MediShield Life is a basic health insurance plan that covers all Singaporeans and Permanent Residents. It helps you manage large hospital bills and selected costly outpatient treatments such as dialysis and chemotherapy for cancer. With lifelong coverage and inclusion of pre-existing medical conditions, MediShield Life ensures you will always have access to subsidised care at public hospitals. With this in mind, let’s break down how MediShield Life works in Singapore.

🎥 Prefer watching? Check out the video version of this post.

Table of Contents:

- What is MediShield Life

- Insurance Coverage (Benefits)

- Cash Value

- Insurance Premium (Cost)

- Limitations and Risks

- Claims

- Insurance Nomination

- Eligibility

- MediShield Life vs Integrated Shield Plan

- Final Thoughts

- Changes to MediShield Life

One Minute Summary:

- MediShield Life benefits is designed to cover all Singapore Citizens and Permanent Residents (PRs).

- Its primary purpose is to cover large subsidised medical bills, mainly in public hospitals under Class B2/C wards.

- Deductible and co-insurance are some out-of-pocket costs that you need to pay before any payout from MediShield Life.

- You can use the savings in your CPF MediSave Account to pay for the entire insurance premium.

- The Government provides various subsidies to ensure no one loses MediShield Life coverage because of financial difficulties.

- You may consider a private insurance scheme if you prefer non-subsidised healthcare.

Part 1: What is MediShield Life

MediShield Life is a non-participating, basic health insurance policy administered by Central Provident Fund Board (CPF Board) on behalf of the Ministry of Health. It is designed to cover large hospital bills and selected outpatient treatments. MediShield Life is governed under the MediShield Life Act 2015 (Act 4 of 2015).

Part 2: Insurance Coverage (Benefits)

