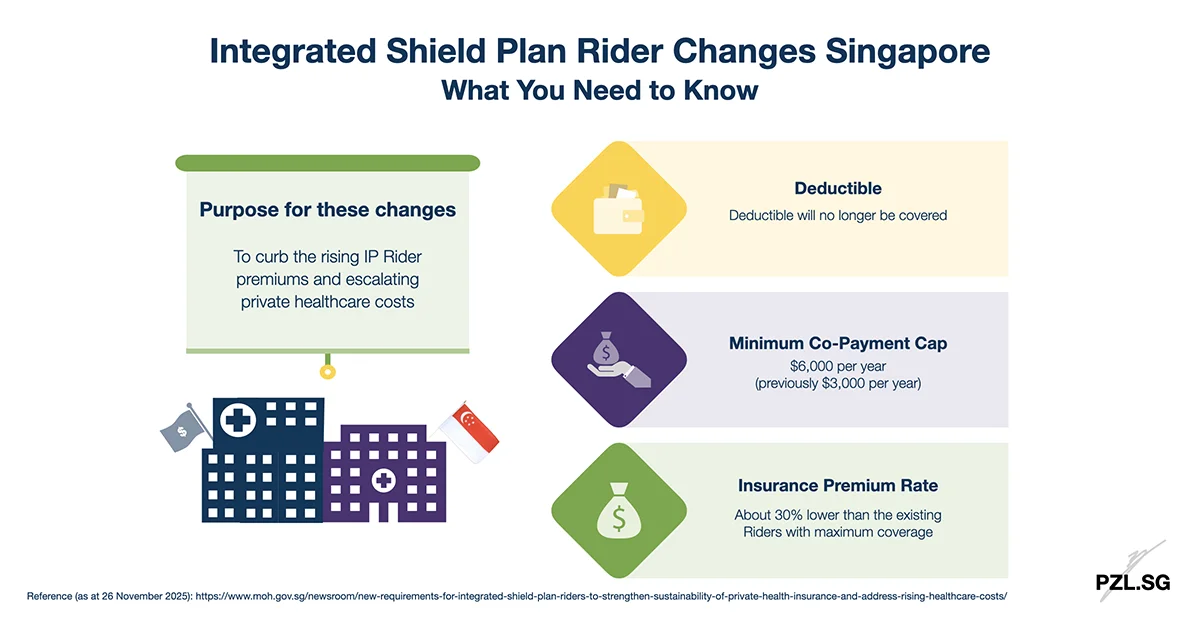

From April 2026, new Integrated Shield Plan Riders in Singapore will no longer cover the deductible portion of your medical bill. In addition, the minimum co-payment cap will increase from $3,000 to $6,000 per policy year. These changes affect how much you pay out-of-pocket when you are hospitalised. With this in mind, let’s go through these changes and understand and what they means to you.

🎥 Prefer watching? Check out the video version of this post.

Table of Contents:

- What is an Integrated Shield Plan

- What is an Integrated Shield Plan Rider

- New Requirements for the Integrated Shield Plan Riders

- Will The Upcoming Changes Affect You?

- Why is MOH Making These Changes?

- Considerations When Reviewing Your Health Insurance

- Final Thoughts

One Minute Summary:

- From April 2026, new Riders will no longer cover the minimum IP deductibles.

- In addition, the minimum co-payment cap will increase from $3,000 to $6,000 per policy year.

- With lower coverage, the new IP Riders are expected to be 30% cheaper than the current ones with maximum coverage.

- As an existing policyholder (before 27 November 2025), you are not affected by this change. Wait for the insurers to provide a further update.

- If you purchase an IP Rider during the transition period (between 27 November 2025 and 31 March 2026), you will transit to the new riders no later than April 2028.

Part 1: What is an Integrated Shield Plan

An integrated shield plan is a private health insurance scheme that provides reimbursement for hospital bills and selected outpatient treatments. These plans are typically used to cover non-subsidised medical bills. That is, bills that you incur at

- Class B1 wards at public hospitals,

- Class A wards at public hospitals, or

- Standard room at private hospitals.

