When it comes to building a robust medical safety net, MediShield Life forms the foundation of your healthcare coverage in Singapore. However, with rising healthcare costs and escalating premiums for private Integrated Shield Plans (IPs), a question I hear increasingly often is, “is it actually possible to rely on MediShield Life alone?”

This is a valid concern, especially if you are balancing your current cash flow with future retirement security. You want protection, but you don’t want to overpay for insurance you might not need. In this article, we will evaluate MediShield Life’s coverage and limitations to help you make an informed, sustainable decision about your healthcare planning.

Table of Contents:

- What is MediShield Life

- What does MediShield Life cover?

- What is not covered by MediShield Life?

- Case Studies

- When MediShield Life may be enough

- When MediShield Life may NOT be enough

- Considerations When Reviewing Your Health Insurance

- Final Thoughts – Is MediShield Life enough?

One Minute Summary:

- MediShield Life is Singapore’s national health insurance scheme that protects you from large hospital bills in public healthcare institutions.

- It does not cover 100% of medical bills. Instead, it imposes sub-limits, deductibles, and co-insurance to keep premiums sustainable. These out-of-pocket cost can be paid using MediSave or your cash savings.

- Generally, MediShield Life may be sufficient if you are comfortable with subsidised care, prioritise affordability, and have sufficient savings to pay for the deductible and co-insurance.

- On the other hand, MediShield Life may not be enough if you prefer comfort and privacy, want speed and choice, or have limited savings.

- If you want more comprehensive coverage, an Integrated Shield Plan offers more healthcare options.

- When reviewing your health insurance, consider the benefits and costs to find one that offers peace of mind and is sustainable in the long run.

Part 1: What is MediShield Life

MediShield Life is a basic health insurance scheme that covers all Singapore Citizens and Permanent Residents. It is designed to help cover 9 in 10 subsidised bills in public healthcare institutions. MediShield Life is structured so that the deductible and co-insurance components can be paid using your CPF MediSave. This minimises that needs to be paid in cash.

Key features of MediShield Life:

- Automatic Coverage: Automatically covers all Singaporeans and Permanent Residents

- Universal Protection: Offers coverage for life, regardless of age or pre-existing conditions

- Affordable: Premiums can be fully paid using CPF MediSave

- Targeted Design: Primarily for subsidised care in public hospitals

MediShield Life is not meant to be comprehensive. Instead, it is designed to be universal, affordable, and more importantly, sustainable.

Part 2: What does MediShield Life cover?

Some of the core benefits MediShield Life provides include:

- Inpatient Hospitalisation: Coverage for Class B2 and C wards in public hospitals

- Surgical Procedures: Covers surgeries and approved treatments

- Costly Outpatient Treatments: Includes kidney dialysis, chemotherapy, and radiotherapy

- Cancer Drugs: Covers treatments and services listed on the Cancer Drug List (CDL)

That said, MediShield Life is not designed to provide absolute peace of mind by covering 100% of medical costs. Instead, it imposes

- Sub-limits by treatment types

- Annual claim limits

- Deductibles and co-insurance

These measures are in place to keep the MediShield Life premiums sustainable.

Part 3: What is not covered by MediShield Life?

Part 3.1: Pro-Ration Factor (The “Hidden” Cost)

The pro-ration factor affects how much of your bill MediShield Life considers when calculating your claim. The actual factor ranges between 10% and 100% (the latter means MediShield Life will take the entire bill into consideration for its claim computation).

Factors that affect the pro-ration factor:

- Your citizenship (Whether you are a Singapore Citizen or a Permanent Resident)

- Selected ward class

- Inpatient or outpatient treatment

- Type of treatment

Examples for Pro-Ration Factor:

- Singaporean in Class C ward: 100% of the bill is considered for claim computation

- Singaporean in Class A ward: 27% of the bill is considered for claim computation

- Singapore PR in Class C ward: 50% of the bill is considered for claim computation

As shown above, for Permanent Residents, a pro-ration factor applies even in subsidised wards. This means for a $10,000 bill, at least $5,000 needs to be paid using MediSave or cash savings.