Part 2.1: Main Benefits

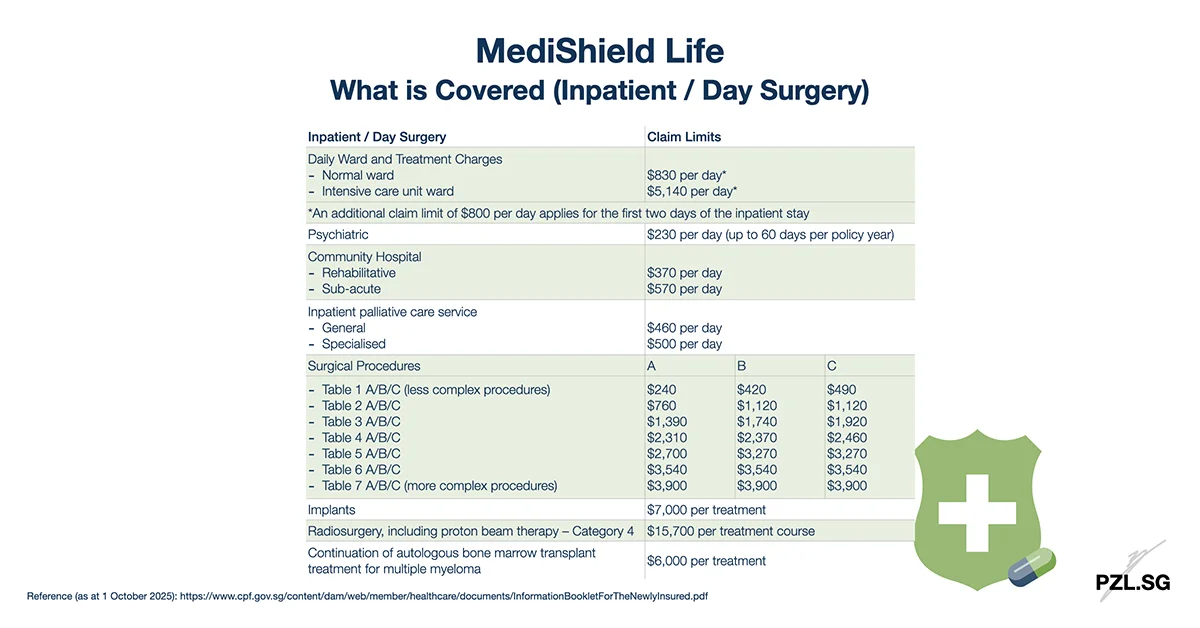

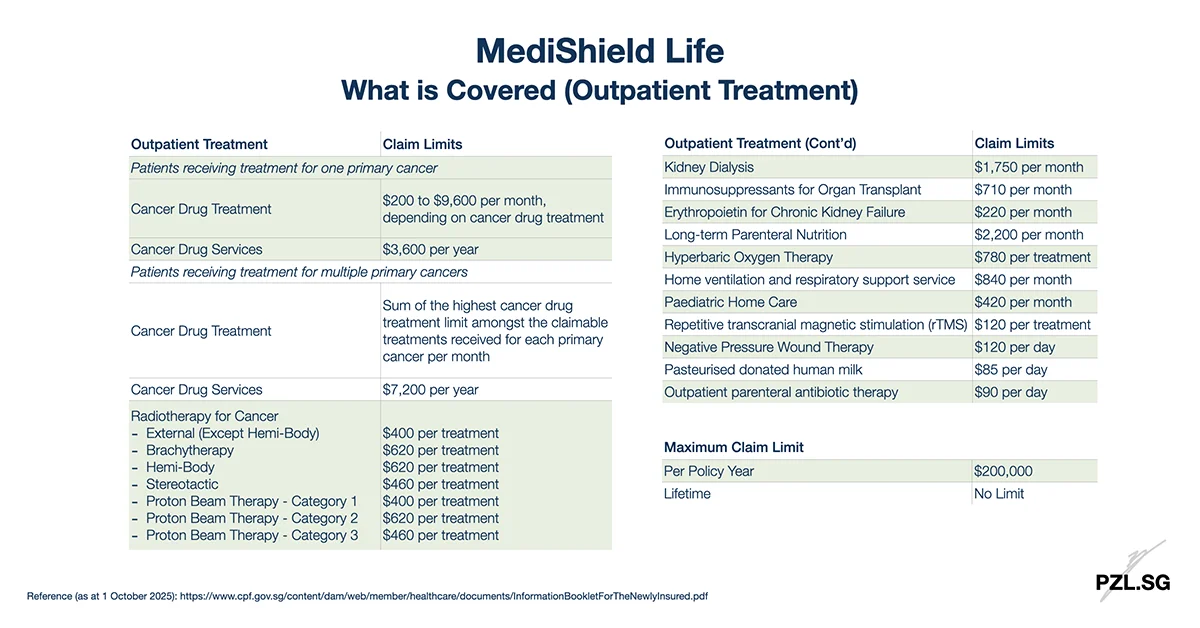

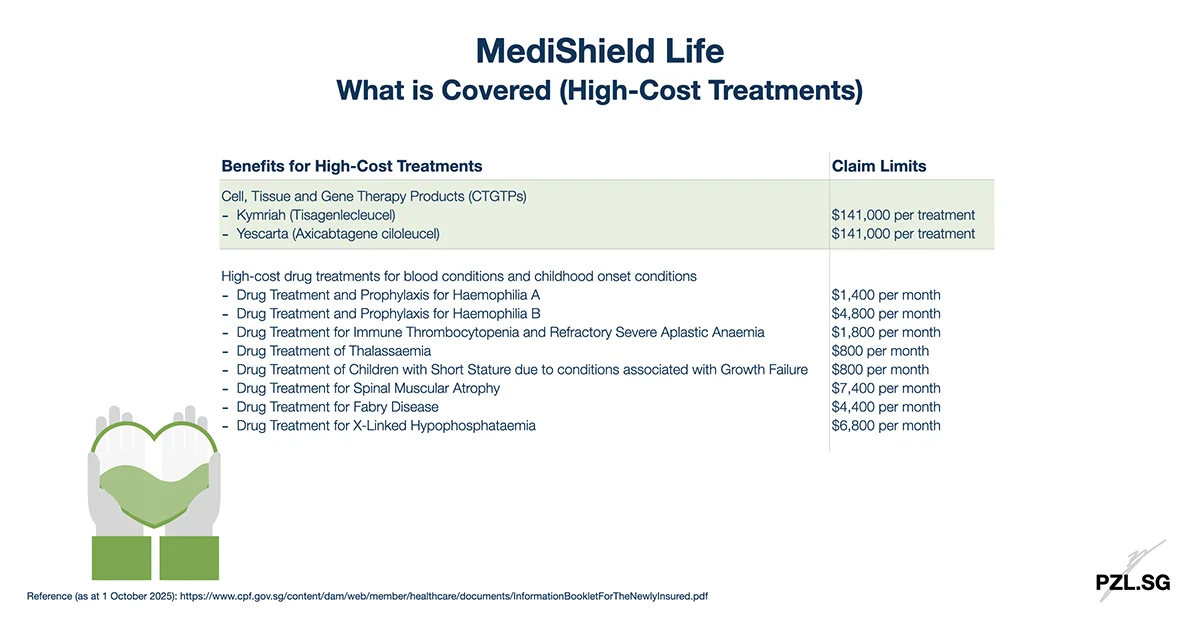

MediShield Life coverage is meant for subsidised Class B2/C wards in public hospitals. These benefits help reduce the financial burden from large medical bills, especially for chronic and severe illnesses. I have summarised the key benefits in the following three tables:

Part 2.2: Coverage Amount

MediShield Life provides up to $200,000 of coverage per policy year, and each treatment category has its own sub-limit. For example, you can claim up to $1,750 per month for kidney dialysis.

A policy year is the 12-month period starting from the date your policy begins or renews. For example, if your coverage began on 1 May, your policy year runs from 1 May this year to 30 April the following year. This is important as the treatment benefit limits reset every policy year, ensuring ongoing coverage for long-term illnesses such as cancer.

Part 2.3: Coverage Period

Similar to CareShield Life, MediShield Life provides lifelong insurance coverage for as long as you live. This lifelong protection ensures that you do not have to worry about healthcare cost, especially in older age.

