Overall, the illustrated investment rate of return provides insights into the projected returns for your participating policy. While this may be true, you must remember that these numbers are for illustrative purposes only. In other words, the insurer reserves the rights to adjust the figures subsequently. Be that as it may, let’s understand how the illustrated investment rate of return works in this post.

Table of Contents:

- What is a Participating Policy?

- Illustrated Investment Rate of Return

- Life Insurance Association Singapore’s Guidelines

- Illustrated Yield at Maturity

- Choosing a Participating Fund

One Minute Summary:

- If you are holding onto a participating policy, then you will share the profit generated from the participating fund’s return.

- Above all, Life Insurance Association Singapore (LIA) sets the guidelines on how to derive the illustrated investment rate of return.

- Accordingly, the respective life insurers must follow this approach and ensures that the illustrated rates do not exceed the upper illustration cap.

- In any case, the illustrated investment rate of return is merely a simulation.

- As a result, what’s more important is the participating fund’s stability to provide the promised rate of return over time.

Part 1: What is a Participating Policy?

To sum up, a participating policy is a policy that shares in the divisible surplus of the insurer’s participating fund. In detail, the insurer will pool your premium together with the rest of the policyholders. Thereupon, the insurer will invest this pool of money into its participating fund. In the same way, you will also share the participating fund’s risks (together with the rest of the policyholders).

On the whole, the participating fund’s objective is to provide stable returns in the medium to long-term. In time to come, you may receive a portion of these returns in the form of guaranteed benefits and non-guaranteed bonuses.

Part 2: Illustrated Investment Rate of Return

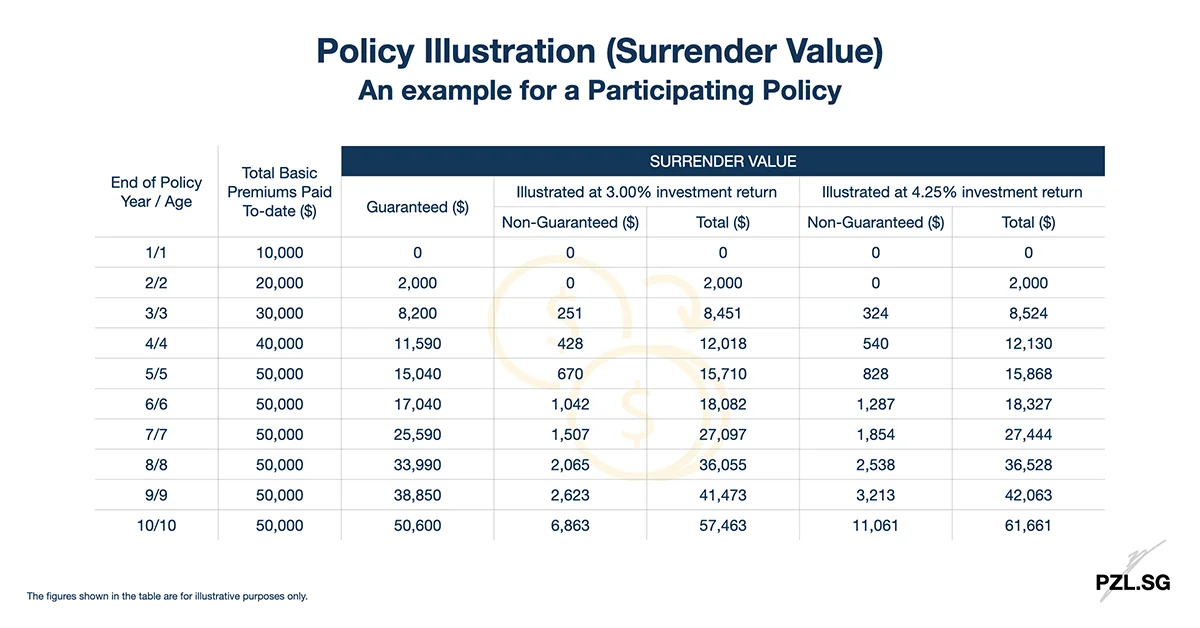

Altogether, the illustrated investment rate of return provides an overview to the projected policy benefits at different time periods. With this purpose in mind, the insurer will prepare the policy illustration based on two scenarios for the participating fund’s investment rates of return, i.e.

- An upper investment return scenario; and

- A lower investment return scenario.

