An Integrated Shield Plan (IP) is a private health insurance policy sold by insurance companies in Singapore. It works together with MediShield Life to provide additional coverage for large hospital bills and selected costly outpatient treatments.

While Integrated Shield Plans are primarily structured for Singapore Citizens and Permanent Residents, expatriates working in Singapore may also use them to complement corporate insurance schemes.

Given the relatively wide target audience, this article explains the key features, limitations, and trade-offs of Integrated Shield Plans. This will help you assess whether they enhance your existing health insurance coverage.

🎥 Prefer watching? Check out the video version of this post.

Table of Contents:

- What is an Integrated Shield Plan

- Insurance Coverage (Benefits)

- Cash Value

- Insurance Premium (Cost)

- Limitations and Risks

- Claims

- Insurance Nomination

- Eligibility

- Target Audience

- Integrated Shield Plan vs MediShield Life

- Final Thoughts

- Changelog

One Minute Summary:

- An Integrated Shield Plan (IP) provides additional coverage on top of the mandatory MediShield Life, offering coverage for higher ward classes or private hospitals.

- IPs generally cover eligible hospital bills on an ‘as-charged’ basis and include pre- and post-hospitalisation benefits.

- Premiums are higher and increase with age. They are funded by a mix of MediSave (up to Additional Withdrawal Limits) and cash.

- Even with an IP, you are responsible for the deductible and co-insurance component of the medical bill.

- An Integrated Shield Plan may suit individuals who prioritise flexibility in choosing their own doctor, speed of access to care, and can afford the higher premium rates.

Part 1: What is an Integrated Shield Plan

An Integrated Shield Plan (IP) is a private health insurance policy sold by insurance companies in Singapore. It is designed to integrate with MediShield Life, Singapore’s basic health insurance scheme that covers all Singapore Citizens and Permanent Residents.

MediShield Life provides a baseline level of protection. It primarily covers treatment in public hospitals (Class B2/C wards), subject to deductibles, co-insurance, and claim limits.

An Integrated Shield Plan builds on this baseline by offering higher coverage limits and access to higher ward classes or private hospitals, depending on the plan tier.

Part 1.1: How an Integrated Shield Plan Works

Singapore’s healthcare insurance structure is designed in layers.

Layer 1: MediShield Life

- Automatic and mandatory for all Singapore Citizens and Permanent Residents

- Covers basic hospitalisation expenses, subject to claim limits

- Applies mainly to Class B2/C wards in public hospitals

- Annual claim limit of up to $200,000 per policy year

- Funded through MediSave deductions and government support

- Involves sub-limits, pro-ration, deductibles, co-insurance

MediShield Life is designed for basic adequacy rather than comfort or choice.

Layer 2: The Additional Private Insurance Component (IP)

- Offered by private insurers and regulated by the Ministry of Health (MOH)

- Provides additional private insurance coverage beyond MediShield Life limits

- Offers coverage for private hospitals or higher ward classes (Class A/B1)

- Typically offers higher annual claim limits, depending on plan tier

- Requires additional premiums payable via MediSave and/or cash

While benefit structures differ across insurers, all Integrated Shield Plans must meet Ministry of Health (MOH) requirements.

Layer 3: Optional Rider

An Integrated Shield Plan Rider (IP Rider) is an optional add-on. Its primary purpose is to reduce the deductible and co-insurance payable under the IP, subject to mandatory co-payment requirements.

Co-payment exists to encourage cost awareness and to reduce over-consumption of healthcare services.

Part 1.2: How the Integration Works in Practice

In practice, the “integration” in an Integrated Shield Plan simplifies the claims experience. When you are hospitalised, the hospital helps you submit a single claim request.

Your private insurer acts as your primary point of contact. They process the bill in two stages:

- Applying the MediShield Life component payouts

- Add the extra coverage from your IP

They issue a combined payment directly to the hospital, sparing you the administrative burden of managing two separate policies.

Part 1.3: Insurers

The following insurers currently offer Integrated Shield Plans in Singapore:

- AIA Singapore Private Limited: HealthShield Gold Max

- Great Eastern Life Assurance Co: GREAT SupremeHealth

- HSBC Life (Singapore) Private Limited: HSBC Life Shield

- Income Insurance Limited: Enhanced IncomeShield

- Prudential Assurance Company Singapore: PRUShield

- Raffles Health Insurance: Raffles Shield

- Singapore Life Limited: Singlife Shield

Part 2: Insurance Coverage (Benefits)

An Integrated Shield Plan provides greater flexibility in healthcare coverage. By selecting a plan tier that aligns with your healthcare preferences, you gain the right level of financial support to meet the medical expenditure.