Part 3: Cash Value

MediShield Life is a non-participating plan. This means:

- The plan does not accumulate cash value

- There is no surrender value

- There is no investment component

In other words, premiums are paid solely in exchange for medical coverage.

Part 4: Insurance Premium (Cost)

Part 4.1: Premium Determinants

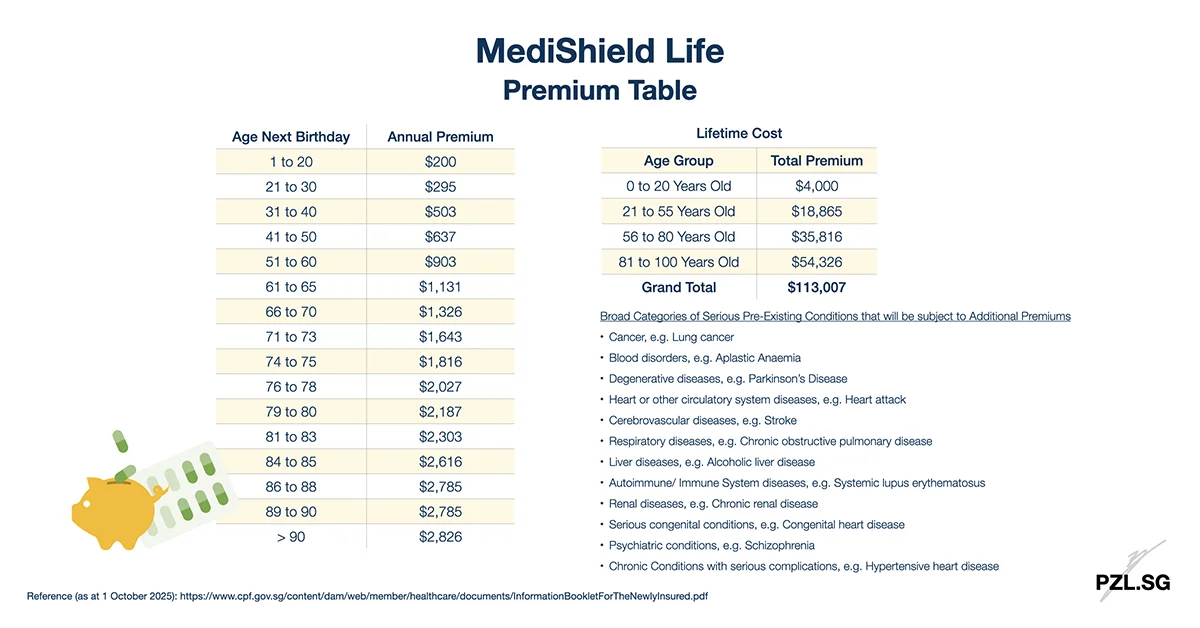

MediShield Life premiums are based on age and are payable each year.

During each renewal, CPF Board will use your Age Next Birthday (ANB) to determine your new insurance premium amount. Generally, this increases with age as the risk and healthcare cost increases over time.

Additionally, if you have a serious pre-existing medical condition, you may need to pay 30% Additional Premiums for the first 10 years.

But don’t worry! The Government provides various subsidies and support to ensure MediShield Life’s premium rates remain affordable. In fact, the Government pledges that you will not lose MediShield Life’s coverage due to inability to pay.

Part 4.2: Why Premiums Increase with Age

MediShield Life operates on a risk pooling model. This means premiums collected are used to help pay for those who need treatment. In general, the risk of claim and the cost of healthcare increase significantly with age. To ensure that the premium rates remain affordable, CPF Board pools the premiums from individuals in similar age cohorts.

Moreover, the Government also offers various subsidies and premium support initiatives to keep premiums affordable:

- Lower- to upper-middle-income Singapore Citizens and Permanent Residents (15% to 60%);

- Pioneer Generation Subsidies (40% to 60%);

- Merdeka Generation Subsidies (5% to 10%);

- Additional Premium Support – if you still cannot afford the premiums after subsidies and MediSave.

