Up to the present time, there is still a constant debate on term vs whole life insurance policy in Singapore. For the most part, we want to pay as little as we can for the insurance premium. At the same time, we want to get as much insurance coverage as we need from the life insurance policy. Moreover, we also want to be insured for probably as long as we live. With this intention in mind, let’s conduct a comparison on term vs whole life insurance to determine which type of life insurance policy is more suitable for you.

Table of Contents:

- Type of Life Insurance Policy

- Insurance Coverage

- Insurance Policy Cash Value

- Insurance Premium

- Conclusion on Term vs Whole Life Insurance

One Minute Summary:

- Generally, a term insurance policy is a non-participating plan while a participating whole life insurance policy is a participating plan.

- On the whole, both types of life insurance policy will provide a basic life cover for you. In addition, you can also include supplementary benefits such as insurance coverage for Total & Permanent Disability, (Major) Critical Illness, and Early Critical Illness.

- Assuming all other factors equal, a participating whole life insurance policy tends to have a higher Cost to Benefit Ratio as compared to a term insurance policy.

- By and large, most term insurance policies are not designed to cover you for life. In contrast, a participating whole life insurance policy tends to cover you for as long as you live.

- To point out a term insurance policy does not have any cash value. By comparison, a participating whole life insurance policy will accumulate a policy cash value over time.

- Summing up, the absolute cost of a term insurance policy is likely cheaper than a participating whole life insurance policy.

- Generally, a participating whole life insurance policy allows you shorten your insurance premium paying period. However, a term insurance policy may not have such a policy feature.

Part 1: Type of Life Insurance Policy

Generally, a term insurance policy is a non-participating plan. Accordingly, you will not participate or share in the profits of the insurer’s participating fund.

On the other hand, most whole life insurance policies are participating plans. To explain, in a participating plan, you will participate or share in the profits of the insurer’s participating fund. In the same way, you will also share the participating fund’s risks. For this purpose, the insurer will pool your insurance premium together with the rest of the policyholders. Thereafter, the insurer will invest this pool of money into its participating fund. All in all, the participating fund is responsible to meet its financial obligations, e.g.

- To generate a stable return in the medium to long-term;

- Issue a payout for insurance claims and to meet expenses.

Part 2: Insurance Coverage

Part 2.1: Scope of Insurance Coverage

As a life insurance policy, both term and whole life insurance policies will usually provide a basic life cover. To this end, in the event of pre-mature death, the insurer will issue the death benefit to either your beneficiaries or your estate (depends on whether you have made an insurance nomination). Additionally, both types of life insurance policy allow you to attach optional supplementary benefits. For example, you may include insurance coverage for Total & Permanent Disability, (Major) Critical Illness, and/or Early Critical Illness.

Summing up, in both cases, the more benefits you add to the life insurance policy, the costlier it becomes. Similarly, the higher the insured amount for the insurance benefit, the higher the cost of insurance. Under those circumstances, you will pay a higher rate of insurance premium.

Meanwhile, for a term insurance policy, there are also plans that are designed to provide a specific set of insurance coverage. For example, a multi-pay Critical Illness insurance policy focuses on financial protection for multiple critical illness conditions. To this end, these term insurance policies may not provide a death benefit.

With this in mind, when you look at term vs whole life insurance, both types of life insurance policy are able to provide insurance coverage for your financial needs. However, their differences lie in the other aspects, e.g. insurance coverage amount. All in all, I will cover each of these aspects in the following sections.

Part 2.2: Insurance Coverage Amount

Assuming all other factors equal, a participating whole life insurance policy tends to have a higher Cost to Benefit Ratio as compared to a term insurance policy. This is because in a term insurance policy, the majority of the insurance premium is used to pay for the insurance charges. In contrast, for a participating whole life insurance policy, the insurance premium needs to cater to both the insurance charges and the insurance policy’s cash value. As a result, a higher Cost to Benefit Ratio suggests that you will pay a higher cost for the benefits that you receive from the life insurance policy.

With this in mind, when you look at term vs whole life insurance, you need to determine the purpose of your life insurance policy. In detail, are you purchasing a life insurance policy to meet your protection needs? Or do you prefer your life insurance policy to serve as many purposes as possible?

Part 2.3: Insurance Coverage Period

As a matter of fact, most term insurance policies are not designed to cover you for life. Instead, it has a fixed insurance coverage period, e.g. till you reach 65 years old. At the end of the insurance coverage period, the term insurance policy will terminate.

