and shareholders.

- As a participating plan, your insurance policy will accumulate a policy cash value over time.

- Given that the insurance premium has to serve multiple needs, a participating whole life insurance policy tends to have a higher Cost to Benefit Ratio (as compared to a term insurance policy).

- Similarly, the absolute cost of a participating whole life insurance policy is likely more expensive than a term insurance policy.

Part 1: Participating Plan

Generally, most whole life insurance policies are participating plans. To explain, in a participating plan, you will participate or share in the profits of the insurer’s participating fund. In the same way, you will also share the participating fund’s risks. For this purpose, the insurer will pool your insurance premium together with the rest of the policyholders. Thereafter, the insurer will invest this pool of money into its participating fund. All in all, the participating fund is responsible to meet its financial obligations, e.g.

- To generate a stable return in the medium to long-term;

- Issue a payout for insurance claims and to meet expenses.

Part 2: Insurance Coverage

Part 2.1: Scope of Insurance Coverage

Presently, most participating whole life insurance policies provide a basic life cover. To this end, in the event of pre-mature death, the insurer will issue the death benefit to either your beneficiaries or your estate (depends on whether you have made an insurance nomination). Additionally, some of these whole life insurance policies include insurance coverage for Total & Permanent Disability as part of its standard insurance coverage. Accordingly, in the event of Total & Permanent Disability (“TPD”), the insurer will issue the TPD payout out to you. Furthermore, most participating whole life insurance policies allow you to attach optional supplementary benefits. For example, you may include insurance coverage for (Major) Critical Illness, and/or Early Critical Illness.

Summing up, the more benefits you add to the life insurance policy, the costlier it becomes. Similarly, the higher the insured amount for the insurance benefit, the higher the cost of insurance. Under those circumstances, you will pay a higher rate of insurance premium.

Part 2.2: Insurance Coverage Amount

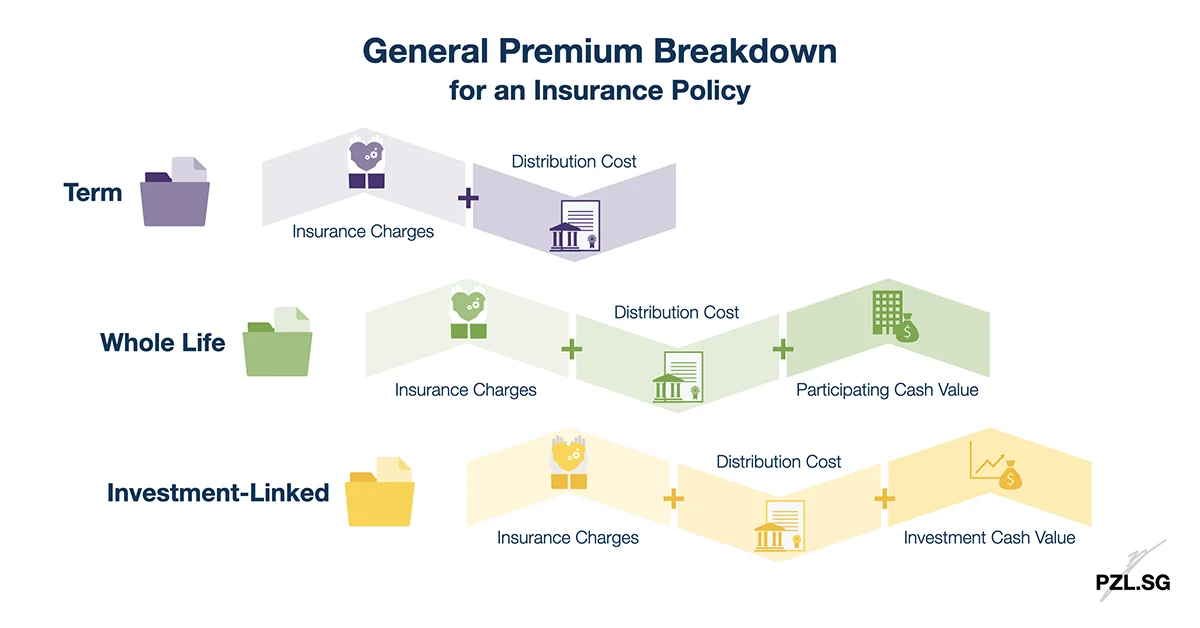

When you compare a participating whole life insurance policy against a term insurance policy, the former tends to have a higher Cost to Benefit Ratio. This is because its insurance premium needs to cater to both the insurance charges and the insurance policy’s cash value. As a result, a higher Cost to Benefit Ratio suggests that you are paying a higher cost for the benefits that you receive from the life insurance policy.

