Dependants’ Protection Scheme (“DPS”) is a common example of a yearly renewable term insurance policy in Singapore. In fact, this is one of those insurance policies that we will likely own and forget. With this in mind, let’s do a revision on this insurance scheme.

Table of Contents:

- Automatic Enrolment

- Scope of Coverage and Policy Term

- Premium and Payment Term

- Claim Matters

- Conclusion on Dependants’ Protection Scheme

One Minute Summary:

- To point out, Dependants’ Protection Scheme went through an enhancement on 1 April 2021. While this post reflects the new coverage, you may read about the changes here.

- For Singaporeans and Permanent Residents (between 21 and 65 years old), your coverage begins automatically after making your first CPF working contribution.

- Despite automatic enrolment, you need to declare your health status to the insurer.

- Dependants’ Protection Scheme provides a lump sum payout of S$70,000 for Death, Terminal Illness, and Total Permanent Disability.

- On balance, the insurer will adjust your renewal premium annually, depending on your age last birthday.

- In any case, Dependants’ Protection Scheme’s payout does not form part of your CPF proceeds. Therefore, you should make an insurance nomination.

Part 1: Automatic Enrolment

Part 1.1: Who is eligible?

Firstly, Dependants’ Protection Scheme works on an opt-out basis. As soon as you fulfil the following three conditions, you will enrol into the insurance scheme automatically:

- Singapore Citizen or Permanent Resident;

- Between 21 and 65 years old;

- Made your first CPF working contribution.

Under those circumstances, you will receive a welcome package from the assigned insurer, Great Eastern Life. Thereupon, you will be covered for the next twelve months (until the next renewal).

Part 1.2: Health Declaration

Even though enrolment is automatic, Dependants’ Protection Scheme is not a guaranteed issuance policy. Emphatically, you will need to declare your health through the declaration form enclosed in the welcome package. Thereafter, Great Eastern Life will confirm your enrolment in due time.

To explain, this practice is to manage the underwriting risk. Otherwise, this insurance scheme may not be sustainable in the long run. For instance, we may need to pay a much higher premium for the same (or lower) level of insurance coverage.

Part 1.3: What if I want to terminate my coverage?

In this situation, you will need to contact Great Eastern Life directly. After submitting the opt-out form, the insurer will terminate your coverage without any penalty.

Before you do so, you should conduct a comprehensive financial portfolio review. This is so as to ensure that you have the right scope of coverage in place. To illustrate, your family may be depending on your income for survival. What’s more, who is going to pay your liabilities when you are gone?

Part 1.4: What if I want to enrol / re-enrol into this insurance scheme?

On this occasion, you will need to submit an application with Great Eastern Life directly. It is important to realise that acceptance will depend on your health status then.

Part 1.5: Am I covered by Dependants’ Protection Scheme currently?

For this purpose, you may check the status on CPF’s website.

- Login to my CPF Online Services.

- From the left navigation menu, click “My Messages”.

- Under the Insurance category, it will show whether you are covered under the Dependants’ Protection Scheme currently.

Part 2: Scope of Coverage and Policy Term

Above all, Dependants’ Protection Scheme covers you worldwide. Hence you don’t need to worry when you are travelling or residing overseas.

Part 2.1: What am I covered for?

In detail, Dependants’ Protection Scheme covers you for

- Death;

- Terminal Illness;

- Total Permanent Disability.

What is Terminal Illness?

Generally, this refers to an illness that is likely to result in your death within twelve months.

What is Total Permanent Disability?

Basically, it refers to either

- Your inability to take part in any employment; or

- The total permanent loss of physical function of either both eyes, or two limbs, or one eye and one limb.

Part 2.2: How much am I covered for?

