By and large, a revocable nomination is a common method to distribute your insurance policy’s death benefit to your intended beneficiary. In order to do this, you will need to complete the insurer’s prescribed form. Before we do that, let’s understand eight things to know about a revocable nomination for an insurance policy in Singapore.

Table of Contents:

- Who can make a Revocable Nomination?

- What types of policy are relevant?

- Will You lose your rights to the policy?

- How will the Policy benefits be distributed?

- What if the nominee dies before me?

- How do You submit a Revocable Nomination?

- Can You make changes to the nomination?

- Should You make a nomination?

One Minute Summary:

- In order to make a revocable nomination, you need to be both the policy owner as well as the life insured under the policy.

- After you have made a revocable nomination, you will continue to retain full rights and ownership over the policy.

- It is important to realise that you will continue to receive all the living benefits under the policy.

- On the other hand, your nominee(s) will receive the death benefit from the insurance policy.

- For one thing, you may revoke your insurance nomination anytime.

Part 1: Who can make a Revocable Nomination?

Firstly, you need to be the policy owner as well as the life insured under the policy. Furthermore, you must be at least 18 years old.

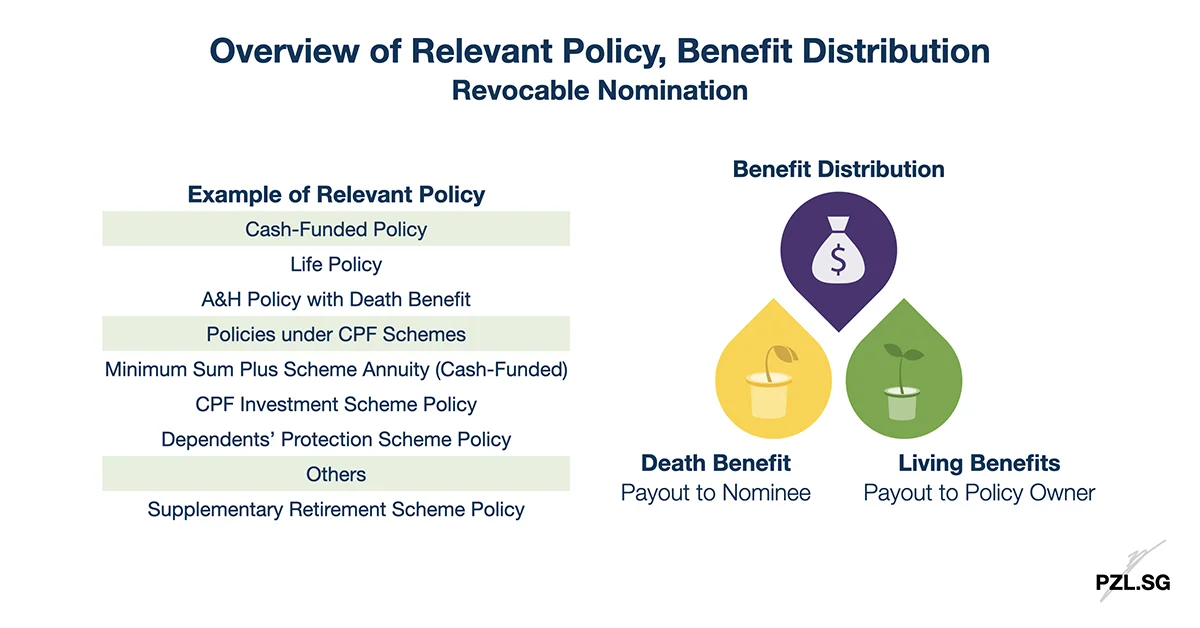

Part 2: What types of policy are relevant?

Secondly, the insurance policy must

- Be a life policy, or an accident and health policy; and

- Insure the life of the policy owner; and

- Provide death benefits; and

- Not be the subject of any trust created under Section 73 of the Conveyancing and Law of Property Act (Cap. 61); and

- Not be an annuity purchased with the retirement sum under Section 15(6C) of the Central Provident Fund Act.

Part 3: Will You lose your rights to the policy?

As the policyholder, you will continue to retain full rights and ownership over the policy. Accordingly, you can revoke the nomination at any time without the consent of the nominee(s). (See Part 7 on how to revoke a revocable nomination.)