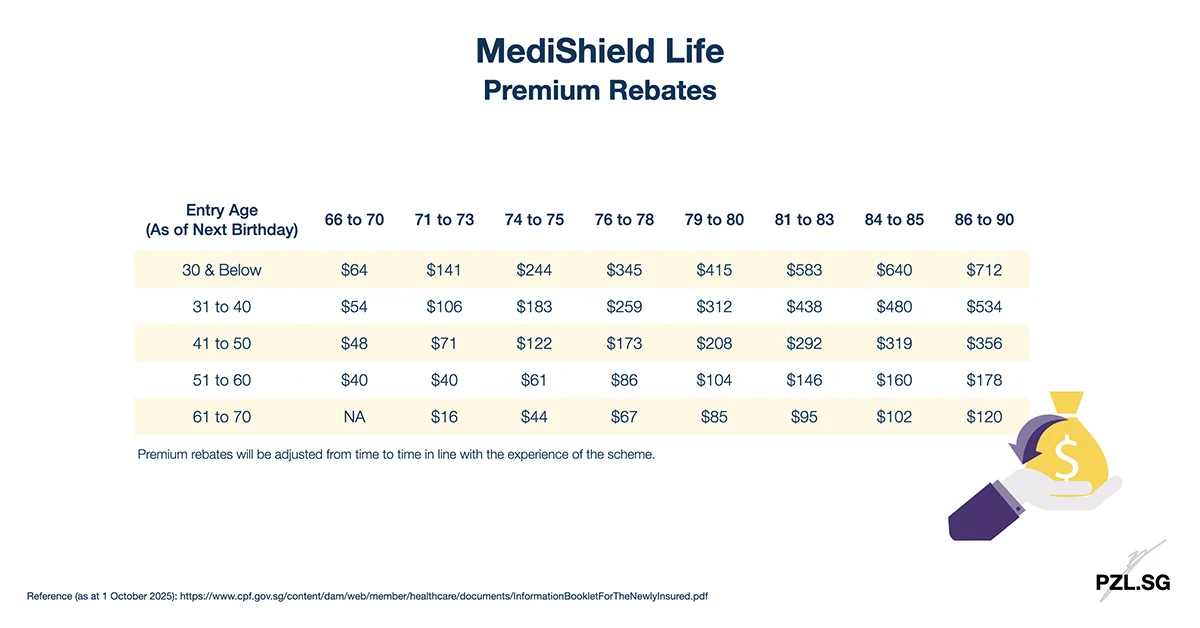

Part 4.3: Premium Rebates

To make lifetime premiums more manageable, the Government provides premium rebates from age 66 onwards. This methodology reduces the impact of higher premiums in older age. Generally, the earlier you are enrolled into MediShield Life, the higher the premium rebates you receive.

Part 4.4: Type of Payment

Premiums are fully payable using CPF MediSave. You can also use an immediate family member’s MediSave to assist with the premiums payment.

Part 4.4: Premium Paying Period

MediShield Life is a yearly renewably health insurance policy. This means you will need to pay the insurance premium every year throughout your life.

Part 5: Limitations and Risks

MediShield Life offers foundational protection that is sized for subsidised treatments at Class B2/C wards in public hospitals. With this in mind, there are some limitations you need to know.

Part 5.1: MediShield Life Claim Limits

MediShield Life has an annual limit of $200,000 per policy year. In addition, each treatment and service is subject to its own sub-limit. If you exceed any of these limits, you will need to pay the remaining costs via MediSave or in cash.