With an integrated shield plan, you will pay for the deductible and co-insurance component of the eligible medical bill. In detail,

- The deductible is a fixed cost of up to $3,500 per policy year, depending on your ward class.

- The co-insurance is 10% of the remainder of the medical bill (after taking the deductible into account).

Part 2: What is an Integrated Shield Plan Rider

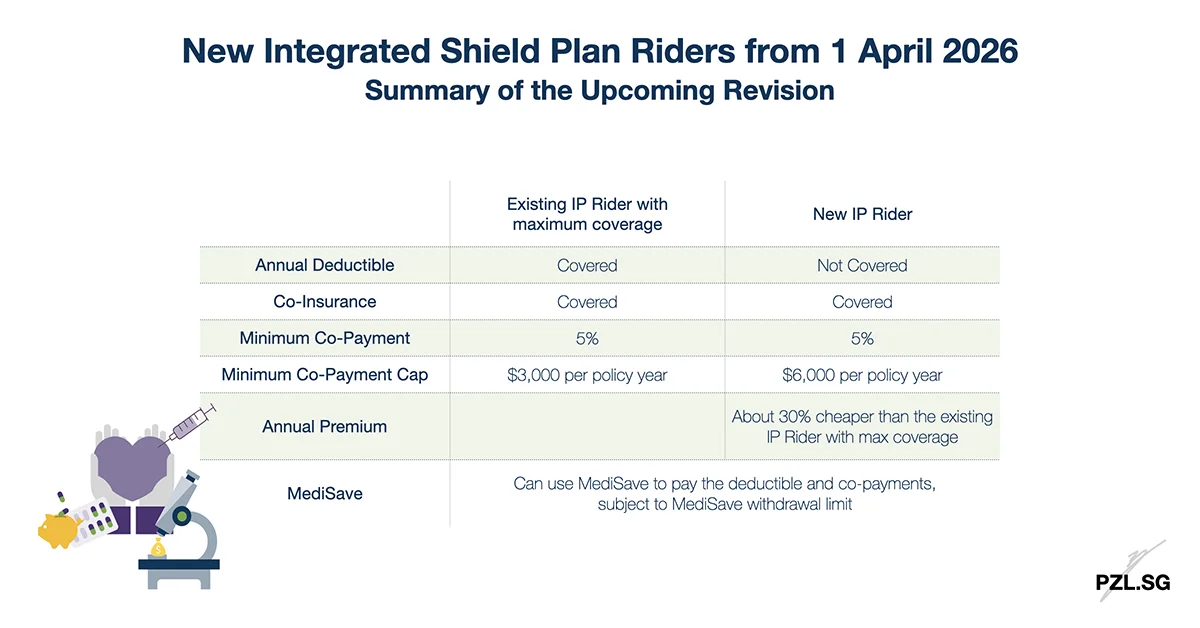

An Integrated Shield Plan Rider (“IP Rider”) is an optional add-on to your main Integrated Shield Plan (“Main IP”). It helps to reduce the out-of-pocket expenses by covering the deductible and co-insurance component of the eligible medical bill. Under those circumstances, you will pay the co-payment component instead. Most insurers offer riders that allow you to pay a 5% co-payment, capped at $3,000 per policy year.

Part 3: New Requirements for the Integrated Shield Plan Riders

The Ministry of Health (MOH) is introducing three major changes to IP Riders to address the rising private healthcare costs and insurance premiums:

- Removal of the deductible coverage

- Increase in the co-payment cap

- Reduction in the insurance premiums rates

Let’s explore each change in detail.

Part 3.1: Removal of the deductible coverage

At present, many IP Riders cover the deductible – the “first portion” of the hospital bill that you must pay before insurance kicks in.