Part 4: How will the Policy benefits be distributed?

Part 4.1: Death Benefit

Generally, the nominee will receive only the death benefit from the insurance policy. In the event that the nominee is below 18 years old, the legal guardian will receive the payout.

Part 4.2: Living Benefit

As the policy owner, you will continue to receive all the living benefits. For example, the policy may include coverage for Total & Permanent Disability, and/or Critical Illness. Under those circumstances, you will receive the payout accordingly.

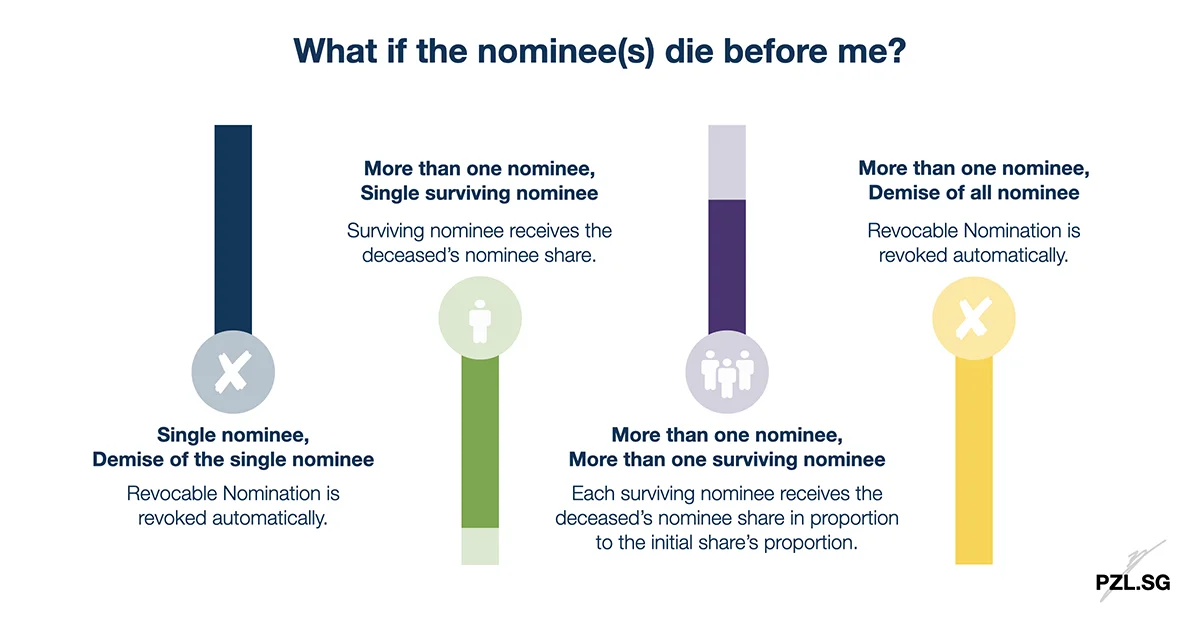

Part 5: What if the nominee dies before me?

Case 5.1: Single nominee, Demise of the single nominee

Given that there is no surviving nominee, the revocable nomination will be revoked automatically.

Case 5.2: More than one nominee, Single surviving nominee

In this case, we will consolidate the deceased nominees’ share first. Thereafter, we will add to the surviving nominee’s share of the death benefit.

Case 5.3: More than one nominee, More than one surviving nominees

In like manner, we will consolidate the deceased nominees’ share first. Thereafter, we will add to each surviving nominee’s share in proportion to each surviving nominee’s initial share.

Case 5.4: More than one nominee; No surviving nominee

In the same way as Case 5.1, there are no surviving nominees. Consequently, the revocable nomination will be revoked automatically.

Part 6: How do You submit a Revocable Nomination?