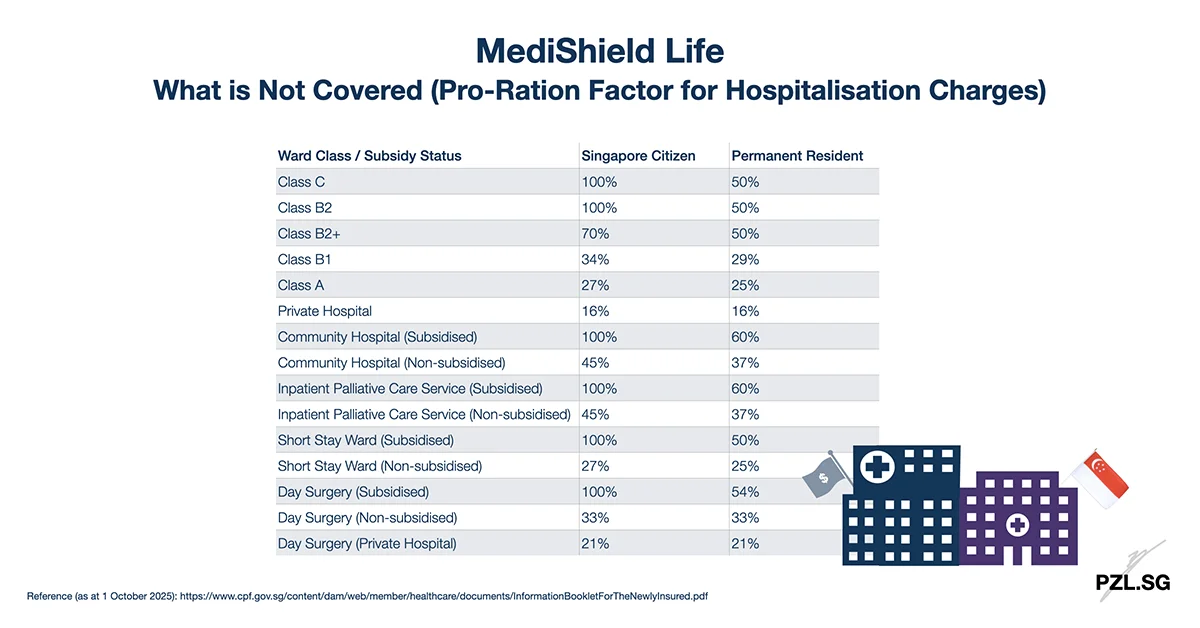

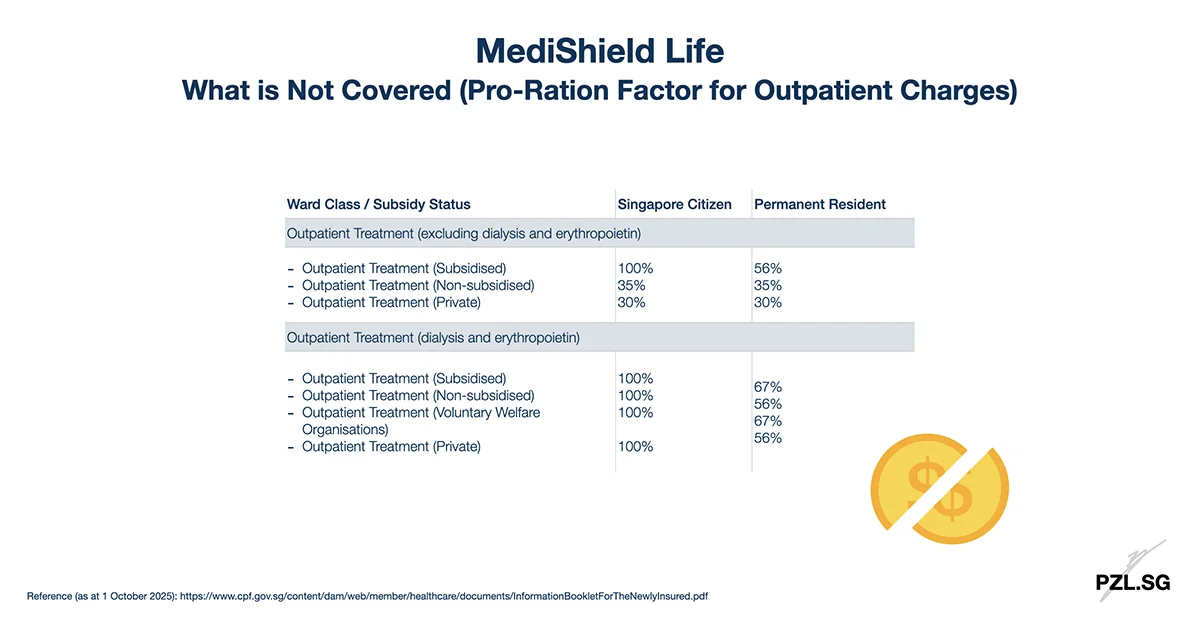

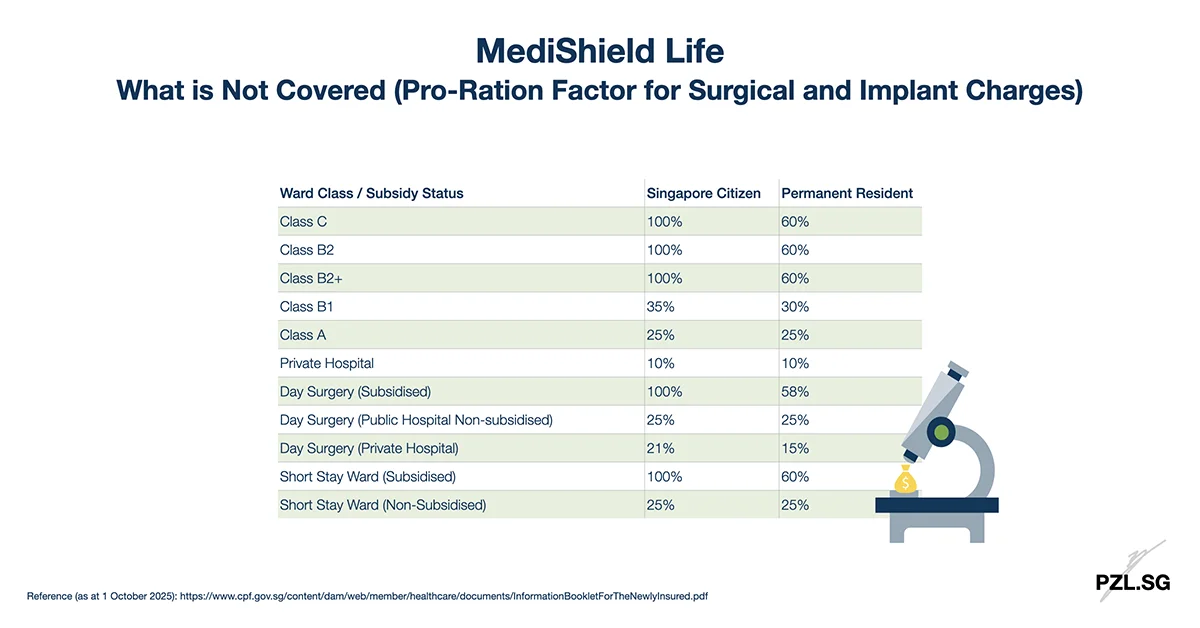

Part 5.2: Pro Ration Factor

Pro-ration reduces your claim amount when you choose non-subsidised care, e.g. Class A/B1/B2+ wards in public hospitals, or private hospitals

MediShield Life’s claim computation is also different for Singapore Citizens and Permanent Residents. In detail, for Singapore Citizens, pro-ration applies only when you choose non-subsidised treatments, e.g. Class A or B1 wards in public hospitals, or private hospitals. Meanwhile, for Permanent Residents, pro-ration applies even in subsidised Class B2/C wards.