Generally, a pro-ration factor applies when there is a mismatch in healthcare expectations. This is because MediShield Life payouts are pegged to subsidised bills. When you choose to upgrade to a higher ward class, your bill increases while MediShield Life coverage decreases.

Part 3.2: Deductible (The “Entry Fee”)

After accounting for the pro-ration factor (if applicable), the deductible is the next layer of cost you must pay before coverage provided by MediShield Life begins. This is a fixed amount that applies in each policy year. The actual amount ranges between $1,500 and $4,500.

Factors that affect the deductible amount:

- Your age next birthday

- Ward class

- Type of treatment

Examples for Deductible:

- Class C Ward (Age 80 and below): $2,000

- Class B2 Ward (Age 80 and below): $2,500

Let’s assume the hospital bill in a Class C ward is $3,000. In this case, you will need to pay a deductible of $2,000. MediShield Life will then consider the remaining amount for claim computation.

Meanwhile, if the bill is $500, you will need to pay the full amount. This is because this amount is less than the annual deductible.

As shown, the deductible primarily affects small medical bills. This is because MediShield Life is designed to cover the large bills, not the small ones.

Part 3.3: Co-Insurance (Sharing the Bill)

After meeting the deductible, you split the remaining bill with the insurer through co-insurance. The co-insurance is payable on each claim.

Factors that affect the co-insurance:

- Size of the bill

- Inpatient or outpatient treatment

Breakdown for the Co-Insurance (Inpatient / Day Surgery):

- First $5,000 (inclusive of deductible): 10%

- Next $5,000: 5%

- Above $10,000: 3%

Let’s assume the hospital bill at Class C ward to be $3,000.

- Deductible = $2,000

- Bill after deductible = $3,000 – $2,000 = $1,000

- Co-Insurance = $1,000 x 10% = $100

MediShield Life covers the remaining bill of $900 (take $3,000 – $2,000 – $100).

Co-insurance applies to every claim to encourage responsible healthcare usage.

Part 3.4: Pre- and Post-Hospitalisation

MediShield Life has limited coverage for expenses before and after your hospital stay. For example, it does not cover

- Pre-admission diagnostics

- Post-discharge follow-up outpatient care

Part 3.5: Experimental and Non-Standard Treatments

In general, MediShield Life excludes experimental treatments and non-standard therapies.

Since 1 September 2022, MediShield Life only covers cancer drugs listed on the Cancer Drug List (CDL). This list comprises cancer drug treatments that are deemed clinically proven and cost-effective. If you opt for advanced immunotherapies or experimental drugs not on this list, you would need to pay these costs yourself.

Part 3.6: Claim Limits

MediShield Life has claim limits that vary by treatment type. For example, for surgical procedures, the claim limit is between $240 to $3,900, depending on the complexity of the procedure. There is also an overall claim limit of $200,000 per policy year.

Part 4: Case Studies

Let’s simulate how MediShield Life claims work in the real world using two common conditions:

