By and large, the Life Insurance Association Singapore (“LIA”) sets and reviews the illustrated investment rate of return (“IIRR”) used in the policy illustration for a participating policy. In fact, LIA introduced the caps for the illustrative investment returns in the year 1994 to ensure consistency among the life insurers. Thereafter, the Life Insurance Association Singapore will review the caps annually. This is so as to keep the illustrative investment returns relevant to the prevailing market conditions. With this in mind, let’s understand the downward revision that took place on 1 July 2021.

Table of Contents:

- What is the Illustrated Investment Rate of Return (“IIRR”)

- What are the changes to the IIRR

- Why is there a Revision

- What is the impact to you

- Final Thoughts

One Minute Summary:

- The illustrated investment rate of return (“IIRR”) shows you the projected investment return that you may receive potentially in due time.

- It is important to realise that the IIRR used in a policy illustration is for illustrative purposes only. As a result, the actual returns may differ from what you see on paper.

- While the downward revision may bring about a negative connotation, we won’t know the real impact until the insurer declare its participating fund’s bonus for that year.

Part 1: What is Illustrated Investment Rate of Return (“IIRR”)

To begin with, let’s recall what is the illustrated investment rate of return (“IIRR”). In general, you will encounter this term whenever you look at a participating whole life insurance policy, or an endowment plan. Overall, the IIRR provides an overview to the projected policy benefits at different time periods, e.g. upon the policy’s maturity. Summing up, the insurer will present this information as a table in its policy illustration. In detail, this is based on two scenarios for the participating fund’s investment rates of return, i.e.

- An upper investment return scenario; and

- A lower investment return scenario.

To point out, this is because the bonuses in a participating policy are non-guaranteed. Hence, the two scenarios depict the volatility and portray a reasonable gauge on the potential benefits. It is important to realise that the insurer’s illustration rates shall not be higher than its view on the achievable investment returns over the lifetime of its participating policies.

Part 2: What are the changes to the IIRR

Since 1 July 2021, the Life Insurance Association Singapore made a downward revision to the illustrated investment rate of return. For this purpose,

- The upper illustration rate shall be revised from 4.75% per annum to 4.25% per annum; and

- The lower illustration rate must be at least 1.25% below the upper illustration rate, i.e. from 3.25% per annum to 3.00% per annum.

Emphatically, all the life insurers are required to comply with the downward revision to the caps on the illustrated investment rate of return. Despite that, the insurers may continue to present its policy illustration at the various IIRR that are below the respective two caps.