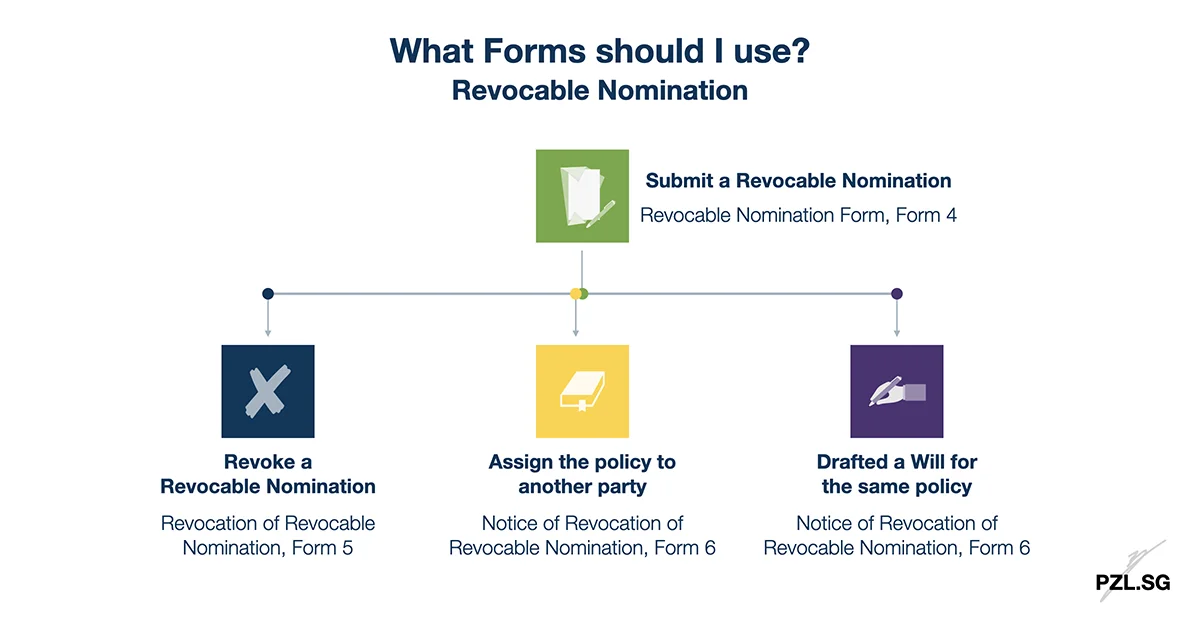

We will use the insurer’s prescribed Form 4, Revocable Nomination Form for this purpose. It is important to realise that you will need to submit one form for each relevant policy. To put it another way, if you have three insurance policies, then you will need to complete three separate forms.

Trivia: Personally, I prefer not to have the witnesses’ section on the same page as the nominees’ section.

Part 7: Can You make changes to the nomination?

In a word, yes. This is because you retain full rights and ownership over the policy. Therefore, you may revoke your existing nomination and make another nomination at any time.

Part 7.1: Revoke a Revocable Nomination

In truth, there will be situations when you wish to make changes to your existing insurance nomination. To illustrate, you may wish to add the newborn to your existing list of nominees. On the other hand, you may want to cancel the nomination only. In either case, you may use the prescribed Form 5, Revocation of Revocable Nomination.

Part 7.2: You assign the policy to another party

When you assign the interest of the policy to another party, the revocable nomination will be deemed revoked. In this case, you will need to notify the insurance company on the revocation. For this purpose, you will need to use the prescribed Form 6, Notice of Revocation of Revocable Nomination.

Part 7.3: You make a Will in accordance with the Wills Act (Cap. 352)

Now, let’s assume that you have completed a revocable nomination for your insurance policy. However, you wish to include the same payout in your Will. In order to prevent unnecessary confusion, let’s notify the insurance company on the revocation. In like manner, you will use the prescribed Form 6, Notice of Revocation of Revocable Nomination. (Same form as Part 7.2)

Part 8: Should You make a nomination?

Short answer: Yes

Above all, an insurance nomination continues to form part of the professional practice in my work. In detail, this happens during the time when I prepare an insurance policy file for my client. It is then when I will (nag) encourage my client to “do some homework”.

By and large, you will not want to leave it to the government to decide the distribution for you.

Checklist:

- Consolidate all your insurance policies into a proper insurance policy summary.

- Get a file to store all your insurance policy related documents.

- Complete an insurance nomination for each relevant policy.

This post is part of Starter’s Guide! This means that I have taken extra time and effort to explain the basics of the presented topic in a simple manner. In effect, I hope this helps you to start responsible planning today. Subscribe to my newsletter if you like to see more of these content!

Reference:

Insurance Act (Chapter 142)

Leave a Reply