An Integrated Shield Plan Rider (IP Rider) is an optional add-on to your Integrated Shield Plan (IP). It is designed to improve cost predictability and reduce your out-of-pocket expenses when you are hospitalised.

This article explains the key features, limitations, and trade-offs of IP Riders. It will help you decide whether they enhance your existing health insurance coverage or represent a cost you can forgo.

Important Update: Integrated Shield Plan Riders must comply with the new Ministry of Health (MOH) requirements by April 2026. I will update this post as insurers release specific details. Meanwhile, here is what you need to know and how these changes may affect you: Integrated Shield Plan Rider Changes Singapore: What You Need to Know

Table of Contents:

- What is an Integrated Shield Plan Rider

- Insurance Coverage (Benefits)

- Cash Value

- Insurance Premium (Cost)

- Limitations and Risks

- Claims

- Insurance Nomination

- Eligibility

- Target Audience

- Integrated Shield Plan vs MediShield Life

- Final Thoughts

- Changelog

One Minute Summary:

- What it is: A supplementary policy attached to your Integrated Shield Plan (IP) that reduces your out-of-pocket costs during a hospital stay.

- Key Benefit: It reduces the Deductible and Co-insurance you would otherwise pay in cash or MediSave.

- Cancer Coverage: Riders now provide the primary way to access coverage for non-standard cancer drugs (non-CDL) that IPs exclude.

- Cost: Riders must be paid in cash only.

- Upcoming Changes (1 April 2026): New riders will no longer cover the deductible, and the co-payment cap will be raised to $6,000.

Part 1: What is an Integrated Shield Plan Rider

An Integrated Shield Plan Rider (IP Rider) is a supplementary policy attached to your main Integrated Shield Plan. You cannot purchase a rider on its own – it must “ride” on a base insurance plan from the same insurer.

To understand the rider, we must first understand the Integrated Shield Plan (IP). This private health insurance plan provides higher coverage limits and access to private healthcare in higher ward classes (e.g., Class A) or private hospitals. However, the limits of coverage is subject to deductibles and co-insurance, which are costs you must pay yourself.

The IP Rider builds on this layer by covering these deductibles and co-insurance. This effectively reduces your out-of-pocket liability.

Part 1.1: How an Integrated Shield Plan Rider Works

Singapore’s healthcare insurance structure is designed in layers.

Layer 1: MediShield Life

- Automatic and mandatory for all Singapore Citizens and Permanent Residents

- Covers basic hospitalisation coverage, mainly for Class B2/C wards in public hospitals

- Designed for basic adequacy rather than comfort or choice

Layer 2: Additional Private Insurance Coverage (Integrated Shield Plan)

- This is a MediSave-approved Integrated Shield Plan offered by private insurers and regulated by the Ministry of Health (MOH)

- Provides coverage for Private Hospitals or Class A/B1 Wards in public hospitals

Even with an IP, you are responsible for the deductible (typically $3,500) and co-insurance (typically 10% of the bill).

Layer 3: Optional Rider

- Also offered by private insurers and regulated by the Ministry of Health (MOH)

- Pays the co-insurance and deductible that the Integrated Shield Plan leaves behind (from Layer 2)

The IP Rider improves the predictability of your final bill. Instead of paying an unknown 10% of a large medical insurance claim, you pay a capped co-payment (e.g., $3,000). Unlike the MediShield Life premium (Layer 1) and IP premiums (Layer 2), IP Rider premiums must be paid entirely in cash.

Part 1.2: Insurers

The following insurers currently offer riders for Integrated Shield Plans in Singapore.

- AIA Singapore Private Limited: HealthShield Gold Max

- Great Eastern Life Assurance Co: GREAT SupremeHealth

- HSBC Life (Singapore) Private Limited: HSBC Life Shield

- Income Insurance Limited: Enhanced IncomeShield

- Prudential Assurance Company Singapore: PRUShield

- Raffles Health Insurance: Raffles Shield

- Singapore Life Limited: Singlife Shield

Part 2: Insurance Coverage (Benefits)

Part 2.1: Reducing Out-of-Pocket Costs

The primary function of the rider is to cover the Deductible and Co-insurance.

- Without the Rider: You pay the deductible + 10% co-insurance.