Part 2.3: Insurance Coverage Period

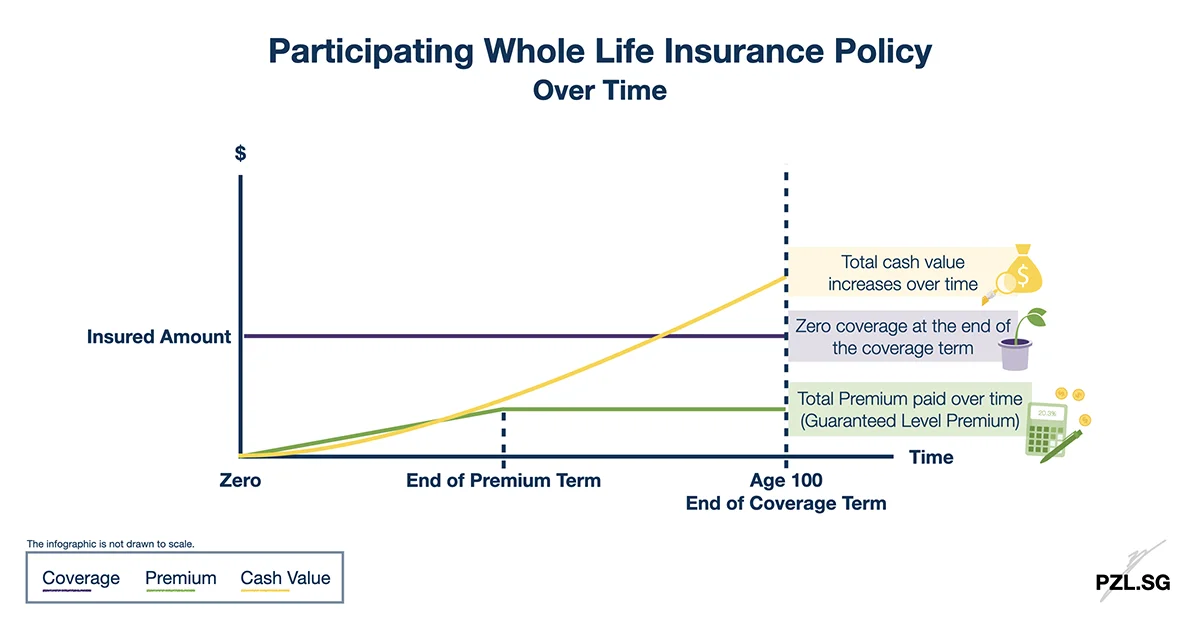

All in all, a participating whole life insurance policy is designed to cover you for life. Although this may be true, not all the insurers define “whole life” the same way. To point out, there are some whole life insurance policies that cover you till age 100 only. In this situation, upon the policy anniversary following your 100th birthday, the insurer will pay both the basic insured amount and the accumulated bonuses out to you.

By comparison, there are also whole life insurance policies that cover you for as long as you live. To clarify, even if you live beyond age 100, the whole life insurance policy will continue to cover you. In this case, your beneficiaries or your estate will receive the death benefit when you pass away.

Part 3: Insurance Policy Cash Value

As I have noted earlier (in Part 1), as a participating plan, your insurance premium is pooled together with the rest of the policyholders. Thereafter, the insurer will invest this pool of money into its participating fund. In time to come, the participating fund will generate a return and distribute a portion of this return out to you. By and large, there are two components to the return that you may receive from the participating fund.

Firstly, the participating fund will issue the guaranteed benefit as shown in the policy illustration. For the most part, regardless of the prevailing market condition or the participating fund’s experience, the insurer is obligated to distribute the guaranteed component of the policy cash value out to you.

