Singlife Dementia Cover is a long-term care insurance policy that provides you with a payout in the event of a mental disability. According to Singlife, this is a first-in-market long-term care protection plan that provides up to $170,000 in payouts for cognitive decline and mental health conditions. Moreover, Singlife Dementia Cover includes a lump-sum payout for dementia-related depressive or anxiety disorder and accidental burns or fractures. With this in mind, let’s learn about Singlife Dementia Cover (“the Plan”) in this post.

Table of Contents:

- What is Singlife Dementia Cover

- Insurance Coverage (Benefits)

- Cash Value

- Insurance Premium (Cost)

- Limitations and Risk

- Insurance Nomination

- Singlife Care Collab

- Eligibility

- Target Audience

- Definition

One Minute Summary:

- Type of Plan: Non-Participating

- Type of Coverage: Long-term care

- Main Benefits: Mental Disability Benefit

- Coverage Amount: Between $200 to $2,000

- Coverage Period: Till 99 Age Next Birthday

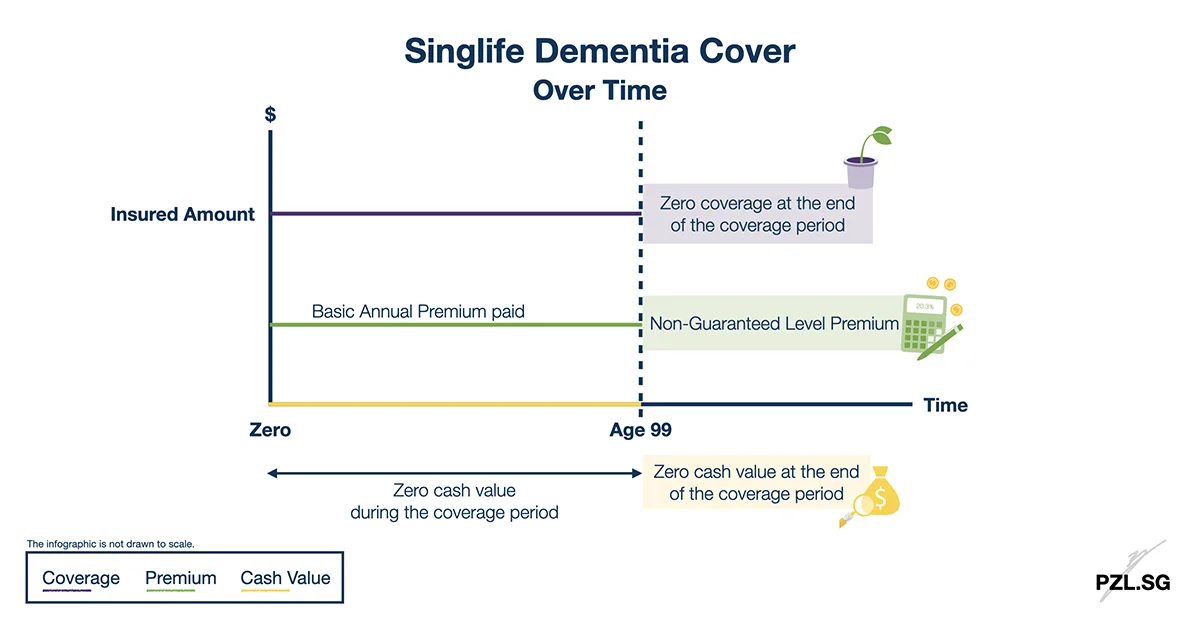

- Cash Value: Nil

- Premium Payment Period: Till 99 Age Next Birthday

Part 1: What is Singlife Dementia Cover

Singlife Dementia Cover is a non-participating health insurance policy. This means you will not participate or share in the profits of the insurer’s participating fund. Instead, the insurance premium is used to pay for the insurance charges and the product’s distribution cost.