To illustrate the impact of pro-ration, let’s consider an example for a Singapore Citizen:

- Type of procedure: Heart, blood vessel, minimally invasive bypass procedure (Code: SD742H)

- Choice of healthcare: Class A ward at National Heart Centre (public hospital)

According to the fee benchmark from Ministry of Health, 75% of the patients are charged around $43,159 for this procedure.

Since this is a non-subsidised treatment, MediShield Life will consider only 35% of the bill for its claim computation. This means you will need to pay at least $28,053.35 (take $43,159 x 65%) for the surgery.

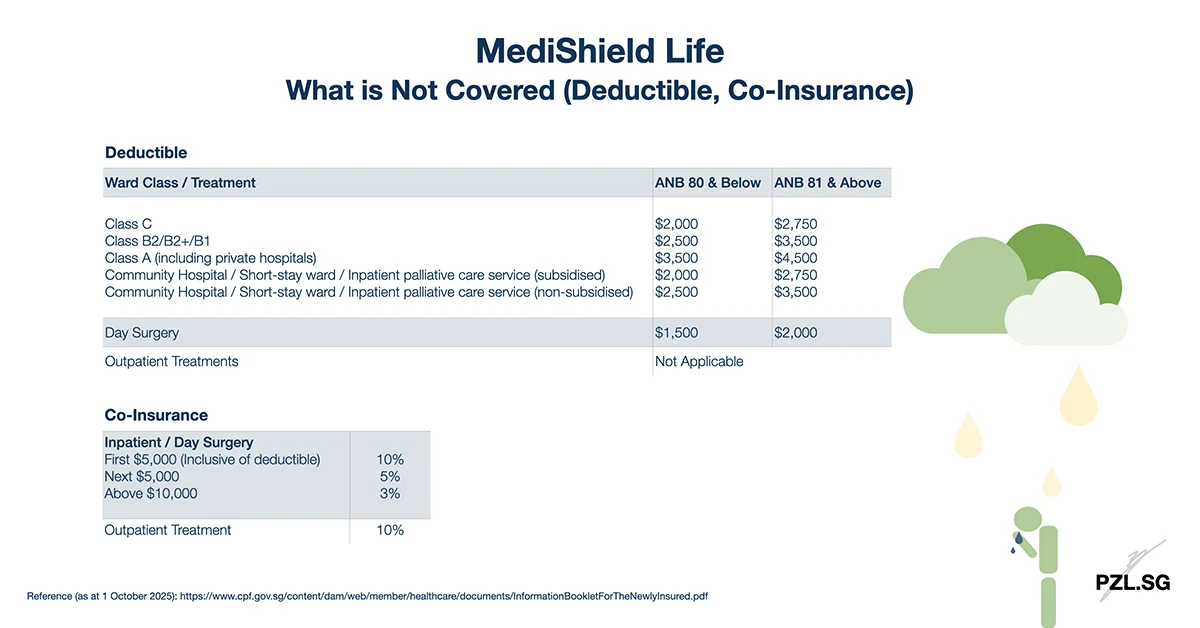

Part 5.3: Deductible

After taking into account the pro-ration factor (if applicable), you need to pay a deductible component. This is a fixed amount you must pay before MediShield Life begins to pay. You need to pay the deductible once in a policy year.

This ensures that MediShield Life focuses on the large bills, not the small ones.

Part 5.4: Co-Insurance

After the deductible, you must pay co-insurance. This is a percentage of the claimable amount. Co-insurance applies to every bill.

This ensures cost-sharing and encourages responsible healthcare usage.

Part 5.5: Pre-Hospitalisation

MediShield Life does not cover pre-hospitalisation consultations, diagnostic scans, and tests that were conducted before admission.

Part 5.6: Post-Hospitalisation

Similarly, post hospitalisation such as follow-up consultations, prescription, and rehabilitation are also not covered.

Part 5.7: Exclusions

Although MediShield Life covers pre-existing conditions, it does not cover all types of treatment fees. Here are some examples of the conditions that MediShield Life do not cover:

- Ambulance fee;

- Cosmetic surgery;

- Dental work (except due to accidental injuries);

- Maternity charges (including Caesarean operations) or abortions, including related complications, except treatments for serious complications related to pregnancy and childbirth;

- Overseas medical treatment.

As can be seen, MediShield Life focuses strictly on essential, subsidised treatments.

Part 6: Claims

Part 6.1: Claim Process

To make a claim, simply inform the medical institution. Thereafter, the medical institution will submit the claim electronically to CPFB.

Once approved,

- MediShield Life pays the claimable amount to the hospital directly.

- You may use CPF MediSave to pay your share of the bill, up to the CPF withdrawal limit.

- Any balance must be paid in cash.

Now, let’s examine how MediShield Life’s claim computation works.

