A clear and effective monthly budget ensures you stay in control of your finances. This is a key step towards financial independence. As a Financial Adviser, I often meet individuals with decent income but still feel stuck. These individuals work hard, save consistently, but worry about not progressing fast enough. After a deep conversation and reality check, the issue almost always narrow down to two things – they do not truly understand their monthly cash flow and they do not have a reliable budgeting system. In this guide, I will walk you through how to create a monthly budget that is not only automated and realistic, but also one that motivates you to stick to the system.

Table of Contents:

- What is a Monthly Budget

- Why You should create a Monthly Budget

- How to create a Monthly Budget

- Final Thoughts

Part 1: What is a Monthly Budget

To begin with, let’s go through the framework in a monthly budget. Altogether, a monthly budget accounts for your cash inflow (income) and cash outflow (expenditure). In effect, you become more aware of your monthly surplus (positive net cash flow) or shortfall (negative net cash flow). Given that information, we are able to determine whether you are financially healthy, or seeing the need to make certain adjustments to your financial habits.

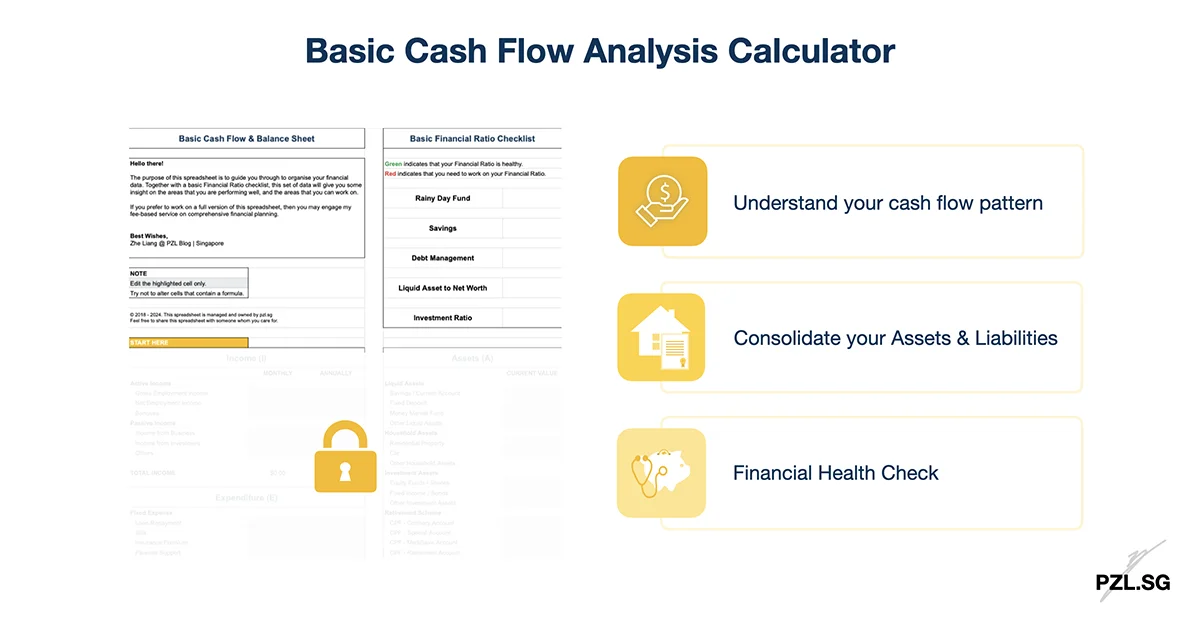

Generally, a basic budget consists of two sections – income and expenditure (you may read more about its components in Understanding Your Personal Cash Flow). After listing down all your sources of income and expenditure, its difference is your net cash flow. If you are looking for a reliable cash flow analysis calculator, then enter your name and email address in the following form and I will send the calculator over to you.