From 1 April 2026, new IP Riders cannot cover the minimum Main IP deductibles. This change aims to encourage more responsible healthcare usage.

Table: Minimum IP deductibles set by the Ministry of Health, Singapore

| Targetted Coverage of Your Main IP | Ward Class that You stayed in | Minimum Deductible (Lower of Target Main IP Coverage or Ward Class) |

|---|---|---|

| Class A / Private | Class A / Private | $3,500 |

| Class B1 | Class B1 | $2,500 |

| Class B2 | Class B2 | $2,000 |

| Class C | Class C | $1,500 |

| Outpatient | NA | NA |

| Day Surgery / Short Stay Wards | Non-Subsidised | $2,000 |

| Day Surgery / Short Stay Wards | Subsidised | $1,500 |

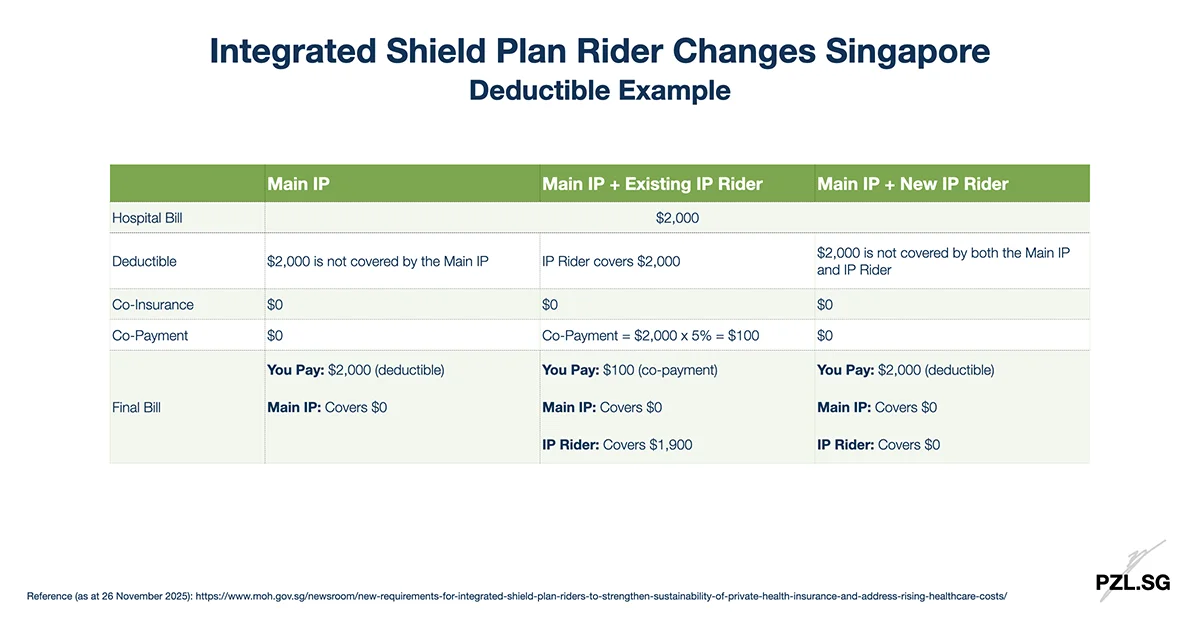

To illustrate the impact, let’s study the following example together:

If you have an integrated shield plan only, you will continue to pay the full deductible amount. In other words, you are not affected by the upcoming new requirements.

If you have an integrated shield plan with an existing IP Rider, the IP Rider will cover the $2,000 incurred under the Main IP. In this case, you will pay a 5% co-payment, or $100.

If you have an integrated shield plan with the new IP Rider, you will need to pay the full deductible amount. As the IP Rider no longer covers the deductible component, you are affected by the upcoming new requirements.

Part 3.2: Increase in the Co-Payment Cap

At present, many IP Riders cap your annual co-payment at $3,000.

From 1 April 2026, the minimum co-payment cap will increase to $6,000 per year. This aligns with rising healthcare costs and larger bill sizes.

