When it comes to investing, there is a common debate between lump sum investing and dollar cost averaging. In truth, each investment strategy has its own advantages and disadvantages. With this in mind, let’s understand the concept and compare how well they perform against each other.

Table of Contents:

- Guiding Principles

- Understanding the Concept

- When the Price moves Downwards

- When the Price moves Upwards

- When the Price moves Down, then Upwards

- When the Price moves Up, then Downwards

- Lump Sum Investing vs Dollar Cost Averaging

- Real Life Application

One Minute Summary:

- To explain, lump sum investing works on the basis of “buy low, sell high”.

- On the other hand, dollar cost averaging ignores the price fluctuation and market trend in investment.

- In any case, the portfolio must recover eventually in order for you to reap a profit.

Part 1: Guiding Principles

Before going through the illustrations, let’s study the guiding principles behind each strategy.

Part 1.1: Guiding Principles for Lump Sum Investing

To point out, there isn’t anything sophisticated associated with lump sum investing. Generally, you will just strive to “buy low, sell high”.

Part 1.2: Guiding Principles for Dollar Cost Averaging

Altogether, there are three guiding principles:

- Firstly, there is a defined period on which the investment is made, e.g. 10 periods;

- Next, we will invest the same capital during each time period, e.g. $1,000 per period;

- Finally, we will invest on each time period, i.e. no period is skipped or missed.

For that reason, you will invest the same amount of capital on every time period. Emphatically, you will ignore any price fluctuation in the portfolio throughout your investment period.

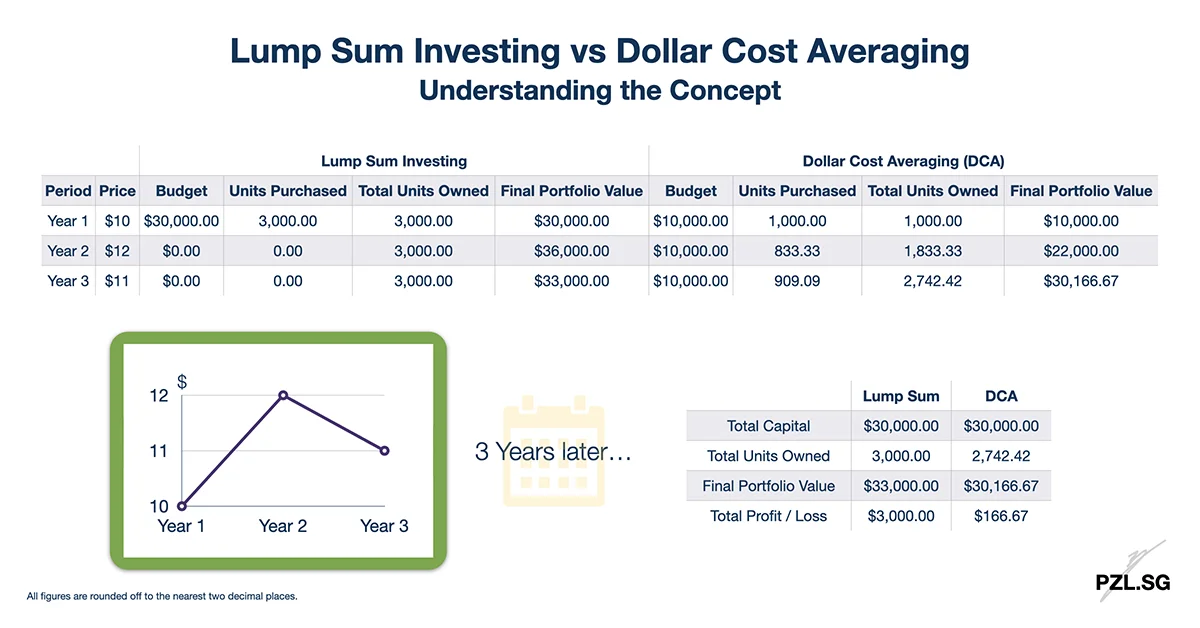

Part 2: Understanding the Concept

Part 2.1: Basic Assumptions

As a start, let’s do a general comparison between lump sum investing and dollar cost averaging. To illustrate, we will use the following three assumptions:

- Number of Periods: 3 Years

- Total Capital: $30,000 (to be split equally over the investment period for dollar cost averaging)

- All figures are rounded off to the nearest 2 decimal places.