Part 2: Insurance Coverage (Benefits)

Part 2.1: Main Benefits

Singlife Dementia Cover provides four main benefits and I have summarised them in the following table:

Table: Summary of Benefits for Singlife Dementia Cover

| Cognitive Care Benefit | Mental Care Benefit | Emotional Resilience Benefit | Mental Expenses Benefit | |

|---|---|---|---|---|

| Condition for Claim | Upon Late Dementia | Upon Major Depressive Disorder; or Schizophrenia; or Bipolar Disorder; or Early / Intermediate Dementia | After being diagnosed with Early / Intermediate / Late Dementia, the Insured has either Depression; or Anxiety | After being diagnosed with Early / Intermediate / Late Dementia, the Insured sustains an Accidental Injury |

| Payout Structure | Yearly payout, up to a max of 10 years | Yearly payout, up to a max of 5 years | Lump Sum payout (once per lifetime) | Lump Sum payout (once per lifetime) |

| Payout Amount | 5 times the selected benefit amount per year | 5 times the selected benefit amount per year | 5 times the selected benefit amount in one lump sum | 5 times the selected benefit amount in one lump sum |

| Coverage Period | Up to Age 99 | Up to Age 80 | Up to Age 80 | Up to Age 80 |

| Other Notes | Upon payout for Cognitive Care Benefit, Mental Care Benefit will cease and not be claimable | Benefit can be paid concurrently with other Benefits, except Cognitive Care Benefit | Benefit will be paid only once; benefit can be paid concurrently with other benefits | Benefit will be paid only once; benefit can be paid concurrently with other benefits |

For the Cognitive Care Benefit, as soon as the Plan starts paying this benefit, the Mental Care Benefit ends and will no longer be claimable.

For Cognitive Care Benefit, and Mental Care Benefit, the payout is made over ten years and five years respectively. Let’s take the case when you recover from the covered condition after two years. If you meet the condition for a claim again in the future, the Plan will pay the remainder of the benefit payout duration, i.e. for up to eight years and three years respectively (depending on which condition you are diagnosed with).

After the date of diagnosis of Late Dementia, the Insurer will also waive the payment of the insurance premium. This means you do not need to pay the insurance premium during the period when you have Late Dementia.

Part 2.2: Coverage Amount

You have the option to select a benefit amount that ranges from $200 to $2,000, making a $100 adjustment each time. For instance, you may choose a benefit amount of $500. In this case, the payout amount would be $500 x 5 times = $2,500 (either as a lump sum or an annual payout, depending on the condition of the claim).

It is important to realise that Singlife does not allow you to increase the benefit amount after the policy’s commencement date. Despite that, Singlife allows you to reduce the benefit amount while the Plan is in force. To do so, you should not have made any claims on the Plan yet.

Part 2.3: Coverage Period

Singlife Dementia Cover will insure you till you reach 99 (based on Age Next Birthday). During this period, Singlife guarantees that you will be able to renew this long-term care insurance policy annually. This is so long as you pay the insurance premium on time.

That being said, Singlife Dementia Cover will terminate upon certain events, e.g. death of the life insured. Given that the list of events is relatively long, I will encourage you to read the Product Summary or the Insurance Policy Contract for the full list.

Part 3: Cash Value

As a non-participating health insurance policy, Singlife Dementia Cover does not have any cash value. Accordingly, you won’t be able to terminate this Plan for a surrender value. Instead, you will receive a payout from the insurance policy only when a covered event is triggered.

Part 4: Insurance Premium (Cost)

Part 4.1: Premium Determinants

Generally, the insurance premium is determined based on your entry age and gender. Additionally, it also depends on the coverage amount that you have chosen.

Part 4.2: Non-Guaranteed Level Premium Rates

Although the insurance premium rate is level, it is not guaranteed to remain the same throughout the entire policy period. In general, a level insurance premium means you will pay the same amount of money to the insurer every year. Despite that, Singlife reserves the right to revise the insurance premium rate for each age during the policy anniversary (by serving you a notice of revision at least 30 days in advance). Thereafter, the insurance premium rate will be adjusted. Hence, in this case, we say that the insurance premium rate is not guaranteed.

Part 4.3: Premium Period

The premium paying period coincides with the coverage period. Accordingly, you will pay up to the policy anniversary after you turn 98 years old (based on Age Next Birthday).

Part 4.4: Distribution Cost

In general, distribution cost refers to the charges that arise from the marketing and sale of a product or service. To sum up, the total distribution cost for Singlife Dementia Cover spreads across the first six policy years. In detail, the distribution cost for the respective six years is 109%, 45%, 20%, 15%, 10%, and 10%.