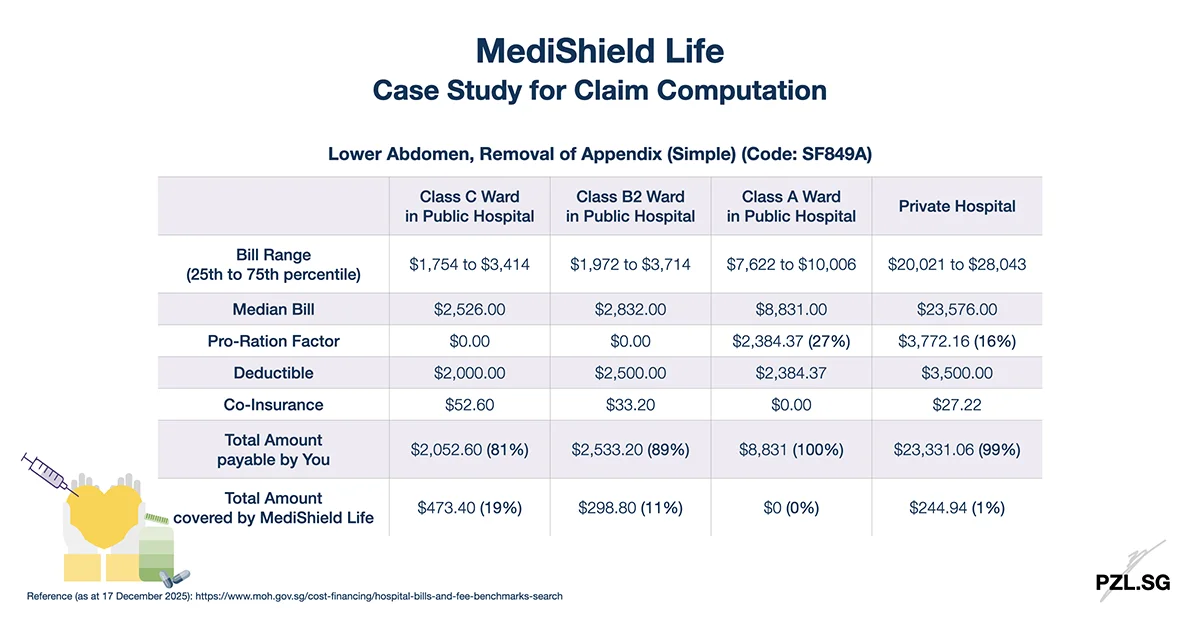

- Lower Abdomen, Removal of Appendix (Simple) (Code: SF849A)

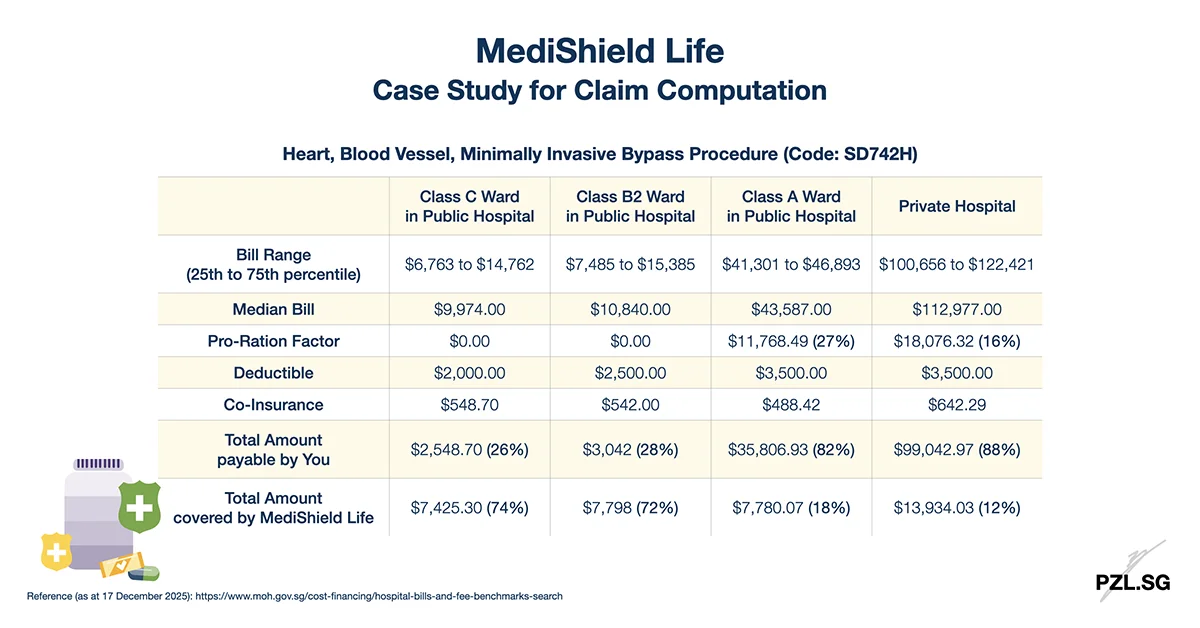

- Heart, Blood Vessel, Minimally Invasive Bypass Procedure (Code: SD742H)

Part 4.1: Lower Abdomen, Removal of Appendix (Simple) (Code: SF849A)

Let’s start with the appendix removal, a relatively simple and common emergency procedure.