To illustrate the impact, let’s study another example together:

If you have an integrated shield plan only, you will pay:

- Deductible of $3,500, and

- Co-Insurance of $19,650.

In this case, the Main IP will cover $176,850 of the medical bill.

If you have an integrated shield plan with an existing IP Rider, you will pay:

- Co-Payment of $3,000 (assuming that the co-payment cap applies).

In this case, the Main IP will continue to cover $176,850 of the medical bill while the IP Rider will cover $20,150.

If you have an integrated shield plan with the new IP Rider, you will pay:

- Deductible of $3,500, and

- Co-Payment of $6,000 (assuming that the co-payment cap applies).

In this case, the Main IP will still cover $176,850 of the medical bill while the IP Rider will cover $13,650.

As can be seen, the new IP Rider covers a smaller portion of the medical bill. This is as compared to the existing IP Rider.

Part 3.3: Reduction in the Insurance Premium Rates

Since the new IP Riders provide lower coverage, the premiums will become more affordable. According to Ministry of Health, it estimates that you will enjoy around 30% premium savings on average. This translates to around

- $600 in annual savings for private hospital rider policyholders

- $200 in annual savings for public hospital rider policyholders.

Older policyholders may benefit more due to higher existing premium rates.

Part 4: Will The Upcoming Changes Affect You?

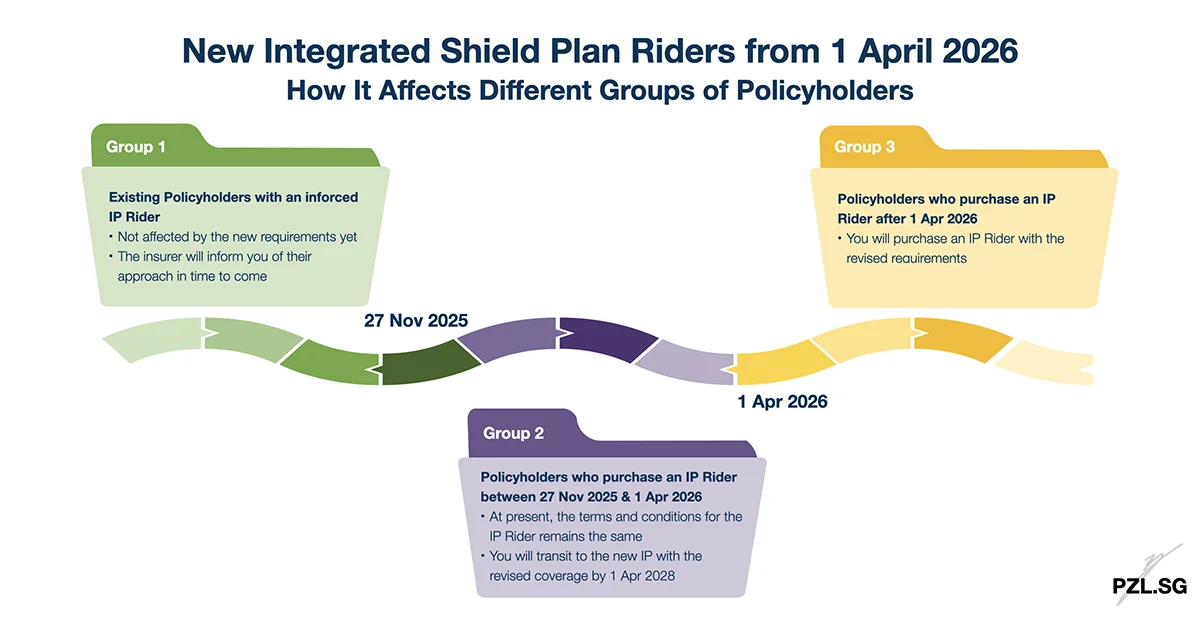

There are three groups of policyholders who may be affected by this change.