Part 5: Limitations and Risk

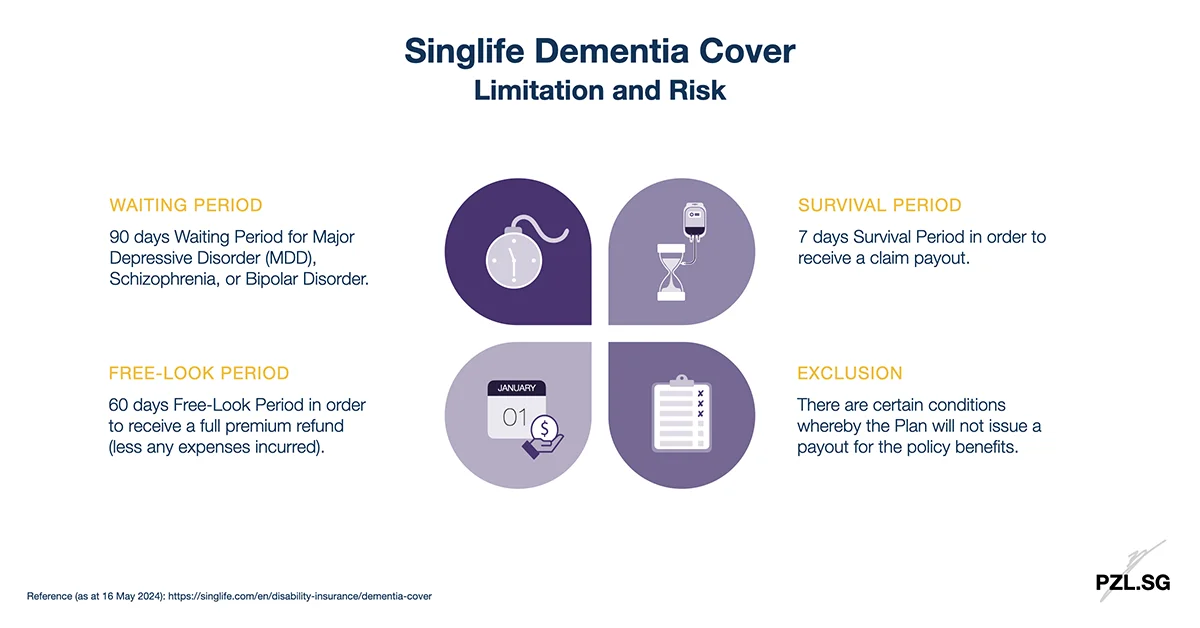

Part 5.1: Waiting Period

There is a 90-day Waiting Period for Major Depressive Disorder (MDD), Schizophrenia, or Bipolar Disorder. During this period, the Plan will not make any benefit payout for the above-mentioned conditions. The insurer counts the 90 days based on the date of diagnosis from the

- Policy Issue Date;

- Benefit Commencement Date of the Basic Benefit; or

- Reinstatement date of the Plan;

whichever latest.

Part 5.2: Survival Period

For the benefit to be payable, you must survive for 7 days after the date of diagnosis for the covered condition. To point out, there is no death benefit for this insurance policy. As a result, if you pass away before the end of the survival period, then there is no payout from this Plan.

Part 5.3: Free-Look Period

Singlife Dementia Cover comes with a 60-day Free-Look Period. The Free-Look Period begins 7 days after Singlife sends the insurance policy contract out to you (be it by post or electronically). Accordingly, if you write to Singlife to cancel your insurance policy during this period, Singlife will refund the insurance premium that you have paid, without interest. Additionally, Singlife will also deduct any expenses that they have incurred in assessing the risk under the policy and in issuing the insurance policy.

Part 5.4: Exclusion

There are certain conditions whereby the Plan will not issue a payout for the policy benefits. Given that the list of exclusions is relatively long, I will encourage you to read the Product Summary or the Insurance Policy Contract for the full list of exclusions.

Part 6: Insurance Nomination

Based on the current Insurance Nomination Law, you are allowed to make a revocable nomination. On the other hand, you are not allowed to make a trust nomination.