Part 2.1: Types of Plans Available

Insurers generally offer four tiers of coverage:

- Private Hospital Plans (Standard rooms)

- Class A Plans (Public Hospitals)

- Class B1 Plans (Public Hospitals)

- Standard Integrated Shield Plan (Public Hospitals, Class B1 ward)

Higher tiers offer higher claim limits and greater flexibility, but this comes with higher premiums.

Part 2.2: General Benefits

Integrated Shield Plans are designed to cover eligible large, unexpected expenses. Coverage typically includes:

Hospitalisation Expenses:

- Daily ward and treatment charges

- Surgical procedures

- Implants

- Radiosurgery

- Continuation of Autologous Bone Marrow

- Transplant Treatment for Multiple Myeloma

Outpatient Treatment:

- Cancer Drug Treatment

- Cancer Drug Services

- Radiotherapy for Cancer

- Kidney Dialysis

- Immunosuppressants for Organ Transplants

- Erythropoietin for Chronic Kidney Failure

- Long-Term Parenteral Nutrition

Additional Benefit Limits:

- Pre-Hospitalisation Treatment

- Post-Hospitalisation Treatment

- Major Organ Transplant

- Living Donor Organ Transplant

- Pregnancy and Delivery-Related Complications

- Congenital Abnormalities Benefit of Insured

- Emergency overseas treatment

- Proton Beam Therapy Treatment

- Cell, Tissue and Gene Therapy

Coverage details vary across insurers, but core benefits are broadly similar. The Ministry of Health Singapore provides a comparison table to help you evaluate different plans.

Part 2.3: Coverage Amount

Generally, Integrated Shield Plans offer higher annual claim limits than MediShield Life. This reduces the risk of unexpected large medical bills.

Coverage operates on a policy-year basis. A policy year is the 12-month period starting from the date your policy begins or renews. For example, if your coverage began on 1 May, your policy year runs from 1 May this year to 30 April the following year. This is important as the treatment benefit limits reset every policy year, ensuring ongoing coverage for long-term illnesses such as cancer.

Part 2.4: Coverage Period

Similar to MediShield Life, Integrated Shield Plans are structured to provide lifelong insurance coverage, provided premiums are paid when due and the policy remains in force. This continuity is particularly relevant as healthcare needs tend to increase with age.

Part 3: Cash Value

An Integrated Shield Plan is a non-participating plan. This means:

- The plan does not accumulate cash value

- There is no surrender value

- There is no investment component

In other words, premiums are paid solely in exchange for medical coverage.

Part 4: Insurance Premium (Cost)

Part 4.1: Premium Determinants

Integrated Shield Plan premiums are age-based and payable annually. Insurers determine premiums using Age Next Birthday (ANB) at each renewal. Premiums increase with age, reflecting higher healthcare utilisation and costs.

Part 4.2: Why Premiums Increase with Age

Integrated Shield Plans operate on a risk-pooling model, and the rates are non-guaranteed. Premiums collected from policyholders fund claims across the insured pool. As age increases, the probability and cost of claims rise. This results in higher premiums for older age bands to account for increased medical risks.

Part 4.3: Type of Payment

Premiums are payable by MediSave, subject to a cap known as the Additional Withdrawal Limit (AWL):

- $300 per year if aged 40 or below (next birthday)

- $600 per year if aged 41 to 70

- $900 per year if aged 71 and above

Any amount above these limits must be paid in cash. Foreigners must pay the full premium in cash. Rider premiums for IPs (Layer 3) must also be paid entirely in cash.

Part 4.4: Premium Paying Period

Integrated Shield Plans are yearly renewable policies. Premiums are payable annually for as long as coverage is maintained.

Part 4.5: Estimated Lifetime Cost

Premium levels depend on residency status and plan tier. Based on available insurer averages, the estimated lifetime premium cost (from age 0 to 100) is approximately:

- Class A ward (public hospital): $66,516

- Private hospital: $201,158

These figures reflect averages across the 7 insurers and apply to the IP only.

Part 5: Limitations and Risks

An Integrated Shield Plan is not an unlimited “blank cheque”. Here are some constraints to be aware of.

Part 5.1: Claim Limits

Each IP has an annual claim limit, with sub-limits for specific treatments. Expenses exceeding these limits must be paid using MediSave or cash.

Part 5.2: Pro-Ration Factor

If you seek treatment at a facility above the plan’s coverage level, a pro-ration factor applies.

For example, a plan that covers up to Class A wards may apply a 70% pro-ration factor for private hospital treatment. This means only 70% of the bill is considered for claim computation.