Seeing that market price at $10 per investment unit for the first year,

- Lump Sum Investing: You will invest the entire capital of $30,000 into a portfolio. In effect, you will own $30,000 / $10 = 3,000 investment units today.

- Dollar Cost Averaging: Given that total capital of $30,000 to invest over 3 years, you will invest $30,000 / 3 years = $10,000 each year. For this purpose, you will buy $10,000 / $10 = 1,000 investment units today.

Part 2.2: When the Price moves Upwards, Price per Investment Unit = $12

- Lump Sum Investing: Since you have utilised your entire capital, you will not engage in any further investment activity.

- Dollar Cost Averaging: In this case, you will continue to use your annual budget of $10,000 to invest into the portfolio. Accordingly, you will purchase an additional $10,000 / $12 = 833.33 investment units.

Part 2.3: When the Price moves Downwards, Price per Investment Unit = $11

- Lump Sum Investing: Similar to Part 2.2, you will remain status quo.

- Dollar Cost Averaging: In similar fashion, you will buy $10,000 / $11 = 909.09 investment units.

In summary for lump sum investing, you will simply use your entire capital to buy as many investment units as you can in the first year. By comparison for dollar cost averaging, you will split the capital equally over the entire investment period first. Thereafter, you will invest the same amount during each period. Now that you have a grasp on each strategy, let’s go through four examples together.

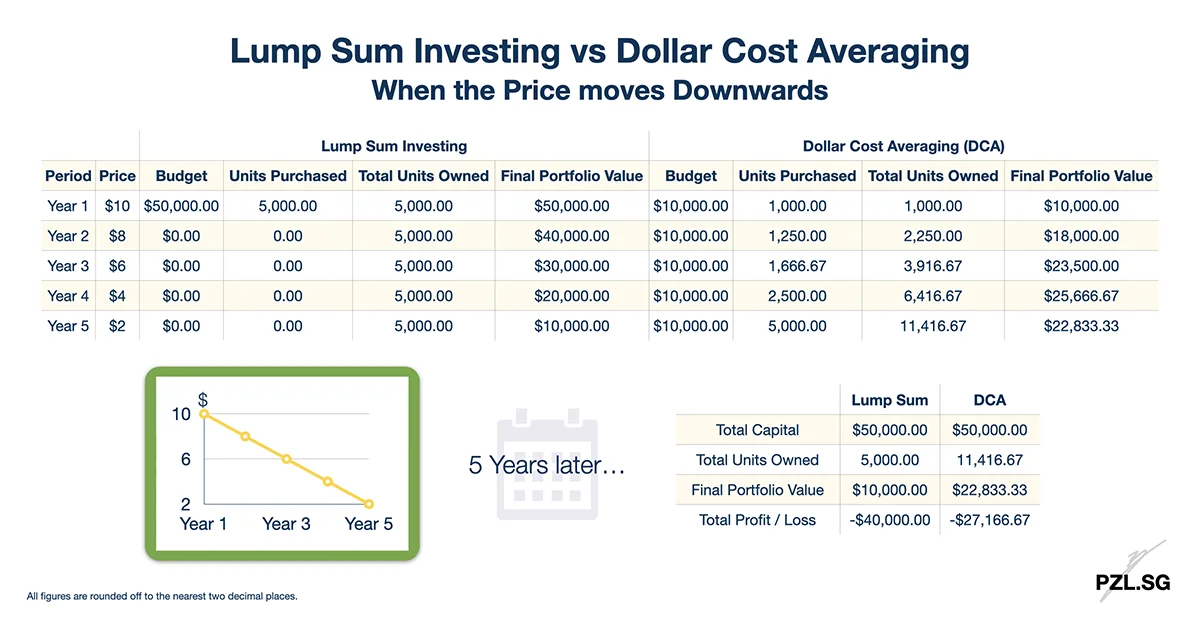

Part 3: When the Price moves Downwards

To illustrate, let’s take a total capital of $50,000 to invest over 5 years. Based on the current market price of $10 per investment unit,

- Lump Sum Investing: You will purchase $50,000 / $10 = 5,000 investment units.