Part 3: Why is there a Revision

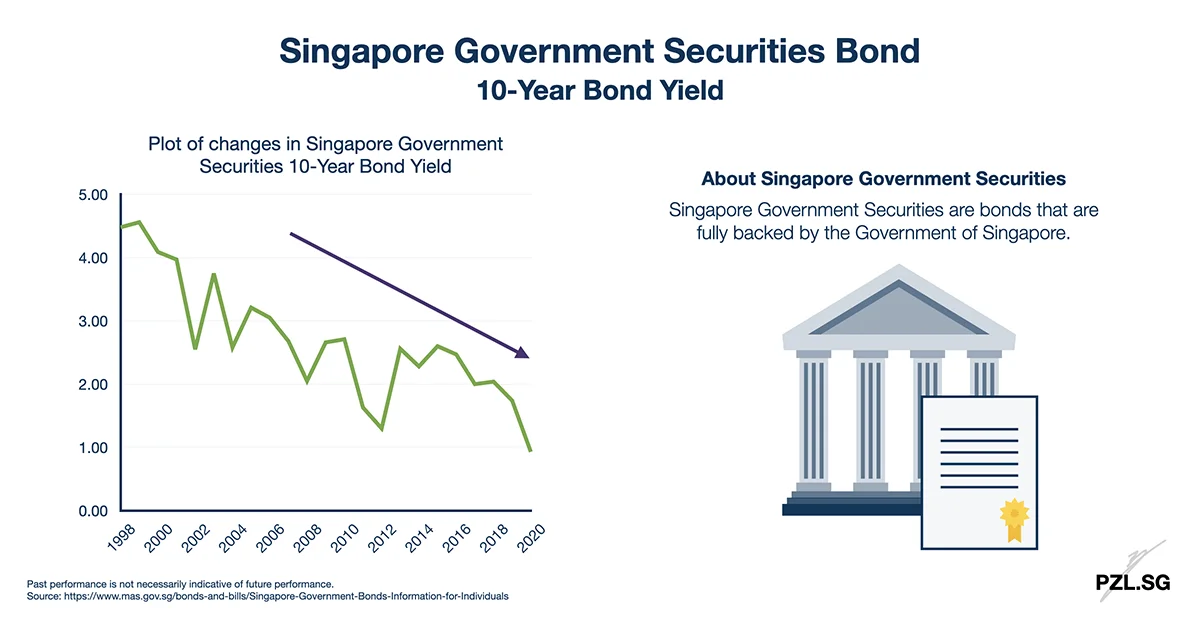

At this time, we continue to live in a sustained low interest rate environment. To demonstrate, the bond yield has been decreasing over the years. Consequently, this inflicted damage on the investment returns for the fixed income instruments. Given that most of the participating funds place an emphasis on bonds, this is certainly a point for concern.

Under those circumstances, the Life Insurance Association Singapore sees the need to make a downward revision to the caps on the illustrated investment rate of return. Thereupon, you will be able to see a more realistic range of projected investment returns for your participating policy.

As a matter of fact, such a revision is not an unseen phenomenon. For example, LIA made another revision in year 2013 where

- The upper illustration rate was revised from 5.25% per annum to 4.75% per annum; and

- The lower illustration rate was designed to be at least 1.5% below the upper illustration rate, i.e. from 3.75% per annum to 3.25% per annum.

Before implementing a revision, the Life Insurance Association Singapore would take its member companies’ views into consideration based on a number of factors. For instance, LIA would study the typical asset class mix that the participating fund invests into. This is together with its historical class performance, as well as on the global economic outlook. Altogether, these data help to determine the assumptions for the long-term returns on each asset class.

Is the Monetary Authority of Singapore (MAS) aware of this revision?

In a word, yes. To clarify, MAS has been informed of the downward revision to the caps on both the upper illustration rate, and the lower illustration rate used in the policy illustration.

Part 4: What is the Impact to you?

For one thing, both the upper illustration rate and the lower illustration rate are purely for illustrative purposes only. To put it another way, neither of the rates represent the upper or the lower limits of the insurers’s participating fund performance. Evidently, the participating fund’s actual performance will depend on its actual experience. In detail, you may refer to the insurer’s participating fund update for that year.

Accordingly, this means that the downward revision would not affect or reflect the actual returns, and/or bonuses for your participating policies. This is regardless of whether it is an existing participating policy, or one that you purchased on or after 1 July 2021. After all, the eventual returns on a participating policy purchased before 1 July 2021 need not necessarily be higher than that of a participating policy that is purchased from 1 July 2021 onwards. While this may be true, some insurers may take this opportunity to review and re-design some of its existing participating policies. As a result, you may observe some adjustments to the new policy’s premium and benefits.

Part 5: Final Thoughts

Above all, nobody likes to see a downward revision to their projected investment return. However, it must be remembered that the figures presented in the policy illustration are for illustrative purposes only. Consequently, there is no way to conclude that the new participating policy (purchased from 1 July onwards) would be worse off. In fact, there were previous episodes when an insurer declared a higher bonus to its policyholders. After all, there exists an incentive for the insurance company to provide a higher return to you. This is because of the regulatory requirements. In detail, there is a 9:1 ratio on policyholders to shareholders’ distribution. In other words, for every $9 given to the policyholder, the shareholder will receive $1.

By the same token, just because you got your participating policy before 1 July 2021 doesn’t mean that you will be in a better position automatically. This is because the insurer may declare a lower rate of bonus following a year of a poor participating fund performance. As I have noted earlier, bonuses are non-guaranteed and the figures that you see in the policy illustration are for illustrative purposes only. Hence, who owns a crystal ball to foresee the future?

Leave a Reply