- With Rider: You pay a 5% co-payment.

- The Safety Net: Most riders include a Co-payment Cap (typically $3,000 per policy year) if you use the insurer’s panel of specialists. This ensures that even if your bill is $500,000, your cash outlay remains capped at $3,000.

Part 2.2: Cancer Drug Treatment and Services

Since the Cancer Drug List (CDL) was implemented in September 2022, rider coverage for cancer drugs has become increasingly valuable. Main IPs now only cover drugs listed on the CDL, and only up to specific monthly limits.

The Coverage Gap in Integrated Shield Plans:

- If a drug is not on the Cancer Drug List, the IP covers $0.

- If a drug is on the CDL but expensive, you may incur additional out-of-pocket cost.

To address this gap, most IP Riders now include an additional rider benefit specifically for cancer coverage, offering:

- Multiplier for drugs on the CDL: They boost the claim limit for CDL drugs.

- Non-CDL coverage: Reimbursement for drugs not on the Cancer Drug List.

For many policyholders, access to these non-standard cancer treatments is now the primary reason to hold a rider.

Part 2.3: Coverage Period

Like the Integrated Shield Plan, IP Riders are structured to provide lifelong coverage, provided premiums are paid when due and the policy remains in force. This continuity is particularly relevant as healthcare needs tend to increase with age. However, the rider is contingent on the main plan – if you drop your IP, the rider is automatically terminated.

Part 3: Cash Value

An Integrated Shield Plan Rider is a non-participating plan. This means:

- The plan does not accumulate cash value

- There is no surrender value

- There is no investment component

In other words, premiums are paid solely in exchange for medical insurance coverage.

Part 4: Insurance Premium (Cost)

Part 4.1: Premium Determinants

Premiums are age-based and payable annually. Insurers determine premiums using Age Next Birthday (ANB) at each renewal. Premiums increase with age, reflecting higher healthcare utilisation and costs.

Part 4.2: Why Premiums Increase with Age

Integrated Shield Plan Riders operate on a risk-pooling model, and the rates are non-guaranteed. Premiums collected from policyholders fund claims across the insured pool. As age increases, the probability and cost of claims rise. This results in higher premiums for older age bands to account for increased medical risks.

Part 4.3: Type of Payment

Premiums must be paid fully in cash.

Part 4.4: Premium Paying Period

Integrated Shield Plans Riders are yearly renewable policies. Premiums are payable annually for as long as coverage is maintained. Some insurers allow payments on a monthly basis, though this is more expensive.

Part 4.5: Estimated Lifetime Cost

Premium levels depend on residency status and plan tier. Based on available insurer averages, the estimated lifetime premium cost (from age 0 to 100) is approximately:

- Class A ward (public hospital): $96,870

- Private hospital: $370,569

These figures reflect averages across the 7 insurers and apply to the IP Rider premiums only.

Part 5: Limitations and Risks

Part 5.1 : Coverage scope

The IP Rider follows the main plan. Generally, it does not cover:

- Treatments excluded by the main IP (e.g., cosmetic surgery, experimental procedures not recognised by MOH)

- Pre-existing conditions, unless explicitly accepted during underwriting.

Part 5.2: Pre-Existing Conditions

A pre-existing condition is any illness, injury, or symptom that existed before you purchased the plan or during the waiting period.

Coverage for pre-existing conditions is subject to medical underwriting. Depending on the outcome, such conditions may be excluded, loaded (higher premiums), or deferred (coverage delayed).

If you buy an IP and Rider when you are healthy, you are fully covered. However, if you try to add a rider at a later stage, standard medical underwriting will apply. In this case, if you have a medical condition, the insurer may exclude the condition (for rider coverage) or reject the application entirely.

Part 5.3: Panel Restrictions and Pre-Authorisation

Some plans require the use of the insurer’s panel network for full benefits. Certain treatments also require pre-authorisation. Visiting a non-panel doctor or undergoing treatments without pre-authorisation may result in higher out-of-pocket costs or reduced coverage.

Generally, if you visit a panel doctor, the rider will cap the co-payment at $3,000 per policy year. For non-panel doctors, the cap is often removed. This means you will pay the full co-payment with no maximum limit.

