In truth, it can be a daunting task to understand the various types of insurance policies in Singapore. Despite that, we need to equip ourselves with adequate knowledge to help us make the right decisions. With this in mind, let’s understand the basics in this post.

Table of Contents:

- Life and Health Insurance Policies

- Savings and Investment

- General Insurance

- Conclusion on the types of Insurance Policies

One Minute Summary:

- In summary, there are three types of insurance policies – life and health, savings and investment, and general insurance.

- By and large, we can use an insurance policy to transfer the financial risk to an insurer.

- A life and health insurance policy provides a payout for any of the covered events, e.g. critical illness.

- A savings and investment plan is a disciplined approach to grow your wealth.

- General insurance provides financial protection for your prized assets.

Part 1: Life & Health Insurance Policies

As a matter of fact, we are the biggest asset that we own. Therefore, it is only right for us to take care of ourselves.

Part 1.1: Main Purpose

Basically, a life and health insurance policy covers well, your life and health (no pun intended). In general, we will associate such coverage with a life’s major turning point, e.g.

- Pre-mature death;

- Severe disability;

- Critical illness;

- Medical expenses;

- Long-term care.

Part 1.2: Why do You need a life and health insurance policy?

In order to answer this question, we need to go back to the basics – understanding yourself. In detail, we need to identify your current life stage and to start planning for your future. Above all, a life and health insurance policy is a risk management tool to solve three major problems in life,

- dying too early;

- inability to work till retirement; and

- exhausting hard-earned savings too quickly.

Be that as it may, the following infographic summarises our common needs.

For instance, you need life insurance when you have a family member that depends on your income. In like manner, we may also use a life insurance policy to cover your liabilities. Otherwise,

will your family member be able to afford to pay off your outstanding loans?

Part 1.3: How much insurance coverage do You need?

As much as I wish to have a crystal ball to calculate the exact financial gap, none exists in reality. For that reason, we need to conduct comprehensive financial planning to this end. In effect, this instils clarity into your future. Thereupon, it drives meaning into the numbers that we put into your insurance coverage.

To begin with your financial planning journey,

- Either speak with a qualified financial planner for professional advice; or

- Do further research on your own and become your own advisor.

Even if you are an expert in the field, it may be wise to seek a professional second advice. This is with the intention to cover potential blind spots.

Part 1.4: Types of Insurance Policies available

Within the life and health category itself, there are six types of insurance policies to serve different needs.

- Term Insurance;

- Participating Whole Life Insurance;

- Investment-Linked Policy;

- Personal Accident Insurance;

- Hospitalisation Insurance

- Disability Income Insurance

Altogether, they ensure that you are adequately covered for all life’s major events.

Part 1.5: Example of a Life and Health insurance policy

For one thing, the Singapore government takes on initiatives to provide us with a basic foundation in our insurance coverage. To list out, here are three of them that you may know.

Part 1.5.1: MediShield Life

In brief, MediShield Life is the core of our nation’s healthcare policy. Summing up, it provides coverage against medical bills for hospitalisation and certain approved outpatient treatments.

Part 1.5.2: Dependants’ Protection Scheme

In contrast, Dependants’ Protection Scheme is a yearly renewable term insurance policy. In detail, it provides a lump sum payout in the event of death, terminal illness, and total permanent disability.

Part 1.5.3: CareShield Life

Finally, CareShield Life is our nation’s new severe disability insurance scheme. On the condition that you become severely disabled, you will get a monthly cash payout. What’s more, you will continue to receive the payout for as long as you remain disabled.

Part 2: Savings & Investment

From time to time, we may use an insurance policy as a tool to help us reach our financial goals. In this case, we look at the savings and investment category.

Part 2.1: Main Purpose

At any rate, a savings and investment plan provides stronger leverage for the dollar. Under those circumstances, the same effort (i.e. capital, and time period) yields a higher return. This is because of the compounding effect of money.

Part 2.2: Why do You need a Savings and Investment plan?

