Five years ago, Central Provident Fund (CPF) Board introduced MediShield Life to replace the older MediShield. Together with better coverage at an affordable premium, MediShield Life won applauses for its “for all, for life” coverage. Notwithstanding that positive response, it is time for the Council to enhance our nation’s healthcare policy again. With this in mind, let’s understand the eight changes that took place on 1 March 2021.

Table of Contents:

- What is MediShield Life?

- Refresh and Refine Claim Limit

- Larger healthcare transformation effort

- Other Recommendations

- Premium Adjustment

- What’s next?

One Minute Summary:

- Firstly, MediShield Life is designed for Singaporeans that seeks subsidised medical treatment in public hospitals in Singapore.

- At length, the MediShield Life Council has made recommendations to enhance our coverage while keeping premiums affordable. (Details in Part 2 to Part 5.)

- Furthermore, Ministry of Health has committed additional premium support for Singaporeans over the next two years. Above all, no one will lose MediShield Life coverage due to financial difficulties.

Part 1: What is MediShield Life

Before that, let’s do a quick recap on MediShield Life. In essence, it provides coverage against medical bills for hospitalisation and certain approved outpatient treatments in Singapore. For the most part, it covers all Singaporeans and Permanent Residents in Singapore.

At this time, the healthcare cost per person continues to rise about 10% year on year on the national level. Consequently, it becomes imperative to improve MediShield Life’s scope of coverage. All in all, we can divide the upcoming changes into three sections (Part 2 to Part 5).