Part 2: Why You should create a Monthly Budget

Above all, a monthly budget sets an expectation for your cash flow. In due time, you will be able to achieve three objectives:

- Track your income and expenditure (for future cash flow projection);

- Enforce discipline against any unnecessary expenditure (build good financial habits);

- Build up savings over time (achieve your financial goals).

To demonstrate the use of a monthly budget, let’s go through a case study together. In this case, we want to buy our future home in five years’ time;

- Cost of the Home: $500,000

- Type of Loan: HDB Loan with 10% downpayment

- Mode of Payment: Cash

Given that 10% downpayment, you will need to save $500,000 x 10% = $50,000 in five years’ time. To put it another way, this is equivalent to $10,000 a year, or about $833.33 a month. With this intention in mind, you must have at least this amount in your monthly net cash flow.

Despite that, it may not be wise to save up for this amount blindly. For one thing, you may take advantage of the compounding effect of money so that you can achieve more (money) with less (capital). Here are some possibilities as an illustration:

- Financial Instrument A gives a yield of 1% per annum: In this situation, you are able to achieve the same goal by saving $813.02 monthly.

- Financial Instrument B gives a yield of 2% per annum: On this occasion, you are able to achieve the same goal by saving $793.05 monthly.

In addition to saving up for your financial goal, you will also want to ensure that you have sufficient liquidity throughout your wealth accumulation journey. For example, would saving $833 monthly cripple your monthly cash flow? Overall, a monthly budget forces you to put more thoughts into the money that you earn and spend each month.

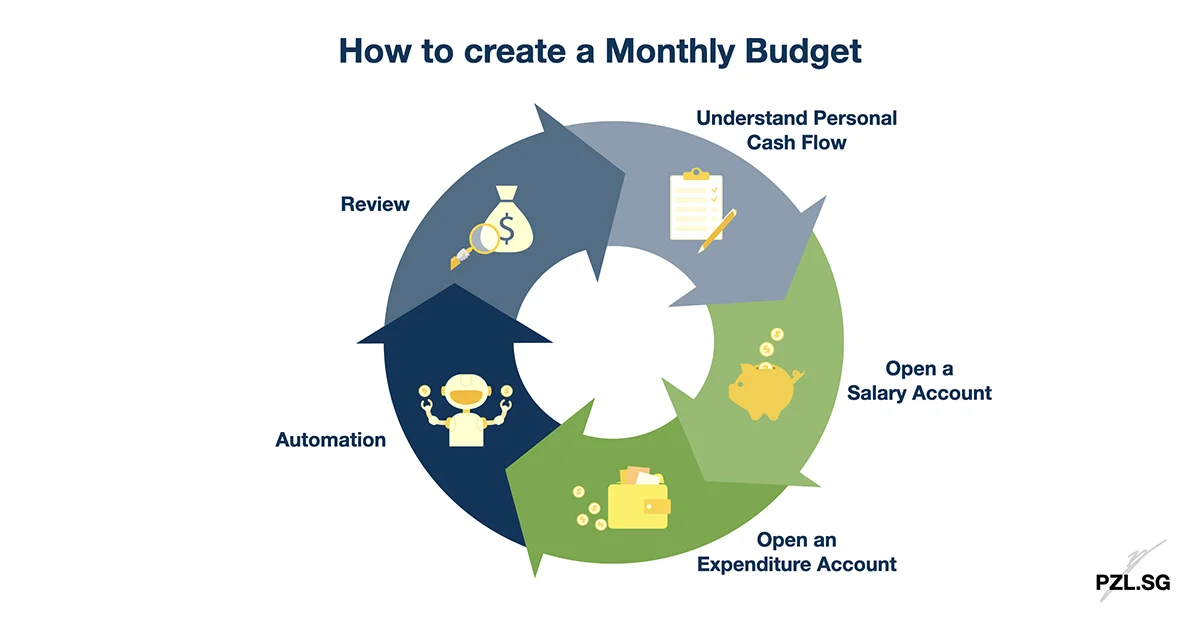

Part 3: How to create a Monthly Budget

Now that we have a better understanding on a monthly budget and what it can do for you, let me share my strategy with you.