- Dollar Cost Averaging: On this occasion, you will purchase $50,000 / 5 years / $10 = 1,000 investment units.

Part 3.1: At Year 2, Price per Investment Unit = $8

- Lump Sum Investing: You will remain status quo.

- Dollar Cost Averaging: You will use the annual budget of $10,000 to purchase $10,000 / $8 = 2,250 investment units.

In essence for lump sum investing, you will not buy or sell any investment units after the first year. In contrast for dollar cost averaging, you will continue to spend the annual budget to buy as many investment units as you can every year.

Part 3.2: Five years later…

In sum, you would have used a total capital of $50,000 for each strategy. Meanwhile,

- Lump Sum Investing: You will own 5,000 investment units, worth 5,000 x $2 = $10,000

- Dollar Cost Averaging: You will own 11,416.67 investment units, worth 11,416.67 x $2 = $22,833.33

To put it another way, you lost $50,000 – $10,000 = $40,000 via lump sum investing. Whereas for dollar cost averaging, you lost lesser amount of money; $50,000 – $22,833.33 = $27,166.67.

Part 3.3: Long-Term Outlook

In the long run, both strategies do not work well (obviously). Notwithstanding that, here is the key point to note:

- Lump Sum Investing: The number of investment units (that you own) is fixed after the first year. Consequently, you are not affected by the market volatility throughout the investment period. In time to come, your profit or loss will depend on the final position of your portfolio. If the portfolio’s final position is lower than its initial position, then you will suffer from a loss.

- Dollar Cost Averaging: In this situation, you are able to acquire more investment units during a downtrend market. In effect, this reduces the overall cost of the portfolio, thereby accounting for the lesser loss incurred.

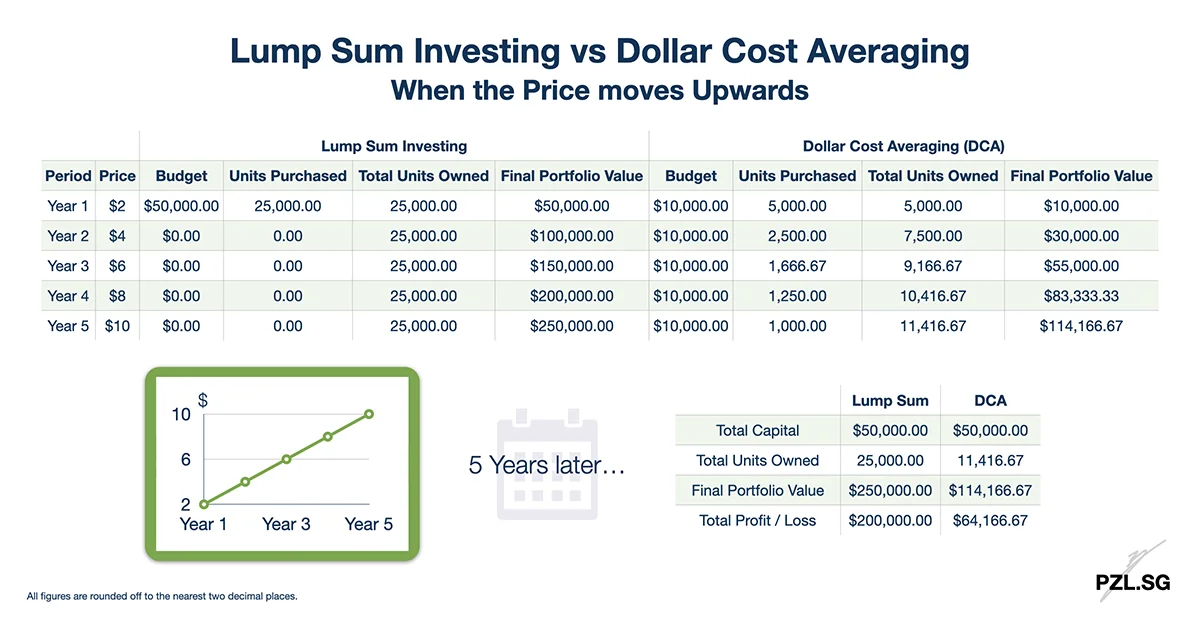

Part 4: When the Price moves Upwards

Comparatively, let’s look at an example when the portfolio portrays an upward trend. In the same way, let’s take a total capital of $50,000 to invest over 5 years. Based on the current market price of $2 per investment unit,

- Lump Sum Investing: You will purchase $50,000 / $2 = 25,000 investment units.