Observations from this case study:

- Under subsidised care (Class B2/C ward), the bill size is relatively small (median bill is less than $3,000).

- Since the bill size is relatively small, the deductible will make up the majority of this bill. This means you will end up paying the majority of the cost.

- If you seek treatment under non-subsidised care, the pro-ration factor will make up the majority of the bill. This also means most of the bill becomes your responsibility.

Conclusion from this case study:

- MediShield Life is designed to cover large medical bills, not the small ones. The deductible works as expected to encourage you to take care of the more manageable bills.

- MediShield Life is designed to cover subsidised care. The pro-ration factor works as expected to adjust the claimable amount when you opt for non-subsidised care.

Part 4.2: Heart, Blood Vessel, Minimally Invasive Bypass Procedure (Code: SD742H)

Next, let’s examine the claim computation for bypass surgery, the most common form of heart surgery in Singapore.

Observations from this case study:

- Under subsidised care (Class B2/C ward), the bill size is larger (median bill costs more than $9,000).

- After accounting for the deductible, MediShield Life kicks in to cover the majority of the bill.

- If you seek treatment under non-subsidised care, the pro-ration factor will make up the majority of the bill. This also means you will end up paying the majority of the cost.

Conclusion from this case study:

- MediShield Life works as designed to cover the majority of the bill (at least 70% covered).

- MediShield Life is designed to cover subsidised care. The pro-ration factor works as expected to adjust the claimable amount when you opt for non-subsidised care.

Part 4.3: Key Takeaways from Both Case Studies

- Simple procedures can cost more than complex ones if non-subsidised.

- For small subsidised bills, you are likely to pay the majority of the bill (through the deductible).

- For larger subsidised bills, MediShield Life works as expected to cover the majority of the bill.

- For non-subsidised care, MediShield Life covers a smaller portion of the bill. This is regardless of the bill size.

These observations confirm that MediShield Life works exactly as designed.

Part 5: When MediShield Life may be enough

MediShield Life may provide sufficient coverage if you

- Are comfortable with subsidised care: You are comfortable staying in a naturally ventilated ward shared with 5 to 7 other patients.

- Are willing to wait for non-urgent care: You are willing to rely heavily on standard polyclinic referrals and subsidised specialist queues, where wait times can be longer.

- Prioritise affordability: You want your health insurance to be fully paid using your MediSave and to avoid paying cash for the insurance premium.

- Accept “team-based” care: You trust the hospital’s assigned medical team and do not need to choose a specific surgeon.

- Have medical sinking fund: You have set aside savings to cover the annual deductible and co-insurance.

- Accept standard, cost-effective treatments: You are comfortable with treatments that are medically proven to be effective.

Part 6: When MediShield Life may NOT be enough

MediShield Life may not provide sufficient coverage if you

- Are a Permanent Resident: Pro-ration factor applies even for subsidised care.

- Prefer comfort and privacy: You prefer an air-conditioned room or a single room.

- Want speed and choice: You want to skip the subsidised waiting times and choose your preferred specialist.

- Want “full journey” coverage: You want coverage for pre- and post-hospitalisation.

- Have limited savings: You cannot afford a sudden cash outlay for the deductible and co-insurance and prefer an insurance rider to cushion the majority of this out-of-pocket cost.

- Want access to non-standard treatments: You can want the option to access advanced medical treatments, experimental therapies, or procedures that are not covered by MediShield Life.

In these situations, you may wish to consider additional private insurance coverage to bridge the gap between MediShield Life and your healthcare expectations.