Part 5.3 Deductible

After pro-ration (if applicable), a deductible applies. A deductible is a fixed amount payable once per policy year. Deductibles may be paid using MediSave, subject to the applicable withdrawal limits.

Part 5.4 Co-Insurance

After the deductible, you must pay co-insurance – a percentage of the claimable amount. Co-insurance applies to every bill.

Co-insurance exists to promote cost awareness and reduce over-consumption of medical services.

Part 5.5: Pre-Existing Conditions

A pre-existing condition is any illness, injury, or symptom that existed before you purchased the plan or during the waiting period.

Coverage for pre-existing conditions is subject to medical underwriting. Depending on the outcome, such conditions may be excluded, loaded (higher premiums), or deferred (coverage delayed).

Part 5.6: Panel Restrictions and Pre-Authorisation

Some plans require the use of the insurer’s panel network for full benefits. Certain treatments also require pre-authorisation. Visiting a non-panel doctor or undergoing treatments without pre-authorisation may result in higher out-of-pocket costs or reduced coverage.

Part 6: Claims

Part 6.1: Claim Process

To make a claim, inform the medical institution. Claims are submitted electronically to the insurer, which acts on behalf of the Central Provident Fund (CPF) Board for the MediShield Life portion.

Once approved:

- The IP pays the hospital directly.

- You may use your MediSave account to pay your share, within the withdrawal limits.

- Any remaining balance is payable in cash.

Let’s examine how an IP claim computation works.

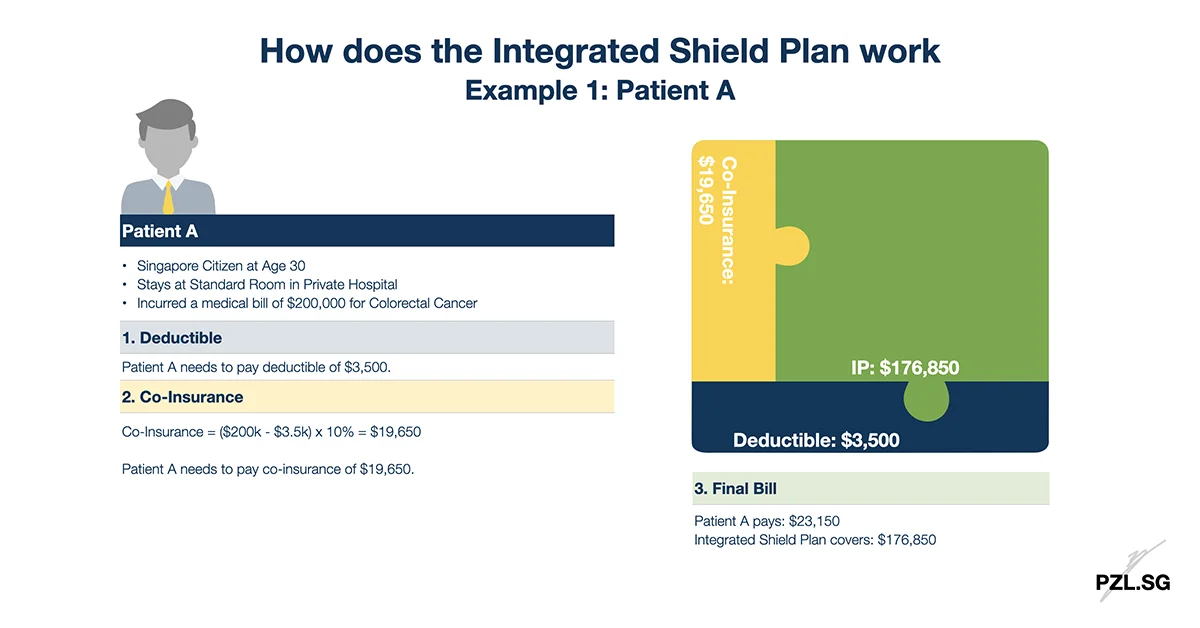

Part 6.2: Example 1 – Patient A

Patient A’s Profile:

- Singapore Citizen at Age 30

- Stays in a Standard Room in a Private Hospital

- Incurred a total bill of $200,000 for Colorectal Cancer

Here is the breakdown of Person A’s medical bill:

- Firstly, Patient A needs to pay a fixed cost of $3,500 for the deductible.

- Next, he needs to pay a co-insurance of $19,650. (Refer to Example 3 above for the calculation.)

- Finally, the Integrated Shield Plan will cover the remainder of the bill.

In total, Patient A pays $23,150 out-of-pocket, while the Integrated Shield Plan covers $176,850.

Part 7: Insurance Nomination

Integrated Shield Plans do not provide death benefits. As such, insurance nomination does not apply.