- Dollar Cost Averaging: In this case, you will purchase $50,000 / 5 years / $2 = 5,000 investment units.

Part 4.1: At Year 2, Price per Investment Unit = $4

- Lump Sum Investing: You will remain status quo.

- Dollar Cost Averaging: You will use the annual budget of $10,000 to purchase $10,000 / $4 = 2,500 investment units.

Similar to Part 3.1, you will just hold onto your investment units for lump sum investing. In contrast for dollar cost averaging, you will continue to spend the annual budget to buy as many investment units as you can every year.

Part 4.2: Five Years later…

To sum up,

- Lump Sum Investing: You will own 25,000 investment units, worth 25,000 x $10 = $250,000

- Dollar Cost Averaging: You will own 11,416.67 investment units, worth 11,416.67 x $10 = $114,166.67

In summary, you will make a profit of $250,000 – $50,000 = $200,000 from lump sum investing. By comparison, dollar cost averaging generated lesser profit, i.e. $114,166.67 – $50,000 = $64,166.67.

Part 4.3: Long-Term Outlook

In the long run, it should also be obvious that both strategies will generate a profit for you. Despite that, here is the key difference:

- Lump Sum Investing: Similar to Part 3.3, your profit or loss depends on the portfolio’s final position. It is without a doubt that you will earn a profit so long as the portfolio’s final position is higher than its initial position.

- Dollar Cost Averaging: Unlike Part 3.3, buying more investment units during an uptrend market increases the average cost of each investment unit. In effect, this thins your overall profit margin.

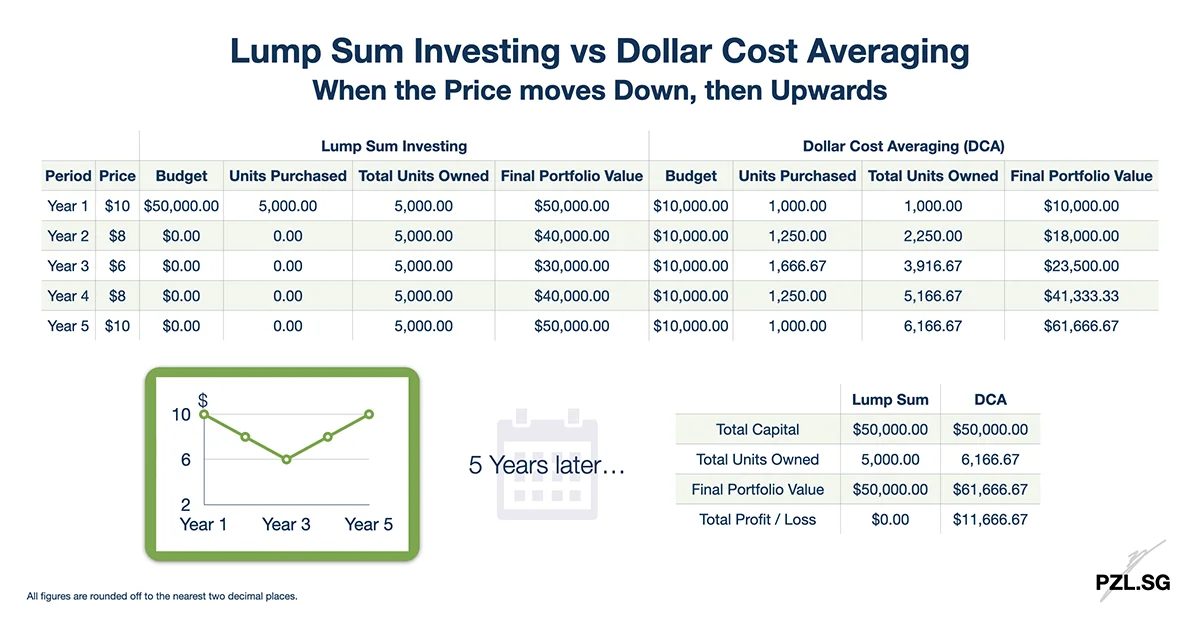

Part 5: When the Price moves Down, then Upwards

After two simple rounds of investing, let’s combine the scenarios from Part 3 and Part 4 together. Correspondingly, we will use the same capital of $50,000 in total. In detail, for

- Lump Sum Investing: You will use the entire budget to buy as many investment units as you can in the first year.