An Integrated Shield Plan may offer:

- More choices of wards, e.g. Class A and B1 wards at public hospitals or private hospitals

- Higher claim limits, e.g. up to $2 million

- Pre- and post-hospitalisation coverage, e.g. up to 180 days before admission and after discharge

- Deductible and co-insurance coverage (subject to co-payment)

- Coverage for non-CDL drugs

Although an Integrated Shield Plan offers additional coverage, there are also important trade-offs to consider:

- Higher premium rates, especially when you are older

- Cash payments beyond the MediSave Withdrawal Limit

- Possible exclusions for pre-existing conditions

Part 7: Considerations When Reviewing Your Health Insurance

Rather than asking “Is MediShield Life enough to meet my healthcare needs?”, a better question is, “What type of healthcare experience does MediShield Life cover?” The following table summarises the key factors to consider when you evaluate your health insurance needs:

Part 7.1: The Comparison Matrix – MediShield Life vs Integrated Shield Plan

| Factor | Stick with MediShield Life | Consider an Integrated Shield Plan (IP) |

|---|---|---|

| Ward Class | B2 / C | A / B1 / Private |

| Doctor | Assigned | Choice |

| Waiting Time | Longer | Shorter |

| Pre/Post Care | Not covered | Comprehensive |

| Out-of-pocket Cost | Deductible, Co-Insurance | Deductible and Co-insurance can be covered by IP Rider (subject to co-payment) |

| Long-term cost (premiums) | Low (Can be fully funded via MediSave) | High (Cash portion increases with age) |

| Medical Sinking Fund (cash reserves set aside for healthcare expenses) | Higher amount (for deductible and co-insurance) | Lower amount (for co-payment) |

Part 7.2: The Decision Framework

You may adopt the following decision framework to aid you in your healthcare planning:

- Calculate Your Risk Exposure: Check your MediSave balance and savings. Can you handle unexpected medical bills without stress?

- Review Your Lifestyle, Health Status, and Family History: Are you healthy and leading an active lifestyle? Do any of your family members have serious or chronic conditions?

- Assess Your Healthcare Preference: Imagine long waiting times to see a doctor, and sharing a non-air-conditioned ward with 7 other patients. Are you truly comfortable with this arrangement?

- Evaluate Sustainability: For Integrated Shield Plans, can you afford the premiums during retirement?

- Conduct Regular Reviews: Review your healthcare plan whenever you reach a life stage milestone (e.g. new job, marriage, children).

Part 8: Final Thoughts – Is MediShield Life enough?

MediShield Life’s core purpose is to ensure no Singaporean is denied basic healthcare due to inability to pay. Accordingly, MediShield Life may be sufficient if you are a Singaporean who

- Is comfortable with Class B2 or C wards in public hospitals

- Accepts the limitations on hospital and doctor choice

- Has savings to manage the out-of-pocket expenses like deductible and co-insurance

- Wish to minimise insurance premiums

MediShield Life and MediSave work together with government subsidies to protect you from large hospital bills.

On the other hand, MediShield Life may not be sufficient if you

- Are a Permanent Resident

- Prefer greater privacy, comfort, or specific specialists

- Have limited savings or MediSave balances

- Want broader coverage with minimal out-of-pocket costs

- Have significant health risks or family medical history

- Want to protect your retirement savings from medical expenses

In summary, MediShield Life is the foundation of your medical safety net – but it may not be the finish line. Your goal is not simply to buy the “best” or the “most” coverage available. Over-insuring yourself can be just as dangerous as under-insuring. If you commit to an expensive health insurance plan but cannot afford the premiums during your retirement, you may be forced to terminate the policy when you need it the most.

Similarly, if you under-insure yourself, you could end up depleting your retirement savings to pay medical bills, compromising on treatment choices to save money. Significant out-of-pocket medical expenses can affect your entire family’s financial well-being too.

Ultimately, getting the right healthcare insurance is a balancing act. You need to weigh the benefits and costs to find a sweet spot – one that offers peace of mind and is sustainable in the long run.

Are you on my free weekly newsletter? Each week, I send out exclusive insights on finance and insurance. For instance, in Volume 5 Issue 5, I shared with my readers on how they can afford to pay MediShield Life’s insurance premium till 100 years old. If such content resonates with you, be sure to subscribe!

First Published: 13 February 2019

Last Updated: 17 December 2025

Leave a Reply