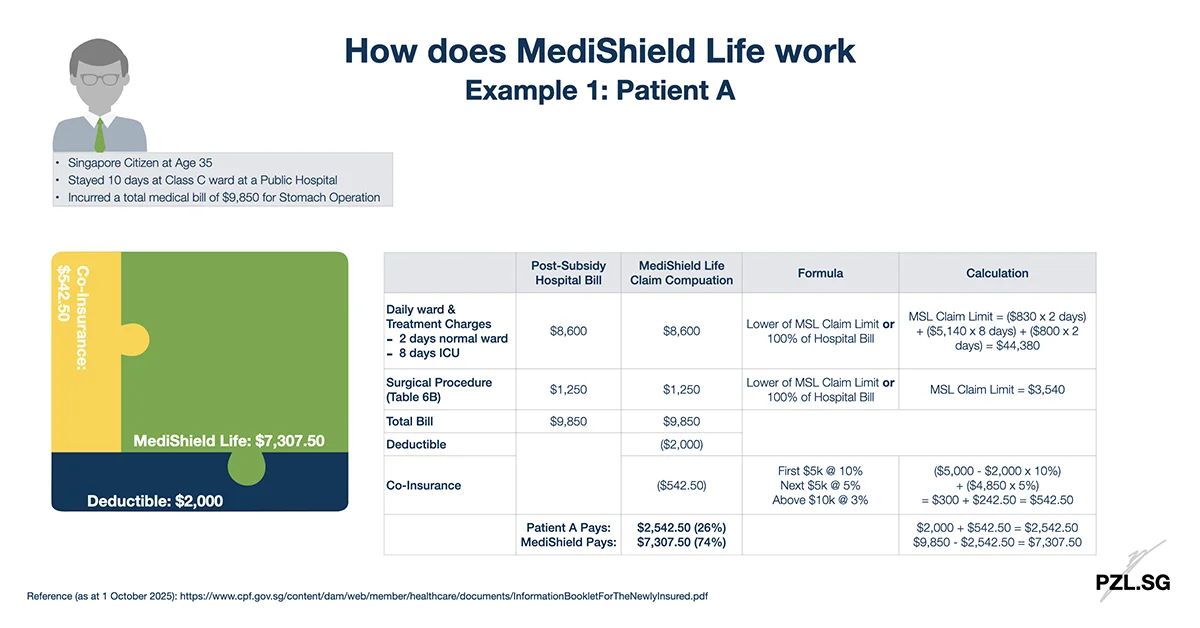

Part 6.2: Example 1 – Patient A

Firstly, let’s look at Patient A and this is his profile:

- Singapore Citizen at Age 35;

- Stays at Class C ward in Public Hospital;

- Incurred a total bill of $9,850 for a Stomach Operation.

In this example, this is the breakdown for the medical bill:

- Firstly, Patient A needs to pay a fixed cost of $2,000 for the deductible.

- Next, he needs to pay a co-insurance of $542.50. (Refer to the above Example 1 for the calculation.)

- Finally, MediShield Life will cover the remaining bill.

In total, Patient A pays a total of $2,542.50 out-of-pocket, while MediShield Life covers $7,307.50.

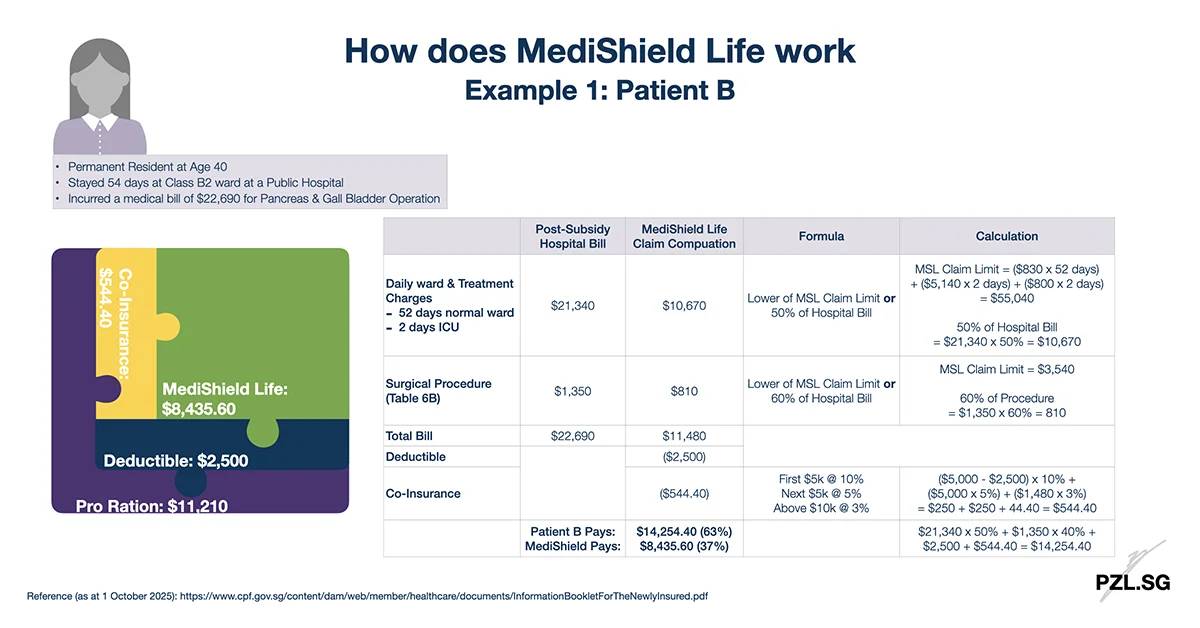

Part 6.3: Example 2 – Patient B

Next, let’s look at another example to learn how to calculate the Pro-Ration Factor. This is Patient B’s profile:

- Singapore Permanent Resident at Age 40;

- Stays at Class B2 ward in Public Hospital;

- Incurred a total bill of $22,690 for a Pancreas & Gall Bladder Operation.