By comparison, a participating whole life insurance policy is designed to cover you for life. Although this may be true, not all the insurers define “whole life” the same way. To point out, there are some whole life insurance policies that cover you till age 100 only. In this situation, upon the policy anniversary following your 100th birthday, the insurer will pay both the basic insured amount and the accumulated bonuses out to you.

With this in mind, when you look at term vs whole life insurance, you need to determine the time period when you need to rely on life insurance for financial protection. Generally, this period is the time when you don’t have sufficient assets to meet your financial needs. After you have accumulated sufficient assets, you may not need rely on a life insurance policy to provide the financial leverage anymore.

Part 3: Insurance Policy Cash Value

To point out, a term insurance policy does not have any policy cash value. As a result, you won’t be able to withdraw any monies out from the term insurance policy. In like manner, there is also no surrender value when you terminate a term insurance policy. To that end, you will only receive a policy payout when a covered event is triggered, e.g. death.

On the other hand, a whole life insurance policy is usually a participating plan. Consequently, your insurance premium is pooled together with the rest of the policyholders. Thereafter, the insurer will invest this pool of money into its participating fund. And in time to come, the participating fund will generate a return and distribute a portion of this return out to you. Summing up, there are two components to the return that you may receive from the participating fund; that is, the guaranteed benefit and the non-guaranteed bonuses.

With this in mind, here are three questions to ask when you look at term vs whole life insurance. Firstly, is your primary objective to seek financial protection? Next, are you willing to compromise on the amount of insurance coverage so that your life insurance policy is able to acquire a policy cash value? And finally, are there any better financial instruments that are capable to generate a similar rate of return for you?

Part 4: Insurance Premium

Part 4.1: Insurance Premium Rate

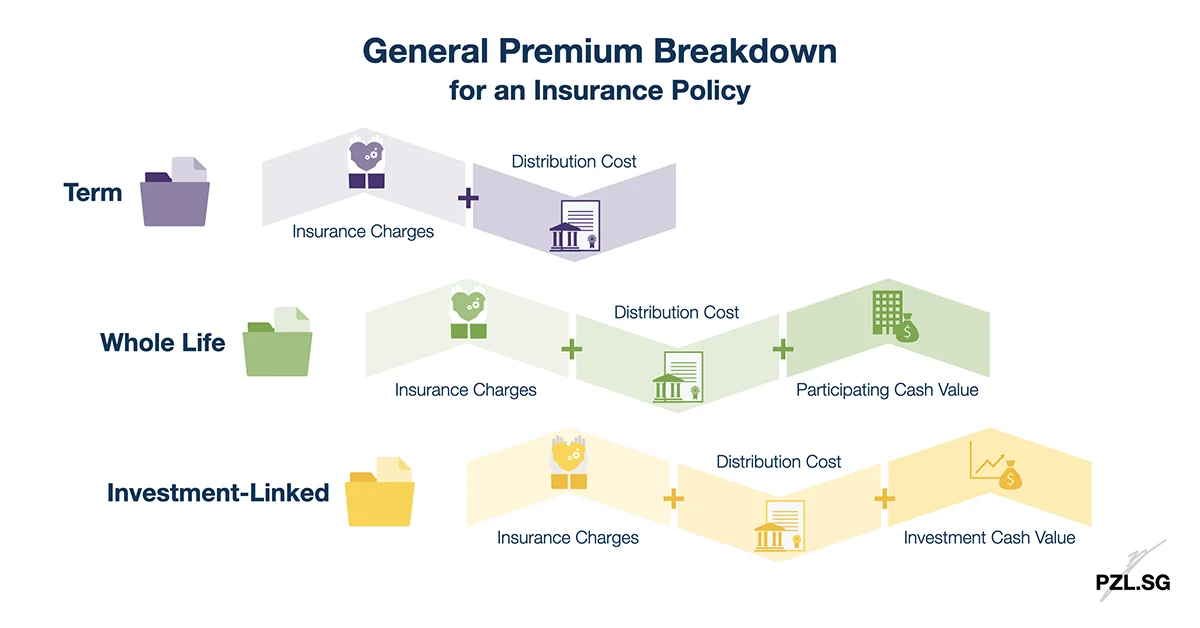

To sum up, the absolute cost of a term insurance policy is likely cheaper than a participating whole life insurance policy. This is because in a term insurance policy, most of the insurance premium is used to pay for the insurance policy’s insurance charges. In addition, a part of the insurance premium is also used to pay for the insurance policy’s distribution cost, albeit a smaller component. For one thing, this is similar to a participating whole life insurance policy. Although in a participating whole life insurance policy, the insurance premium is invested into the insurer’s participating fund first. However, the insurer will still take a portion of the monies in the participating fund to pay for an insurance claim and for its own insurance policy’s distribution cost. To this end, we can say that both types of life insurance policy has a similar cost structure.