Secondly, the insurer may also declare non-guaranteed bonuses. In general, this comes in the form of the reversionary bonus and the terminal bonus. Since this is a non-guaranteed component, the insurer is not obligated to distribute the bonuses out to you. Instead, the distribution will depend on the participating fund’s experience each year. Summing up, both the guaranteed and the non-guaranteed benefits form the total surrender value that you can see in the policy illustration table.

Next, although the entire insurance premium is invested into the insurer’s participating fund, not every dollar (that is put in) will generate a policy cash value out to you. For instance, let’s look at the additional insurance premium that you pay for the Critical Illness supplementary benefit. In this case, the critical illness insurance premium will still contribute to the insurer’s participating fund. In due time, the participating fund will generate a return out of this insurance premium. However, this return is used to cover the cost of any Critical Illness claims. Consequently, it will not be paid out to the policyholder in the form of a policy cash value.

Part 4: Insurance Premium

Part 4.1: Insurance Premium Rate

To sum up, the absolute cost of a participating whole life insurance policy is likely more expensive than a term insurance policy. This is because the insurance premium is used to serve multiple purposes; i.e. pay for both financial protection and to accumulate a policy cash value. In addition, a part of the insurance premium is also used to pay for the insurance policy’s distribution cost.

Part 4.2: Insurance Cost Structure

Next, let’s look at the insurance cost structure for a participating whole life insurance policy. In general, for the death benefit, the cost of insurance is usually guaranteed throughout the insurance policy’s premium paying period. To put it another way, you will pay the same amount of money to the insurer each year. For example, let’s assume that a whole life insurance policy costs $3,000 annually. In this situation, the insurance premium will remain at $3,000 annually throughout the entire premium paying period.

By comparison, for the supplementary benefits, e.g. the critical illness benefit, the cost of insurance is usually non-guaranteed. Consequently, the insurer may revise the insurance premium rate based on the future experience, and according to Singapore’s laws and regulations. Although the insurer may revise the insurance premium rate in the subsequent years, such adjustments shall not be made on an individual basis. Overall, these adjustments will be made to all its policyholders.

Part 4.3: Insurance Premium Paying Period

In general, most participating whole life insurance policies have a limited payment period feature. Accordingly, you may choose to limit the number of years that you pay for the insurance premium. For example, let’s take the case of a 30 year old life insured. In this case, he can opt to pay the insurance premium over 20 years (i.e. till age 50) while staying covered for life.

Next, if you have included any supplementary benefits, then the insurance premium paying period for these benefits shall follow the basic life insurance policy.

Part 5: Participating Whole Life Insurance Policy Features

At this time, there are many types of whole life insurance policy on the market. In detail, each of these insurance policies may have a different policy structure and feature. Despite that, let’s look at two of the most common features that you can find in most of the participating whole life insurance policies.

Part 5.1: Insurance Policy Loan

Firstly, you can choose to take up an insurance policy loan and borrow money from your participating whole life insurance policy. For this purpose, you may do so via either a voluntary policy loan or an automatic policy loan. In brief, for a voluntary policy loan, you can withdraw a percentage of the insurance policy’s net surrender value. In contrast, for an automatic policy loan (“APL”), the insurer will withdraw the insurance premium that is due from the insurance policy’s cash value.

Part 5.2: Option to Purchase Additional Insurance Benefit (“OPAI”)

Basically, the option to purchase additional insurance benefit allows you to purchase a new whole life insurance policy or an endowment savings plan. For this purpose, you do not have to undergo any medical underwriting. Therefore, you can be sure to increase your insurance coverage without any proof of your present health. Generally, in order to exercise this option, you will need to undergo a life’s major event, e.g. a change in marital status, or the birth of your child.

Part 6: Conclusion

All in all, a participating whole life insurance policy provides you with an assurance for life. For the most part, such financial protection comes in handy during your retirement years when you are no longer earning an income. Moreover, your insurance policy will also acquire a policy cash value – one that you can probably tap into to meet your financial needs.

First Published: 18 September 2019

Last Updated: 25 June 2024

Leave a Reply