Since Patient B is a Permanent Resident, we need to apply a pro-ration factor to her medical bill. Here is how it works:

- For the hospitalisation charges, MediShield Life will consider only 50% of the medical bill for its claim computation, i.e. $21,340 x 50% = $10,670. (You may refer to the table in Part 5.2 to learn more about the Pro-Ration Factor).

- For the surgical charges, MediShield Life will consider 60% of the medical bill for its claim computation, i.e. $1,350 x 60% = $810.

- Patient B needs to pay a fixed cost of $2,500 for the deductible.

- Next, Patient B needs to pay a co-insurance of $544.40.

- Finally, MediShield Life will cover the remaining bill.

In sum, Patient B pays a total of $14,254.40 out-of-pocket, while MediShield Life covers $8,435.60. As I have explained earlier, the Pro-Ration Factor will affect the amount that MediShield Life covers for the medical bill.

Part 7: Insurance Nomination

MediShield Life does not provide death benefits. As such, insurance nomination does not apply.

Part 8: Eligibility

MediShield Life is compulsory and it covers

- All Singapore Citizens from birth; and

- All Permanent Residents from the day they attain residency.

This coverage is automatic, regardless of age or health.

Part 9: MediShield Life vs Integrated Shield Plan

MediShield Life focuses on covering the essential healthcare needs while Integrated Shield Plans (IPs) offer additional coverage, especially for:

- Non-subsidised care, e.g. Class A/B1/B2+ wards in public hospitals, or private hospitals,

- Pre- and post-hospitalisation treatment,

- Wider range of outpatient treatments.

In general, if you are comfortable with subsidised care, MediShield Life may be sufficient. If you prefer private treatment, an Integrated Shield Plan may offer better coverage. If you wish to evaluate whether MediShield Life meets your healthcare needs, refer to this in-depth article: Is MediShield Life enough in Singapore?

Table: MediShield Life vs Integrated Shield Plan (Key Factors)

| Feature | MediShield Life (MSL) | Integrated Shield Plan (IP) |

|---|---|---|

| Administrator | CPF Board | Private Insurers |

| Scope of Coverage | Sized for Class B2/C wards | Can cover up to private hospitals |

| Coverage Amount | Sub-limits apply, $200k/year | Often “as-charged”, higher annual claim limits |

| Pre- & Post-Hospitalisation | Not covered | Covered (varies by insurer) |

| Deductible/ Co-Insurance | Not covered | IP Rider can reduce the cost |

| Cash Value | None | None |

| Insurance Premium | Lower, fully payable with MediSave | Higher, MediSave limited to Additional Withdrawal Limit |

Part 10: Final Thoughts

MediShield Life forms the bedrock as our national basic health insurance scheme. It offers lifelong, universal, and affordable protection, focusing on

- Singapore Citizens; who

- Seeks subsidised treatment in Class B2 or Class C wards in public hospitals; or

- Seeks subsidised outpatient or day surgery treatments in public hospitals.

Various government subsidies and support are in place to ensure that no Singaporean is denied essential healthcare due to financial constraints. This provides you with a peace of mind if you need medical attention.

However, MediShield Life does have limitations. For example, if you prefer private healthcare, then MediShield Life alone will not be enough. In this case, you may wish to explore purchasing an integrated shield plan.

Overall, MediShield Life works together with:

- MediSave Account, for paying deductible and co-insurance

- Integrated Shield Plans, for enhanced coverage

- MediFund, as a safety net for those who are unable to afford the remaining bills

These three layers shapes Singapore’s healthcare system as a robust, sustainable, and an inclusive one.

Part 11: Changes to MediShield Life

15 October 2024: Enhancements to MediShield Life

The Government has accepted the MediShield Life Council’s recommendations to expand and strength MediShield Life’s coverage starting April 2025.

1 September 2022: Review of Coverage for Outpatient Cancer Drug Treatments

Ministry of Health announced changes to the financing of outpatient cancer treatment. In detail, these changes help to ensure that MediShield Life’s premium and the cost of cancer treatments remain affordable over time.

1 March 2021: MediShield Life 2020 Review

The MediShield Life Council has recommended changes to MediShield Life’s premium and benefits. These changes ensure that our nation’s health insurance scheme remain sustainable and relevant to the needs of Singaporeans.

Read More: Changes to MediShield Life Singapore in March 2021

Leave a Reply