- Dollar Cost Averaging: You will use $50,000 / 5 years = $10,000 to buy as many investment units as you can every year (over 5 years).

Part 5.1: Five Years later…

In time to come,

- Lump Sum Investing: You will own 5,000 investment units, worth 5,000 x $10 = $50,000

- Dollar Cost Averaging: You will own 6,166.67 investment units, worth 6,166.67 x $10 = $61,666.67

As you can see, there is no profit or loss from lump sum investing. By comparison, dollar cost averaging gives you a profit of $61,666.67 – $50,000 = $11,666.67.

Part 5.2: Long-Term Outlook

- Lump Sum Investing: If the starting point and the ending point are the same, then you will neither make a profit nor suffer from a loss. While this may be true, what are the chances for this phenomenon to happen in reality?

- Dollar Cost Averaging: Owing to the initial downtrend, you managed to buy more investment units. After the portfolio’s recovery, these investment units are worth a higher value. Despite staying at the same unit price (as year 1), dollar cost averaging helps you to reap 23% profit!

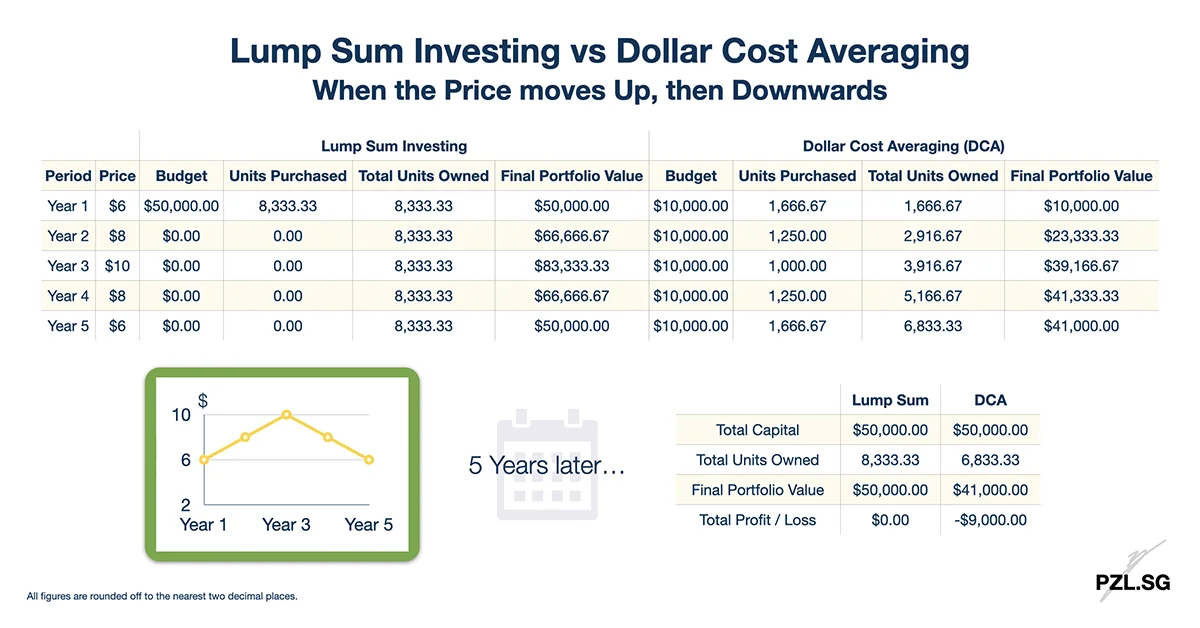

Part 6: When the Price moves Up, then Downwards

Comparatively, let’s invert the scenario in Part 5. In like fashion, we will keep to the total investment capital of $50,000. For this purpose,

- Lump Sum Investing: You will use the entire budget to buy as many investment units as you can in the first year.