Part 6: Claims

Part 6.1: Claim Process

The claims process is seamless. You do not need to file a separate claim for the rider.

To make a claim, inform the medical institution. Claims are submitted electronically to the insurer, which processes the MediShield Life coverage portion on behalf of the Central Provident Fund (CPF) Board.

Once approved:

- The IP pays the hospital directly.

- You may use your MediSave account to pay your share, within the withdrawal limits.

- Any remaining balance is payable in cash.

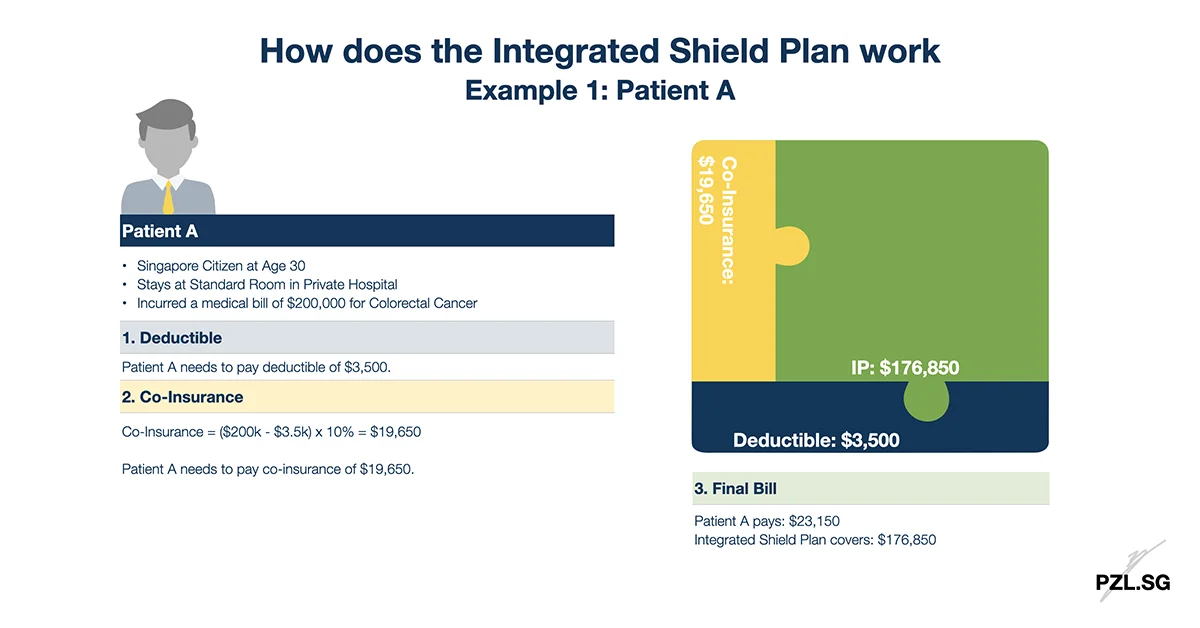

Part 6.2: Example – Integrated Shield Plan without Rider

Let’s revisit the example from the article, What is Integrated Shield Plan Singapore.

Patient A’s Profile:

- Singapore Citizen at Age 30

- Stays in a Standard Room in a Private Hospital

- Incurred a total bill of $200,000 for Colorectal Cancer

Here is the breakdown of Patient A’s medical bill:

- First, Patient A pays a deductible of $3,500.

- Next, Patient A pays 10% co-insurance of $19,650.

- Finally, the Integrated Shield Plan covers the remainder of the bill.

In total, Patient A pays $23,150 out-of-pocket, while the Integrated Shield Plan covers $176,850.