However, as a participating plan, a participating whole life insurance policy has a participating cash value component. Consequently, the insurer has to cater to the cost of this additional component. Accordingly, this explains why a participating whole life insurance policy tends to be more expensive than a term insurance policy.

With this in mind, given that insurance premium is an expense, I feel that we should spend as little as we can.

Part 4.2: Insurance Cost Structure

Next, let’s look at the insurance cost structure for the two types of life insurance policy. In both cases, for the death benefit, the cost of insurance is usually guaranteed throughout the insurance policy’s premium paying period. To put it another way, you will pay the same amount of money to the insurer every year.

By comparison, for the supplementary benefits, e.g. the critical illness benefit, the cost of insurance is usually non-guaranteed for both types of life insurance policy. Consequently, the insurer may revise the insurance premium rate based on the future experience, and according to Singapore’s laws and regulations. Although the insurer may revise the insurance premium rate in the subsequent years, such adjustments shall not be made on an individual basis. Overall, these adjustments will be made to all its policyholders.

Part 4.3: Insurance Premium Paying Period

On the whole, for a term insurance policy, the insurance premium paying period is usually the same as the insurance coverage period. For example, let’s take the case where you purchase a term insurance policy that covers you for 30 years. In this case, you will pay the insurance premium to the insurer over the next 30 years as well.

In contrast, most participating whole life insurance policies have a limited payment period feature. Accordingly, you may choose to limit the number of years that you pay for the insurance premium. For example, let’s take the case of a 30 year old life insured. In this case, he can opt to pay the insurance premium over 20 years (i.e. till age 50) while staying covered for life.

Next, in both cases, if you have included any supplementary benefits, then the insurance premium paying period for these benefits shall follow the basic life insurance policy.

With this in mind, here is a point to consider about the limited payment period feature. To clarify, when you shorten the insurance premium paying period, you will pay the insurance premium over a shorter time period. As a result, you will pay a higher rate of insurance premium each year. For example, if you choose a 20-year payment term, the insurance premium is $2,000 annually. However, if you choose a 10-year payment term, the insurance premium will become $3,500 annually. To this end, in the latter case, you will need to determine whether you are able to afford the higher rate of insurance premium each year.

Despite that, there is usually an advantage of shortening your insurance premium paying period. Summing up, let’s compare the total insurance premium that you pay over the entire insurance premium paying period. Generally, by shortening the insurance premium paying period, your total insurance premium outlay will be lesser. In the earlier example, if we pay $2,000 annually over 20 years, the total insurance premium outlay is $40,000. In contrast, if we pay $3,500 over 10 years, the total insurance premium outlay is $35,000. Hence, this is also a point to note when you evaluate on the optimal insurance premium paying period.

Part 5: Conclusion on Term vs Whole Life Insurance

All in all, when you look at term vs whole life insurance, I reckon that each type of life insurance policy has its own merit. To illustrate, if you wish to pay the least amount of money for your life insurance coverage, then a term insurance policy tends to have a lower Cost to Benefit Ratio. On the other hand, if you wish to be protected for as long as you live, then a participating whole life insurance policy is able to cover you for life.

With this in mind, here is what I would suggest for you. Rather than to compare the policy features, benefit, and cost, let’s start with you first. For this purpose, let’s go back to the basics to determine your financial needs. Secondly, establish the time period when you need to rely on a life insurance policy for its financial leverage. Thereafter, list your assets and cash flow to find out whether you have sufficient assets to meet your financial needs over the stipulated time period. In the event that there is a financial gap, calculate a budget that you are willing and able to set aside for your life insurance policy. After you have completed the four steps, it will be obvious on the type of life insurance policy that will suit you best.

First Published: 9 October 2019

Last Updated: 26 June 2024

Leave a Reply