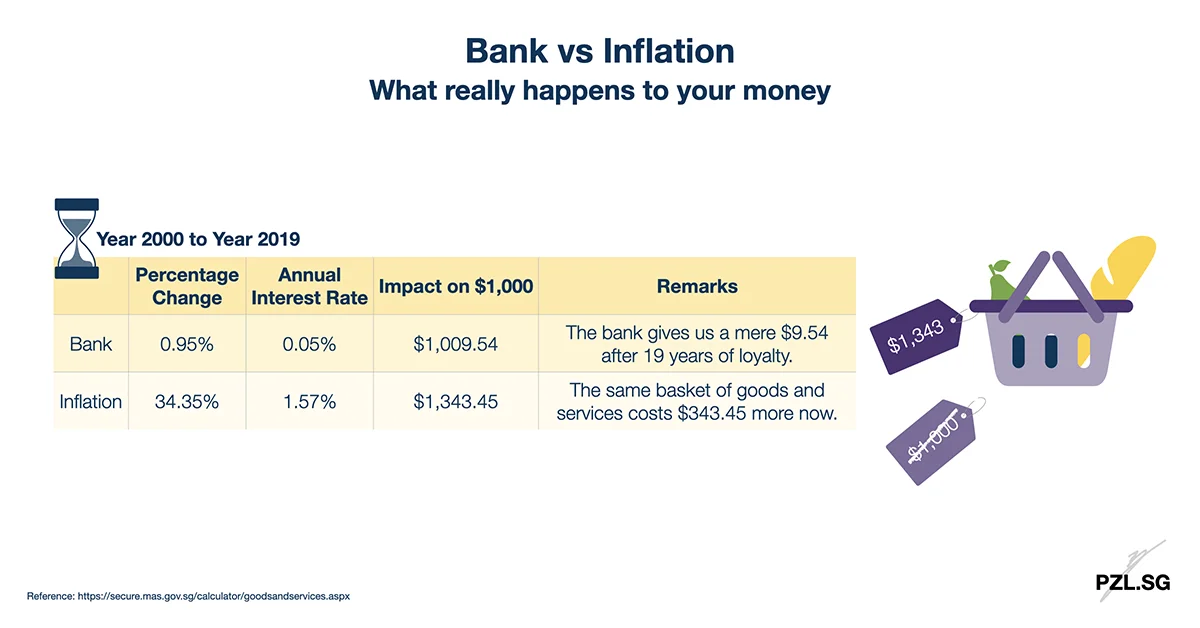

Evidently, we need money to pay for goods and services. Given that time is always counting down, we need a tool to help us save more efficiently. Otherwise, inflation will erode our hard-earned money eventually. To demonstrate, this is what’s happening in the real world.

Emphatically, the bank’s yield is almost guaranteed to be lower than the rate of inflation each year. Under those circumstances, your money loses in value in due time.

Part 2.3: How much money do You need?

As much as you agree that we will need more money in the future, the question remains

how much do you need exactly?

While I don’t know your goals in life, there are five big-ticket items that you may encounter:

- Car and maintenance;

- Wedding and banquet;

- House and renovation;

- Living expenses and children’s education;

- Retirement and long-term care.

To point out, we will pay for these items across different stages of our lives. Accordingly, we shall adopt financial planning early to help us reach the same goal with lesser effort.

Part 2.4: Types of Plans available

On this occasion, we are looking at one of following four options:

- Participating Endowment plan;

- Non-participating Endowment plan;

- Investment-Linked Policy;

- Universal Life Insurance Policy

Part 2.5: Example of a Savings and Investment Plan

To illustrate, let’s use one of the popular tools today – the Singlife Account. In sum, it boasts a non-guaranteed crediting rate of up to 3.5% per annum. By comparison, this is certainly higher than most bank’s interest rate.

Part 3: General Insurance

After spending two huge sections on protecting ourselves and to grow our wealth, we will protect our assets now.

Part 3.1: Main Purpose

In essence, general insurance provides financial protection for the assets that you own. To list out some examples,

- Motor vehicles;

- House and renovation;

- Luggage and travel;

- Jewellery and items with an exorbitant price.

After all, these are expensive assets that we exchange our hard-earned money for. Hence, it makes sense to insure its value.

Part 3.2: Why do You need General Insurance?

All things considered, it may become too costly to replace the item at its face value. Conversely, we may pay a small amount of money to the insurance company to insure the item. In the event that the item is damaged or lost, we get a compensation for the item’s value.

Part 3.2: Types of Insurance Policies available

All in all, the possibilities are infinite, depending on your actual needs. As an illustration, a travel insurance covers for losses arising from travel inconvenience, e.g. flight delay. On the other hand, a motor insurance covers the repair bill for damages to your vehicle.

Part 4: Conclusion on the types of Insurance Policies

In conclusion, we use different insurance policies to hedge against different risks. This is usually because we are unable or unwilling to bear the financial loss ourselves. Thus, we pay a fraction of the cost to transfer the risk to the insurer. In order to do this right, we need to understand and to buy the right insurance policy.

Henceforth, we will rely on our trusted insurance agent to provide responsible financial advice. Accordingly, this helps us to gain valuable insights within a shorter time frame. Despite that, it remains helpful to have basic knowledge on the insurance policies that are offered in the market.

This is especially important because we are responsible for the decisions that we make in our life.

Checklist:

- When was the last time you did a comprehensive insurance portfolio review?

- Are your insurance policies consolidated into a portfolio summary?

- Are you overpaying for your insurance polices?

First Published: 9 January 2019

Last Updated: 30 September 2020

Leave a Reply