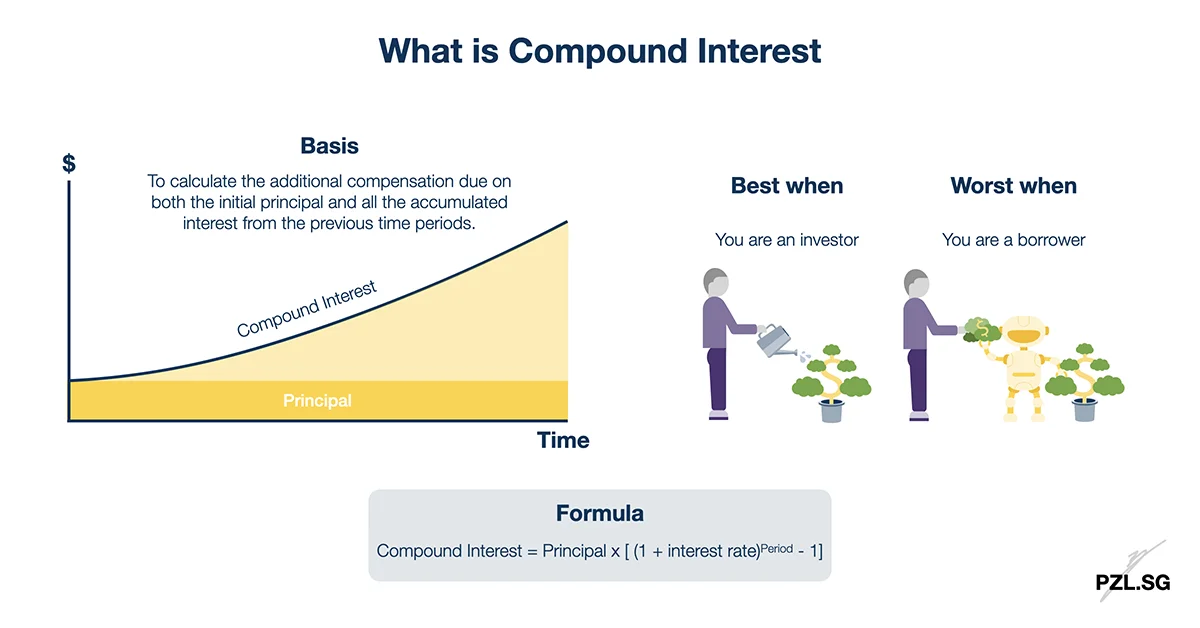

On the whole, we use compound interest to calculate the additional compensation due on both the initial principal and all the accumulated interest from the previous time periods. Unlike simple interest, we will take into account the value of the interest (over time) in our calculation. With this in mind, let’s learn more about compound interest now.

Compound Interest is the 8th wonder of the world. He who understands it, earns it; he who doesn’t, pays it. – Albert Einstein

Table of Contents:

One Minute Summary:

- Compound interest accounts for the additional compensation due on both the initial principal and all the accumulated interest from the previous time periods.

- Given enough time frame, compound interest can turn into exponential growth, which is one of the most powerful forces in finance!

- Generally, compound interest works in your favour when you are an investor. On the other hand, things may get out of hand quickly when you are a borrower.

Part 1: The Formula

Instead of creating another formula, let’s derive it using Simple Interest. This is because simple interest calculates the additional compensation due on the initial principal only. Accordingly, we shall enhance the formula to include the accumulated interest over time.

Part 1.1: Simple Interest Formula

As I have noted previously, simple interest is the multiplication of the principal, the rate, and time period; i.e. Simple Interest = Principal x Interest Rate x Period.

- Simple Interest ($): The compensation on the principal in return for the time spent;

- Principal, P ($): The initial amount of money involved in the situation;

- Interest Rate, i (%): A fixed percentage charged for the situation;

- Time, N (years): The period when the situation occur.

Part 1.2: Total Value at Year 1

To begin with the initial principal P, we will multiply it by the interest rate i to get the interest earned at the end of the year. Summing up, the total value will be P + P x i = P (1 + i). To point out, you will get the same result when you calculate it with simple interest.

Part 1.3: Total Value at Year 2

At year 2, the new principal is P (1 + i). In like manner, we will calculate the interest by multiplying its rate with the principal, i.e. P (1 + i) x i.

In sum, the total value at the end of year 2 will be P (1 + i) + P (1 + i) x i. Through mathematical grouping, that will become P (1 + i) x (1+ i), or P (1 + i)^2.

Part 1.4: Total Value at Year 3

At year 3, the new principal is P (1 + i)^2. Similar to Part 1.3, we will calculate the interest by multiplying its rate with the principal, i.e. P (1+ i)^2 x i.

Altogether, the total value at the end of year 3 will be P (1+ i)^2 + P (1 + i)^2 x i. In the same way, we will simplify it to become P (1 + i)^2 x (1 + i), or P (1 + i)^3.

Part 1.5: Total Value at Year n

As you can see, the power for (1 + i) is directly correlated to the year that we are working with. In detail,

- Total Value at the end of Year 1: P (1 + i)^1;

- Total Value at the end of Year 2: P (1 + i)^2;

- Total Value at the end of Year 3: P (1 + i)^3.

As a result, we can conclude that the total value at the end of year n will be P (1 + i)^n.

Part 1.6: Compound Interest Formula

Accordingly, we will minus the initial principal from the final value to get the compound interest due; i.e. P (1 + i)^n – P, or P [ (1 + i)^n – 1].

Part 2: Sample Calculation

Given that formula, let’s go through two examples together.

Part 2.1: Example 1 – Results from Compound Interest

As an illustration, let’s invest $100,000 into an instrument that yields a rate of 10% for 6 years. As a result, compound interest = $100,000 [ (1 + 0.1)^6 – 1] = $77,156.10.

To sum up, you will receive $100,000 + $77,156.10 = $177,156.10 at the end of 6 years for your investment.

Part 2.2: Example 2 – Results from Simple Interest

At this point, you may wonder

What’s the real impact to include all the accumulated interest in the calculation?

Well, let’s find out now. For this purpose, simple interest = $100,000 x 10% x 6 years = $60,000. Altogether, I will receive $100,000 + $60,000 = $160,000 at the end of 6 years.

In this situation, you will have missed out $77,156.10 – $60,000 = $17,156.10. This is owing to the interest earned on top of the interest accumulated from the previous time period.

Part 3: Real Life Application

As a matter of fact, we use compound interest frequently in our daily lives. For one thing, a classic example will be the interest that you receive from the bank. Generally, most local banks give us an interest rate of 0.05% per annum for our deposit. To illustrate, let’s keep $10,000 with them for 10 years.

In time to come, the compound interest will be $10,000 [ (1 + 0.0005)^10 – 1] = $50.11 (rounded to 2 decimal places)

All in all, you will have $10,000 + $50.11 = $10,050.11 for saving our money with the bank. For the most part, can you imagine how painful it is to not touch your money for 10 years for just $50? Argh!

Part 4: Conclusion

When you compute the returns using compound interest, its yield will always be larger as compared to the returns generated by simple interest. This is because interest is earned on top of all the accumulated interest in the time period.

In the real world, there are many applications, e.g. calculation for bank interest, investment return.

All in all, your money is working harder for you when your returns is computed using compound interest. Of course, this is if and only if you keep the capital and the interest earned within the account!

First Published: 4 December 2019

Last Updated: 9 March 2021

Leave a Reply