After all, the bonuses in a participating policy are non-guaranteed. Hence, the two scenarios depict the volatility and portray a reasonable gauge on the potential benefits. It is important to realise that the insurer’s illustration rates shall not be higher than its view on the achievable investment returns over the lifetime of its participating policies.

Part 2.1: How to determine the non-guaranteed benefits?

Given that participating fund’s asset allocation, the insurer will calculate the expected return for each asset type. To that end, the insurer will set relevant assumptions about the

- Expenses;

- Mortality and morbidity rates; and

- Policy termination rates.

In any case, the insurer shall avoid using a basis that will lead to a higher illustrated value as compared to the results from using the best estimate assumptions. Moreover, the best estimate assumptions should be consistent with those used in the latest actuarial investigations.

Part 2.2: Is the investment performance fixed at the upper or the lower limit?

In a word, neither. In fact, the upper illustration rate and the lower illustration rate are purely for illustrative purposes only. To put it another way, neither rates represent the upper or lower limits of the investment performance of the insurer’s participating fund. Evidently, the participating fund’s actual performance will depend on its actual experience (as mentioned in Part 2.1). In detail, you may refer to the insurer’s participating fund update for that year.

Part 2.3: How will the illustrated investment rate of return change in the future?

Without a doubt, nobody is able to predict the future economic conditions and the participating fund’s actual performance. As a result, the participating fund may generate a higher or lower expected return over the lifetime of the participating policy. Eventually, the actual returns (that you receive) may be higher or lower than those reflected in the policy illustration.

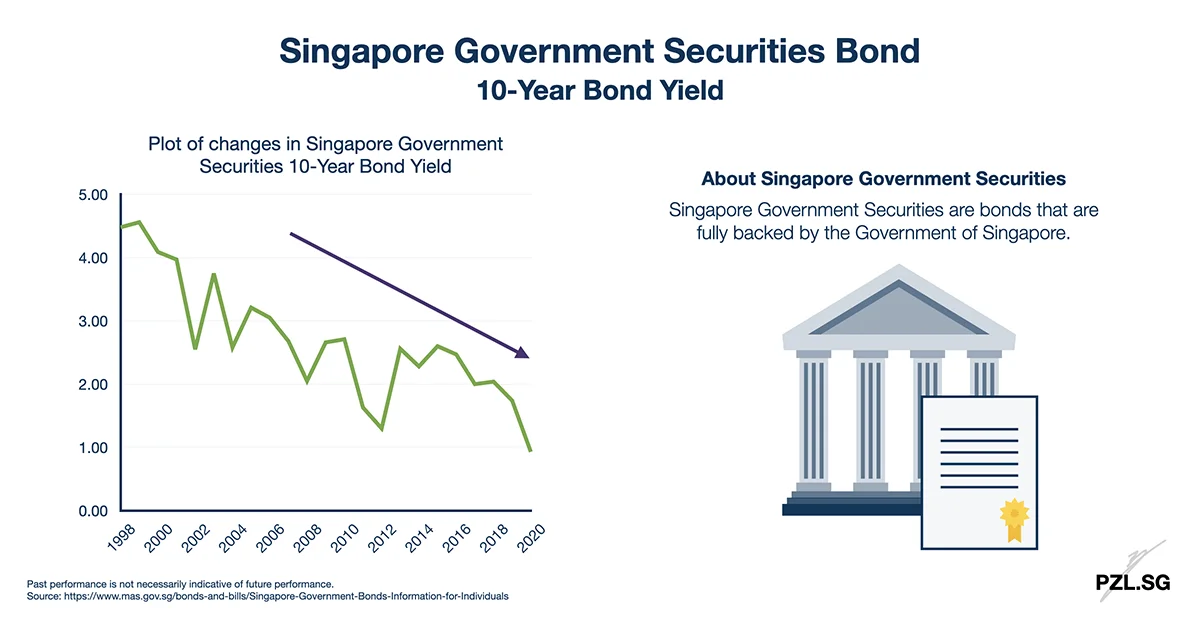

To demonstrate, the bond yield has been decreasing over the years. Consequently, this inflicted damage on the investment returns for the fixed income instruments. As most of the participating funds place an emphasis on bonds, this is certainly a point for concern.