Part 7: Singlife Care Collab

Singlife Care Collab is a one-stop health services hub that offers you convenient access to health care services. For example, Singlife partners with Dementia Singapore, a leading Social Service Agency that specialises in dementia care and is an ardent advocate for a dementia-inclusive society. Additionally, as a Singlife policyholder, you will also enjoy exclusive discounts on selected services, e.g. up to 15% discount on Elderly Care hourly rates from Helpling Care, a home caregiver service provider.

Part 8: Eligibility

To apply for Singlife Dementia Cover, you need to fulfil the following three criteria:

- Either a Singapore Citizen or a Singapore Permanent Resident; and

- Age between 31 and 65 (based on Age Next Birthday); and

- Have an in-forced Singlife’s Long-Term Care Product.

Part 9: Target Audience

According to Alzheimer’s Disease International (ADI), someone in the world develops dementia every three seconds. In fact, in 2020, it was estimated that there are over 50 million people worldwide living with dementia and this number will almost double every 20 years. Under those circumstances, you may require long-term care support. With this intention in mind, Singlife Dementia Cover strives to provide you with some financial relief during this period.

That being said, not everyone is eligible to purchase Singlife Dementia Cover (refer to the Eligibility criteria in Part 8). In fact, Singlife offers this Plan to a small group of existing clients only. Generally, this group of clients would need to have an in-force Long-Term Care insurance policy with Singlife. At this time, Singlife’s Long-Term Care products (e.g. Singlife CareShield Standard) focus on payout if you need assistance with Activities of Daily Living.

By comparison, in addition to the Activities of Daily Living, Singlife Dementia Cover includes coverage for mental disability. Accordingly, this is a plan that you can consider if you wish to have some insurance coverage in the event of cognitive decline.

Want to hear my thoughts on this plan? Subscribe to my free newsletter to gain exclusive insights today!

Part 10: Definition

Singlife Dementia Cover admits a claim for several conditions. However, I’m not going to define every single condition in this post. Instead, I will focus on the main condition, Dementia.

Part 10.1: Early / Intermediate Dementia

Refers to the unequivocal diagnosis of dementia, characterised by irreversible deterioration or loss of cognitive function that has persisted for at least 6 months, as confirmed and supported by all of the following:

- Neuroimaging studies such as CT, MRI, or PET scans; and

- Evidence of moderate functional deficits, where the severity is determined by the results of psychometric assessment as below:

- Clinical Dementia Rating (CDR) score equal to 2; or

- Global Deterioration Scale (GDS) stage 5; or

- Functional Assessment Staging Tool (FAST) stage 5

The confirmatory diagnosis and functional deficits as mentioned above must be certified by a geriatrician, psychiatrist (including geriatric psychiatrist) or neurologist.

The following are excluded:

- Non-organic illnesses, including but not limited to pseudodementia or other psychiatric disorders, and

- Alcohol or drug-related brain damage

Part 10.2: Late Dementia

Refers to the unequivocal diagnosis of dementia, characterized by irreversible deterioration or loss of cognitive function that has persisted for at least 6 months, as confirmed and supported by all of the following:

- Neuroimaging studies such as CT, MRI, or PET scans; and

- Evidence of severe functional deficits, where the severity is determined by the results of psychometric assessment as below:

- Clinical Dementia Rating (CDR) with a score equal to 3; or

- Global Deterioration Scale (GDS) stage 6 or 7; or

- Functional Assessment Staging Tool (FAST) stage 6 or 7.

The confirmatory diagnosis and functional deficits as mentioned above must be certified by a geriatrician, psychiatrist (including geriatric psychiatrist) or neurologist.

The following are excluded:

- Non-organic illnesses, including but not limited to pseudodementia or other psychiatric disorders, and

- Alcohol or drug-related brain damage

Disclaimer:

This post contains a summary of Singlife Dementia Cover and it is for informational purposes only. Accordingly, you are advised to read the respective product summary for full disclaimer and/or seek professional advice. The views and opinions expressed in this publication are those of the author. Therefore, they do not reflect the official policy or position of any other agency, organisation, employer or company. Assumptions made in the analysis are not reflective of the position of any other agency, organisation, employer or company other than the author. This advertisement has not been reviewed by the Monetary Authority of Singapore. Information is correct as of 14 May 2024. Protected up to specified limits by SDIC.

Leave a Reply