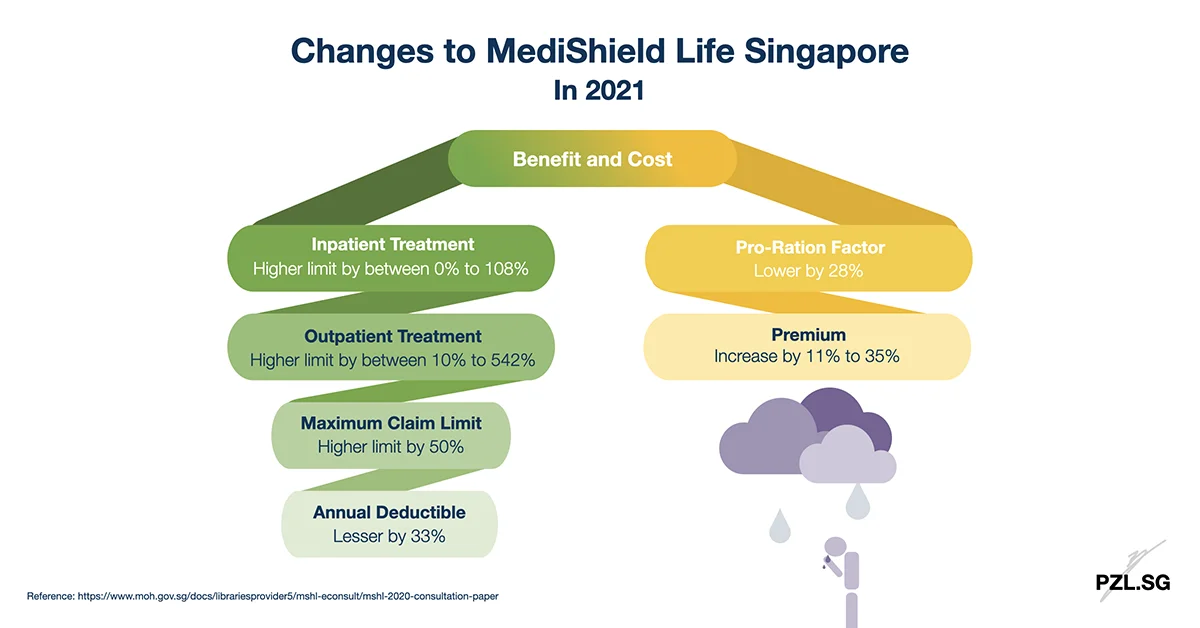

Part 2: Refresh and Refine Claim Limit

Part 2.1: Subsidised Bills and Claim Limits

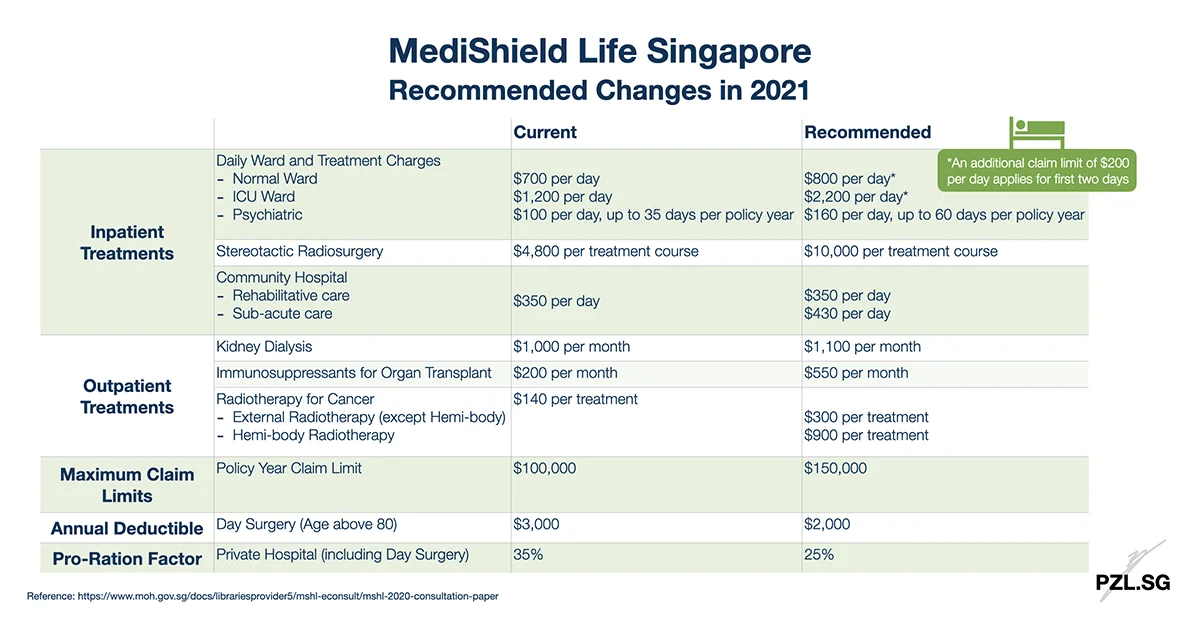

Overall, MediShield Life will refresh its claim limits to cover nine in ten subsidised bills. Additionally, Ministry of Health will review the claim limits around every three years. Emphatically, let’s hope that medical inflation doesn’t catch up that quickly.

Part 2.2: Claim Limits for Community Hospital care and Outpatient Radiotherapy

Moreover, MediShield Life Council will introduce treatment-specific claim limits for costlier types of treatments. For example, sub-acute care tends to be more expensive than rehabilitative care. As a result, patients under sub-acute care may feel the stretch today. For that reason, the Council will separate the claim limits for these two groups of patients.

In like manner, there will be a separate claim limit for external radiotherapy and hemi-body radiotherapy. In effect, this will provide better coverage for patients in the latter category.

Part 2.3: Higher Policy Year Claim Limit

Without a doubt, some of us wonder whether the current $100,000 per policy year claim limit is sufficient. Following the changes, MediShield Life will increase this claim limit to $150,000 per policy year. In sum, this gives us 50% more protection against large medical bills in Singapore.

Part 3: Larger healthcare transformation effort

In addition to raising the claim limit, the Council proposed deeper changes to the functionality of MediShield Life’s coverage.

Part 3.1: Higher claim limit for the first two days of acute hospital stay

Generally, you should expect to undergo more tests and investigations during the first few days of admission. Evidently, this helps the doctors to diagnose your medical condition accurately. Since you require more tests, medical bills tend to become more expensive as well. However here is the problem:

MediShield Life imposes a per day limit for daily ward and treatment charges. Under those circumstances, you may exceed this limit within the first few days. Seeing that issue, the Council proposed to raise the daily ward and treatment charges limit. What’s more, you will enjoy an additional claim limit of $200 per day for the first two days. This is in the hope that you can undergo the necessary investigations without worrying about the final bill.

Part 3.2: Lower Deductible for Day Surgery

Moreover, there is a constant dilemma between a day surgery and an inpatient stay for patients above 80 years old. This is owing to the fact that presently,

- the annual deductible for a day surgery is $3,000; while

- the annual deductible for an inpatient stay in C ward is $2,000.

In this situation, we will prefer to choose an inpatient stay. This is so as to reduce the cost that we need to pay on our own.

In time to come, the annual deductible for both day surgery and inpatient stay in C ward will be $2,000. Hence, there is no incentive for you to occupy that precious hospital bed (unless you really need it).