Despite that, the investment climate may improve in the long run. When the investment returns are consistently higher than expected, the insurer may improve its bonus rates as well. After all, there exists an incentive for the insurance company to provide a higher return to you. This is because of the regulatory requirements. In detail, there is a 9:1 ratio on policyholders to shareholders’ distribution. In other words, for every $9 given to the policyholder, the shareholder will receive $1.

Part 3: Life Insurance Association Singapore’s Guidelines

By and large, Life Insurance Association Singapore (LIA) sets the guidelines on how to derive the illustrated investment rate of return. Emphatically, this ensures fairness as the respective insurers will use a consistent approach to prepare their policy illustrations. Generally, the presented illustrated rates are net of any investment expenses.

At this time (effective from 1 July 2021), LIA has set the maximum long-term illustrated investment rate of return at 4.25% per annum. If the product or the bonus series is unable to support this maximum higher rate, then the insurer shall not proceed to illustrate at 4.25% per annum. Meanwhile, the lower rate must be at least 1.25% lower than the higher rate, i.e. 3.00% per annum.

Part 3.1: How to determine the cap for the illustrated investment rate of return?

In brief, Life Insurance Association Singapore takes into account several factors, e.g.

- The participating fund’s asset class mix (e.g. bonds, equities);

- The long-term returns on each asset class.

Additionally, LIA takes into account the combination of the historical asset class performance, as well as the recent and potential future global economic market dynamics and outlook.

Part 3.2: What if the insurer’s projected best estimate for the investment return exceeds LIA’s cap for the upper illustration cap?

On this occasion, the insurer will only be able to present the policy illustration at LIA’s cap, and not above the upper illustration cap. Otherwise, the insurer must highlight the deviation and provide a clear explanation to justify why it has chosen to illustrate at bonus rates which are higher than the prevailing rates.

Part 3.3: How often does LIA review the illustrated investment rate of return?

All in all, Life Insurance Association Singapore reviews the higher illustrated investment rate of return once every three years. Of course, LIA may conduct ad-hoc surveys in between the periods on a needs basis.

Part 4: Illustrated Yield at Maturity

Summing up, the illustrated yield at maturity represents the annualised investment return that you may receive upon the policy’s maturity. In like manner, this yield is net of the cost of insurance and the incurred expenses.

For this purpose, the insurer will use the participating fund’s illustrated investment rate of return at 3.25% p.a. and 4.75% p.a. to calculate the yield at maturity. As I have noted earlier, this two illustrated investment rate of return do not represent the upper and lower limits of the participating fund’s performance. By the same token, the calculated yield do not represent the upper and lower limits of the yields that you may receive at maturity. Instead, the insurer will inform you (annually) on the actual bonus rates for your participating policy for that year.

Part 4.1: Illustrated Yield at Maturity for an Endowment Plan

In this case, the policy illustration will show the total illustrated yield at the endowment plan’s maturity date. For example,

Based on the Illustrated Investment Rate of Return of 2.75% p.a., your total Illustrated Yield at maturity is 3.50% p.a.

Accordingly, you can compare the illustrated yield at maturity with the returns of Singapore Savings Bonds and Singapore Government Securities. Thereafter, you may evaluate the suitability of having a participating policy in your financial portfolio.

Part 4.2: Illustrated Yield at Maturity for a Whole Life Plan

In this situation, the policy illustration will show the total illustrated yield upon the surrender age at either

- Entry Age + 40 years; or

- Age 65, whichever later.

For instance, let’s take the case of an insured who is 25 years old.

Based on the Illustrated Investment Rate of Return of 4.25% p.a., your total Illustrated Yield upon surrender at age 65 is 2.64% p.a.

In similar fashion, this helps you to ascertain the value of your dollar in a participating whole life insurance policy.

Part 5: Choosing a Participating Fund

It must be remembered that the illustrated investment rate of return is not your actual return. To clarify, the illustrated investment rate of return is merely a simulation of the participating fund’s performance. In truth, nobody knows for sure whether the participating fund is capable of achieving such returns consistently every year.

All things considered, one of the common goals is to invest into the right participating fund. To be sure, you may determine the participating fund’s stability by analysing its financial condition and the actual value of the assets. Furthermore, you need to ensure that the fund incurs a reasonable level of expenses. This is so as to meet its obligations without too much financial distress.

Additionally, you should also take note on the rate of declared bonuses, alongside with its compounding rate over time. Finally, proven track records ensure that the insurance company is capable to implement smoothing of bonuses effectively.

Leave a Reply