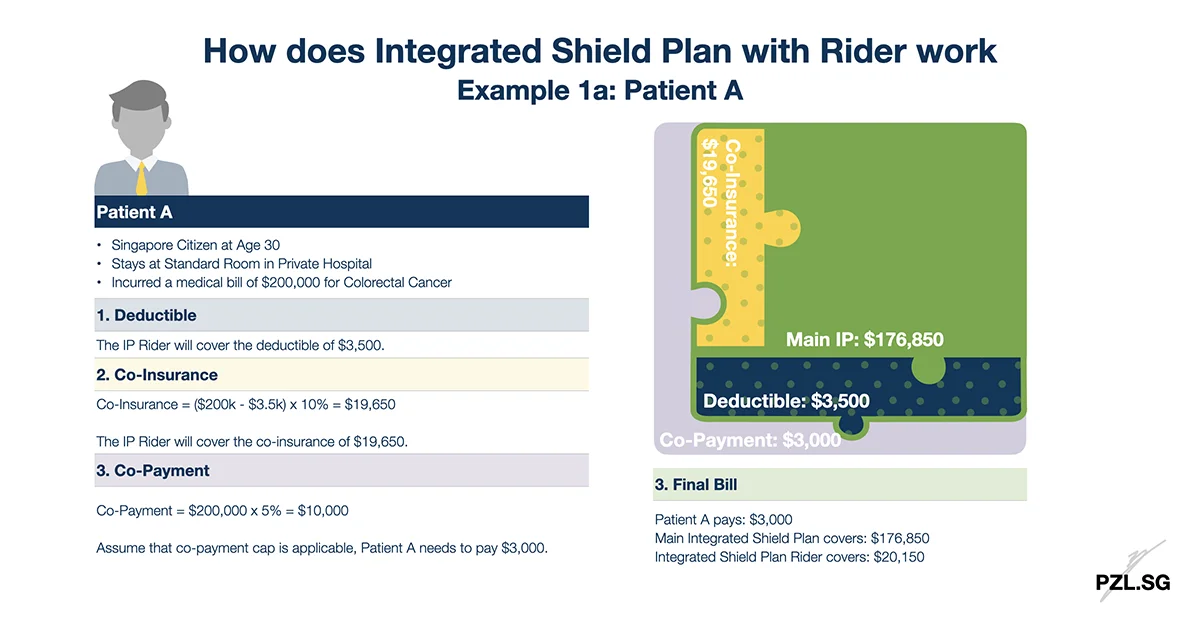

Part 6.3: Example – Integrated Shield Plan with Rider

With an IP Rider, this is how the claim computation looks:

Here is the breakdown for Patient A’s medical bill with the rider:

- First, the rider will cover the deductible of $3,500.

- Next, the rider will cover the co-insurance of $19,650.

- Thereafter, Patient A pays a co-payment of $10,000 (or $3,000 if the co-payment cap applies).

- Finally, the Integrated Shield Plan will cover the remainder of the bill.

Note that the co-payment Patient A pays is lower than the sum of the deductible and co-insurance, regardless of whether the co-payment cap applies.

Part 7: Insurance Nomination

Integrated Shield Plans do not provide death benefits. As such, insurance nomination does not apply.

Part 8: Eligibility

You must first have an Integrated Shield Plan before you can purchase a rider. All Singapore residents may apply for an Integrated Shield Plan Rider, including Citizens, Permanent Residents, and foreigners with a valid pass. Some insurers restrict plan types for foreigners, though no such restrictions apply to locals.

When buying an integrated shield plan, you must declare any medical conditions. Underwriting outcomes generally fall into five categories:

- Standard acceptance: You will pay the standard premium rate for standard coverage.

- Loading: You will pay an additional premium to cover the pre-existing condition.

- Exclusion: You will pay the standard premium rate. However, the insurance policy will not cover the pre-existing condition.

- Postpone: The insurer is unable to offer any terms of acceptance at this time. However, you may apply again at a later time.

- Decline: The insurer is unable to offer any terms of acceptance.

Children are typically eligible from 15 days old, and the last entry age is generally 75. Policies may be renewed for life thereafter.

Part 9: Target Audience

Integrated Shield Plan Riders are not essential for everyone. They represent a trade-off between current cash flow (premiums) and future risk (hospital bills).

An IP Rider may suit individuals who:

- Value cost certainty: You want to know the maximum amount (e.g., $3,000) you need to pay, regardless of how severe the illness is.

- Prioritise access: You want access to non-standard (non-CDL) cancer treatments that the main IPs exclude.

- Have stable cash flow: You can comfortably pay the cash premiums without impacting your retirement savings or daily needs.

Meanwhile, an IP Rider may be less suitable if you:

- Are budget-conscious: If the premiums strain your monthly budget, stick with just the main IP. The main IP prevents bankruptcy; the rider buys absolute peace of mind.