Group 1: You have an existing IP Rider before 27 November 2025

If you have an existing rider, your contract with the insurer remains valid. As a result, you are not affected for now. Your insurer will review and inform you if changes are needed. With this in mind, relax, as there is nothing for you to do at this moment.

Group 2: Policyholders who purchase an IP Rider between 27 November 2025 and 31 March 2026

You can still get the current version of the IP Rider. Generally, these riders will cover the deductible and cap the co-payment at $3,000 per policy year. However, you will transit to the new IP Rider by April 2028.

Group 3: Policyholders who purchase an IP Rider from 1 April 2026

You will purchase an IP Rider that complies with the new requirements. The new IP Rider offers lower coverage, at a more affordable premium rate.

Part 5: Why is MOH Making These Changes?

Currently, the IP Riders offer very generous coverage. Often, patients pay little or nothing because MediSave covers the out-of-pocket cost. This leads to higher claims, rising private healthcare costs, and even higher chances of unnecessary treatments. As a result, insurance premiums increase as well.

According to the data from the Ministry of Health, private IP policyholders with riders are 1.4 times more likely to make a claim. Moreover, their average claim size is also 1.4 times higher than those without riders. These trends make the system increasingly unsustainable.

Through the upcoming revision, MOH aims to

- Keep health insurance affordable,

- Reduce over-consumption (“buffet syndrome”), and

- Enable the health insurance to focus on large bills, not minor ones.

Part 6: Considerations When Reviewing Your Health Insurance

Now, I believe it is a good time to reassess whether your existing health insurance policy still suits your needs.

Part 6.1: MediShield Life vs Integrated Shield Plan

- What is your healthcare expectation? Are you comfortable with Class B2/C wards at public hospitals?

- Do you want to choose your own specialist?

- Do you prefer shorter waiting times?

- Can you afford the higher premium rates in the long run, especially in old age?

- Do you have any medical conditions or family history of major illnesses?

MediShield Life is designed to cover large subsidised bills incurred for hospitalisations in Class B2/C wards in public hospitals. If you have a higher healthcare expectation, you may wish to consider an integrated shield plan. Here are two articles to help you evaluate whether MediShield Life offers enough coverage, and whether you should purchase an integrated shield plan:

Part 6.2 Integrated Shield Plan only vs Main IP with Rider

- Can you comfortable afford the $3,500 deductible and 10% co-insurance?

- Do you prefer predictable medical costs?

- Do you frequently use private or unsubsidised care?

- Can you sustain the IP Rider premium in the long run?

If you have only the Main IP, you will need to pay for the deductible and co-insurance component of the medical bill. Together with the IP Rider, you only need to pay the co-payment component of the medical bill. This amount is always lesser than the sum of the deductible and co-insurance. Here is an article to help you evaluate whether you should purchase the rider for the integrated shield plan.

Part 6.3: Existing IP Rider vs New IP Rider

- Can you handle the $3,500 deductible?

- Are you willing to accept the higher co-payment cap of $6,000?

- Do you want to save on insurance premium?

- How important is ‘absolute peace of mind’ compared to affordability?

With the existing IP Rider, your maximum out-of-pocket cost in a policy year is $3,000. Meanwhile, for the new IP Rider, your maximum out-of-pocket cost in a policy year is $9,500.

Part 7: Final Thoughts

The upcoming revision to Integrated Shield Plan Riders mark an important shift in Singapore’s private health insurance landscape. By reducing coverage, MOH attempts to untie the knot to balance the needs of patients, insurers, and healthcare providers.

While lowering premiums may benefit many, it remains to be seen whether these adjustments will truly slow the long-term rise of private healthcare cost. A similar move in 2018 (introducing the mandatory co-payment) did not fully resolve the issue. So, will another baby step untangle this knot?

Nevertheless, for now, take this opportunity to review your hospitalisation plan to ensure it aligns with your healthcare expectations and long-term affordability.

Leave a Reply