Step 1: Understand Personal Cash Flow

Firstly, we need to understand your personal cash flow. Through a proper cash flow analysis, we will check your earning ability and spending pattern. Thereafter, we will make any necessary adjustments so that you can set aside a feasible amount for your monthly budget (this will also form a part of your financial goal).

At the same time, we will set a target on how much to save every month. For example,

- Monthly Salary: $3,000

- Monthly Expenditure: $1,500

- Targeted Savings: $1,500

Step 2: Open a Salary account

Secondly, we will set up your main bank account, which is also known as your salary account. To point out, the main purpose of a salary account is to

- Credit your monthly salary; and

- Build up your targeted savings.

For the most part, the main bulk of your savings (from your financial goal) will be placed in this bank account. Therefore, it will be wise to reap the maximal return by choosing a bank account that gives a higher yield. In general, I have two criteria for this bank account:

- Not too many sub-requirements to earn a higher bank interest; and

- Zero fees to set up a standing instruction (I will elaborate this point in Step 4).

Example: CIMB FastSaver, DBS Multiplier, OCBC 360, Standard Chartered Bonus$aver, UOB One

Step 3: Open an Expenditure Account

Thirdly, we will open a separate bank account for drawdown purposes. To explain, this account is responsible to meet your day-to-day expenses for the entire month. For that reason, I also have two criteria for this bank account:

- Low or zero minimum average daily balance (as this account may run dry at the end of the month); and

- Has an ATM card or a debit card (purely for convenience sake).

Step 4: Automation

As a matter of fact, the best part of creating our monthly budget is to automate it. After all, we have so many tasks to complete everyday. Hence, it is always welcoming to automate the entire budgeting process. Based on the results from the cash flow analysis (in Part 1), we would have a proper grasp on your total expenditure each month.

After making any necessary adjustments (e.g. to reduce some lifestyle expenses), we will transfer the required monthly expenses from your salary account to your expenditure account. In detail, I will set up a standing instruction on the first day of the month (or it can be any auspicious day that you like). While optional, there are two more things that we need to do:

- Deactivate the salary account’s internet banking token or app; and

- Cut the salary account’s ATM or debit card.

Under those circumstances, it becomes difficult for you to access the monies in your salary account. As a result, you will be forced to spend within your means (from your expenditure account).

Based on the earlier example (from Step 1), we will set up a standing instruction to transfer $1,500 to your expenditure account on the first day of the month. Meanwhile, the remaining $1,500 will remain in your salary account. A year later, you may expect the total savings in your salary account to increase by $1,500 x 12 = $18,000.

On the other hand, the balance in your expenditure account will likely be zero. However, if you spend less than your allocated budget, then you will have some extra savings in this account too!

Step 5: Review Your Budget

Finally, set aside a time to review your budget on a consistent basis (e.g. every quarter). For one thing, this is a good opportunity to evaluate your earning ability, as well as your spending pattern. Furthermore, we will also track your progress towards your financial goals. If you do it (the monthly budget) right, then you should have two sets of savings:

- A fixed amount in your salary account that grows at the end of each month; and

- Any unspent amount from your expenditure account.

In the light of these reviews, you will learn to live within your means. This is particularly important if you tend to have the temptation to spend more whenever you see more money in the bank.

What happens to the money in your salary account?

As I have noted earlier, you have set aside this money to meet your financial goals.

What happens if there is a positive balance in the expenditure account?

On this occasion, you don’t really have to keep this money. In fact, you can splurge and buy anything that you like. This is because you deserve to be rewarded for spending lesser than expected!

Part 4: Final Thoughts

In order to create an effective budget, we need two attributes,

- A clear understanding of your cash flow; and

- The discipline to distinguish between a need and a want.

Eventually, it is not about how much we earn. In truth, it is how much we save that matters.

A budget is telling your money where to go instead of wondering where it went. – Dave Ramsey

First Published: 7 August 2019

Last Updated: 10 November 2021

Leave a Reply