- Dollar Cost Averaging: You will use $50,000 / 5 years = $10,000 to buy as many investment units as you can each year (for 5 years).

Part 6.1: Five Years later…

In due time,

- Lump Sum Investing: You will own 8,333.33 investment units, worth 8,333.33 x $6 = $50,000

- Dollar Cost Averaging: You will own 6,833.33 investment units, worth 6,833.33 x $6 = $41,000

For the same reason given in Part 5, there is no profit or loss from lump sum investing. However, you lost $50,000 – $41,000 = $9,000 from dollar cost averaging.

Part 6.2: Long-Term Outlook

- Lump Sum Investing: Given that same position, you will neither make a profit nor suffer from a loss.

- Dollar Cost Averaging: Unlike the situation in Part 5, you lost 18% of your capital. For one thing, this proves that dollar cost averaging works only if the portfolio recovers eventually. Otherwise, you will never reach the breakeven point.

Part 7: Lump Sum Investing vs Dollar Cost Averaging

In the final analysis, both investment strategies have its pros and cons. Since neither strategy is foolproof, we can use three key questions to help us in the decision-making process:

- Do you have the lump sum available today? (Liquidity Risk)

- Are you comfortable with investing all your capital at one go? (Risk Appetite)

- Are you certain of the portfolio’s direction over your investment period? (Timing Risk)

Above all, every investment comes with some form of investment risks. With this in mind, you should invest based on your risk appetite after a thorough research. After all, investing is about optimising your returns based on your risk profile, and not just maximising returns alone.

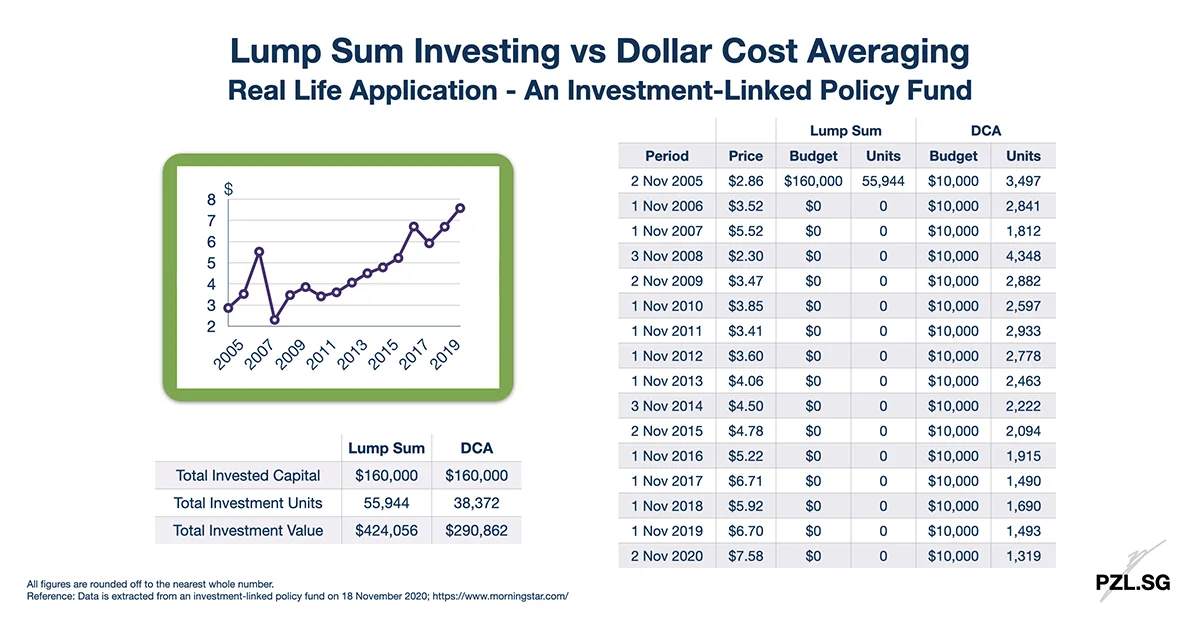

Part 8: Real Life Application

As usual, let’s end this post with a real life application between lump sum investing and dollar cost averaging. For this purpose, I took the data from an investment-linked policy fund.

Leave a Reply