Part 4: Other Recommendations

Part 4.1: Lower Pro-Ration Factor

In order to understand the rationale for the pro-ration factor, let’s reflect upon MediShield Life’s focus. On the whole, MediShield Life is designed for

- Singaporean; and

- Seeks subsidised treatment in Class B2 or C wards in public hospitals; or

- Seeks subsidised outpatient or day surgery treatments in public hospitals

If you are outside this scope, then a pro-ration factor will apply. In effect, MediShield Life’s payout will become similar to its original intention. To illustrate, a 35% pro-ration factor for private hospitals is supposed to align with a subsidised bill in public hospitals.

Well, this calculation is far from ideal in truth. Consequently, the Council proposed to lower it to 25%. Thereupon, you will think twice about that visit to a private hospital next time.

Part 4.2: Remove two standard exclusions

As our nation’s healthcare policy, MediShield Life should take the lead to help more individuals through their recovery process. For this purpose, MediShield Life shall cover the following two treatments:

- Arising from attempted suicide or intentional self-injury;

- Arising from drug addiction, alcoholism, or the person being under the influence of drugs or alcohol.

Part 5: Premium Adjustment

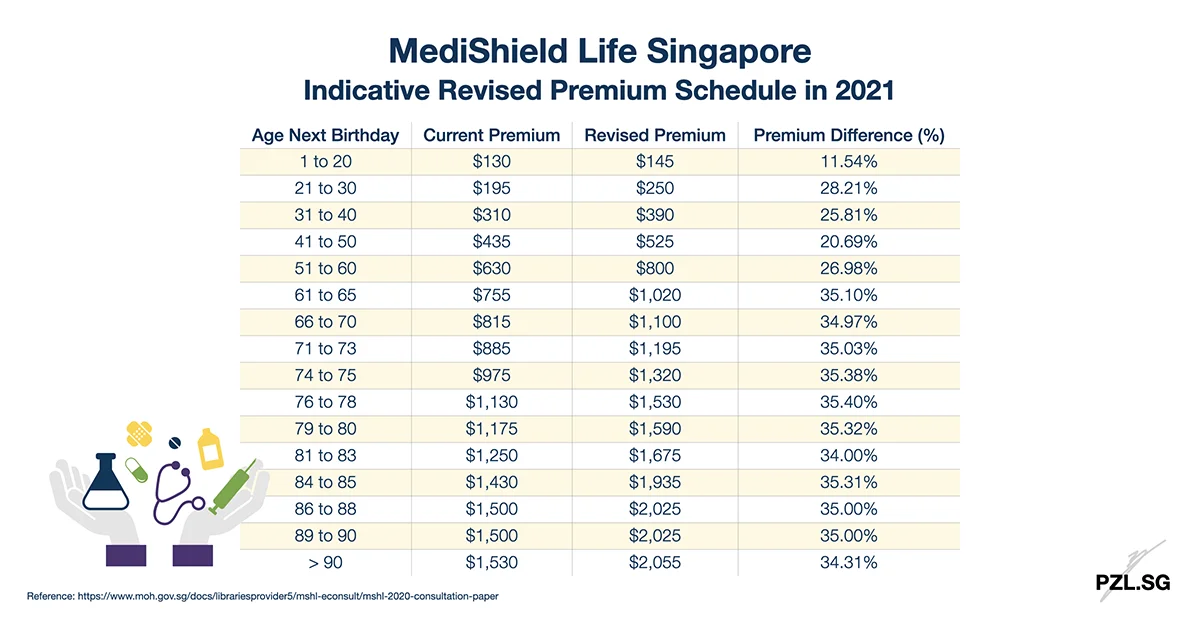

Obviously, MediShield Life cannot support perpetual enhancements by sticking to the old premium rates. Accordingly, the actuary has recommended the premium to increase by up to 35.40%, depending on your age next birthday. To point out, this indicative premium is before any government’s subsidy.

Part 6: What’s next?

As our nation’s healthcare policy, MediShield Life must constantly improve to meet healthcare needs in Singapore. Altogether, these changes will give us a better ability to manage our medical bills.

On the other hand, I’m curious on what is next from the seven private insurers. For instance, I have extracted part of a general exclusion from an integrated shield plan,

any injury or illness caused directly or indirectly , by self-destruction or intentional self-inflicted injury

After MediShield Life’s proposed changes, will this push the respective insurers to become more inclusive as well? Meanwhile, how will they adjust their premium then?

Checklist:

- Do you intend to seek unsubsidised treatments in Singapore?

- Are you comfortable with MediShield Life’s limitations?

- Have you planned on how to afford the insurance premium over the long-term?

First Published: 14 January 2021

Last Updated: 8 March 2021

Leave a Reply