- Rely on public hospitals: If you are content with Class B2/C wards, out-of-pocket costs are already subsidised, making a private rider a luxury.

- Prefer self-insurance: If you have substantial liquid savings (e.g., $50,000+) set aside specifically for healthcare, you may choose to pay the deductible and co-insurance yourself. This is rather than paying an insurer annual premiums to do it for you.

Part 10: IP Rider vs IP

Here is a comparison of Integrated Shield Plans and their riders to help you visualise the difference between an Integrated Shield Plan and its accompanying rider. In summary, the rider is a cash-funded upgrade that buys you predictability and wider access to cancer drug treatments and services.

| IP (Main Plan) | IP Rider (Add-On) | |

|---|---|---|

| Primary Purpose | Covers the majority of the hospital bill (subject to deductible, co-insurance) | Covers the deductible and co-insurance left by the IP |

| Funding Source | MediSave (up to AWL) + Cash | Cash only |

| Deductible | You pay up to $3,500 | Typically covered |

| Co-Insurance | You pay 10% of the remaining bill | Typically reduced to a 5% or 10% co-payment |

| Co-Payment Cap | No cap | Typically capped at $3,000 or $6,000 for panel doctors |

| Cancer Drug List (CDL) | Covers treatments and services on CDL | Covers treatments and services on both CDL and non-CDL |

| Standalone/Rider | You can buy the IP only | Must be attached to the IP |

Part 11: Final Thoughts

An Integrated Shield Plan Rider provides absolute peace of mind in your healthcare financing. It reduces your out-of-pocket exposure significantly. However, it does so by shifting those costs into higher annual premiums.

For some, that trade-off is worth every dollar. For others, the premiums represent money better saved or invested elsewhere.

In any case, a rider does not make you “more insured” in terms of ward class. It simply changes when you pay – upfront (via premiums) or at the point of treatment (via deductible and co-insurance).

However, with the rising costs of cancer therapies, the rider’s role has evolved. It is no longer just about covering the deductible and co-insurance. It is increasingly about securing access to expensive, non-standard drugs that the existing healthcare framework does not cover.

Part 12: Changelog

This section tracks the major regulatory changes to the IP Rider over time.

Part 12.1: Removal of Deductible Coverage, Increase in Co-Payment Cap

Implementation Date: 1 April 2026

- What changed: Ministry of Health mandated for new IP Riders to remove the coverage for the minimum IP deductibles set by MOH. The co-payment cap will also be raised to a minimum of $6,000. The cap will apply to co-payments excluding the minimum IP deductible.

- Before: IP Riders cover the deductible. The co-payment cap is $3,000.

- After: IP Riders no longer cover the deductible. The co-payment cap is doubled to $6,000.

As a result, you must pay the first $3,500 of the medical bill. Additionally, your final out-of-pocket cost may be higher (due to the higher co-payment cap). Despite this, your premiums are expected to be lower.

Part 12.2: Cancer Drug Treatments and Services

Implementation Date: 1 September 2022

- What changed: Ministry of Health Singapore (MOH) implemented the Cancer Drug List (CDL).

- Before: “As-charged” cancer coverage for the Integrated Shield Plan and its accompanying riders.

- After: Government will provide a subsidy only if the cancer treatment is on the Cancer Drug List (Drug Classes A to E). Only treatments on the CDL (Drug Classes A to E) may be claimed under the IP and insurers have to set a sub-limit on the coverage amount. IPs no longer cover cancer treatments not on the CDL (Drug Class F)

As a result of this implementation, IP riders became the only way to get coverage for non-CDL drugs and to achieve higher claim limits for expensive CDL treatments.

Part 12.3: Introduction of Co-Payment

Implementation Date: 8 March 2018

- What changed: Ministry of Health mandated for the new IP Riders to incorporate the co-payment and co-payment cap feature.

- Before: IP Riders cover the full deductible and co-insurance.

- After: IP Riders cover the deductible and co-insurance, subject to a minimum co-payment of 5% or more for your eligible medical bill.

The co-payment was introduced to prevent over-consumption of healthcare services. The co-payment cap helps reduce large bill shocks.

First Published: 20 May 2020

Last Updated: 14 January 2026

Leave a Reply