In sum, if you are

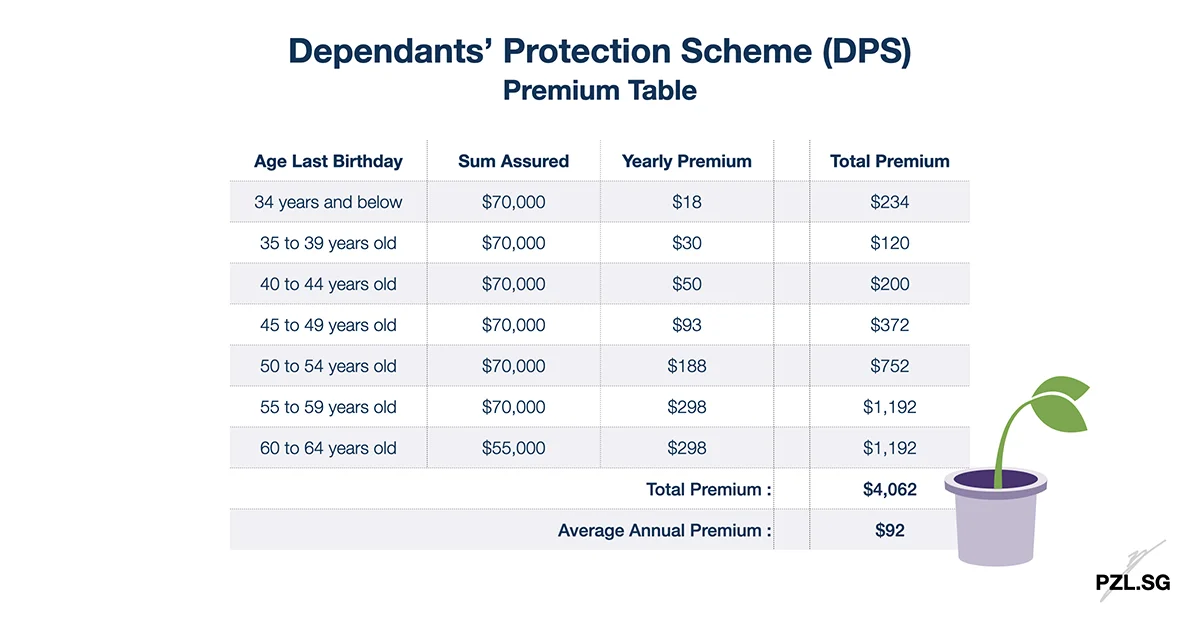

- Between 21 and below 60 years old: Then the sum assured is S$70,000.

- Between 60 and before 65 years old: Then the sum assured will be S$55,000.

Part 2.3: When will the cover end?

By and large, Dependants’ Protection Scheme will cover you till your 65th birthday.

Part 2.4: Will I get back any money after the cover ends?

Since this is a term insurance policy, there is no cash value. Consequently, you won’t get back anything at the end of the coverage period.

Part 3: Premium and Payment Term

Part 3.1: How much does Dependants’ Protection Scheme cost?

Summing up, the annual insurance premium ranges between $18 to $298. As a yearly renewable term insurance policy, the exact premium depends on your renewal age. To point out, the insurer will take your age last birthday as the reference.

Part 3.2: How to pay for Dependants’ Protection Scheme?

- Firstly, the insurer will deduct the premium from your CPF Ordinary Account.

- In the event that there is insufficient funds, the deduction shall take place from your CPF Special Account.

- If both attempts fail, then you will have to pay the outstanding premium in cash.

For one thing, you can pay the premium for your own Dependants’ Protection Scheme policy only. In other words, you cannot use your CPF monies to pay for your family member’s coverage.

Part 3.3: What if I cannot afford the coverage?

In this case, you may lower the sum assured, down to a minimum of S$5,000.

Part 4: Claim Matters

Generally, you will have to submit the relevant claim form to the assigned insurer, Great Eastern Life directly.

Part 4.1: Who gets the death benefit?

In order to answer this question correctly, we need to determine the exact scenario that you are in.

Part 4.1.1: Without an Insurance Nomination, and without a valid Will

In this case, the insurer will distribute the payout to a proper claimant, e.g. family member.

Part 4.1.2: With an Insurance Nomination

On this occasion, your nominees will receive the payout. For the most part, each nominee will receive the allocation that you have stated in the insurance nomination form.

Part 4.1.3: With a valid Will

After completing the probate process, your testator will distribute the payout according to the beneficiaries in the will.

Part 4.2: Who gets the payout for Total Permanent Disability?

Since you are still alive, you will receive the payout.

In any case, Dependants’ Protection Scheme’s payout does not form part of your CPF proceeds. Consequently, you cannot use a CPF Nomination form to distribute the payout. Additionally, this payout is not protected against your creditors.

Part 4.3: Claim Exclusion

Despite that automatic enrolment, there is no payout if any of the following events occur within the first year:

- Self-inflicted injury or suicide;

- Committed a criminal offence that is punishable by death; or

- Committed a criminal act intentionally.

Additionally, there is also no payout when

- You were not in good health before the coverage begins;

- You have provided false or misleading information;

- The claim arose from wars or any warlike operations; or

- The claim arose from participation in any riot.

Part 5: Conclusion on Dependants’ Protection Scheme

On the whole, Dependants’ Protection Scheme is a simple term insurance policy that most of us will have. With this in mind, you should consider it as part of your overall financial portfolio planning. This is especially true since you are paying money for it. Hence, we should find out how to integrate it into your existing portfolio. Finally, remember to submit an insurance nomination for this policy. Above all, do not leave it to the law to decide on the distribution for you!

Checklist:

- How much life insurance coverage do you have?

- Did you keep or terminate this policy?

- Have you made an insurance nomination for this policy?

First Published: 28 August 2019

Last Updated: 17 May 2021

Leave a Reply