Part 8: Eligibility

All Singapore residents may apply for an Integrated Shield Plan, including Citizens, Permanent Residents, and foreigners with a valid pass. Some insurers restrict plan types for foreigners, though no such restrictions apply to locals.

When buying an integrated shield plan, you must declare any medical conditions. Underwriting outcomes generally fall into five categories:

- Standard acceptance: You will pay the standard premium rate for standard coverage.

- Loading: You will pay an additional premium to cover the pre-existing condition.

- Exclusion: You will pay the standard premium rate. However, the insurance policy will not cover the pre-existing condition.

- Postpone: The insurer is unable to offer any terms of acceptance at this time. However, you may apply again at a later time.

- Decline: The insurer is unable to offer any terms of acceptance.

Children are typically eligible from 15 days old, and the last entry age is generally 75. Policies may be renewed for life thereafter.

Part 9: Target Audience

Integrated Shield Plans are not essential for everyone.

An IP may suit individuals who:

- Value flexibility, speed, and choice: You want the option to choose your own specialist and avoid waiting times associated with subsidised care

- Prefer privacy: You require a single room or a 4-bedder (Class A/B1) rather than an open ward (Class B2/C)

- Can manage future costs: You are prepared for premiums to rise significantly in old age

Meanwhile, an IP may be less suitable if:

- Budget is tight: If paying premiums strains your monthly cash flow, relying on MediShield Life is a financially prudent choice

- Content with public healthcare: Singapore’s subsidised wards (Class B2/C) offer excellent medical outcomes. If you are comfortable with shared wards and assigned doctors, the incremental benefit of an IP may not justify the cost

- Have comprehensive corporate coverage: However, rely on this with caution. Coverage typically ceases when you leave your job or retire, and by then, you may not be able to enrol in another private health insurance scheme

In such cases, lower-tier IPs, or MediShield Life alone may be more sustainable.

Part 10: Integrated Shield Plan vs MediShield Life

MediShield Life focuses on essential coverage while Integrated Shield Plans extend coverage to non-subsidised care, broader outpatient treatments, and higher claim limits.

In general, if you are comfortable with subsidised care, MediShield Life may be sufficient. If you prefer private treatment, an integrated shield plan may offer better coverage. If you wish to evaluate whether an Integrated Shield Plan meets your healthcare needs, refer to this in-depth article: Is Integrated Shield Plan necessary in Singapore?

Table: MediShield Life vs Integrated Shield Plan (Key Factors)

| Feature | MediShield Life (MSL) | Integrated Shield Plan (IP) |

|---|---|---|

| Administrator | CPF Board | Private Insurers |

| Scope of Coverage | Sized for Class B2/C wards | Can cover up to private hospitals |

| Coverage Amount | Sub-limits apply, $200k/year | Often “as-charged”, higher annual claim limits |

| Pre- & Post-Hospitalisation | Not covered | Covered (varies by insurer) |

| Deductible/ Co-Insurance | Not covered | IP Rider can reduce the cost |

| Cash Value | None | None |

| Insurance Premium | Lower, fully payable with MediSave | Higher, MediSave limited to Additional Withdrawal Limit |

Part 11: Final Thoughts

An Integrated Shield Plan serves as a bridge between the basic safety net of MediShield Life and the higher costs of non-subsidised healthcare. It introduces flexibility and a wider range of options. When structured thoughtfully, it provides reassurance that a medical setback does not automatically translate into a financial one.

That said, this additional layer of protection comes with higher long-term financial commitments. Based on available data, the average lifetime premium for a plan covering both private and restructured hospitals may amount to around $201,000. Long-term affordability should therefore be a key consideration, especially as premiums rise with age.

In insurance planning, more coverage is not automatically better. The decision should rest on a rational assessment of your budget, medical preferences, and tolerance for uncertainty. What feels comfortable at 35 may appear very different at 65.

It is also important not to overlook the structural limitations of an Integrated Shield Plan. The main component of the IP does not cover deductibles and co-insurance – these remain out-of-pocket expenses. If you are concerned about these costs, consider the optional IP Rider.

The discipline lies in understanding what you need and what you are buying. Recognise its benefits, accept the trade-offs, and assess how it fits into your broader financial plan.

Part 12: Changelog

Part 12.1: Cancer Drug Treatments

Since 1 September 2022, MOH has implemented the Cancer Drug List (CDL). In essence, only treatments on the CDL are claimable under the IP, subject to the plan’s sub-limits. Treatments outside the CDL are not claimable under the IP.

First Published: 29 April 2020

Last Updated: 5 January 2026

Leave a Reply