A child’s personal accident insurance policy tends to include benefits tailored to a child’s unique needs. These benefits and features may not be standard in all the personal accident insurance policies. With this in mind, I compared 15 different plans to identify the most suitable personal accident insurance policy for my child.

Table of Contents:

- My Purpose of Purchasing a Child Personal Accident Insurance Policy

- Child Personal Accident Insurance Policies that Meet My Criteria

- Cost-to-Benefit Ratio

- Should You Get a Child Personal Accident Insurance Policy

- When to purchase a Child Personal Accident Insurance Policy

- Caveat

- Insurance Benefits That Are Not Essential (Opinion)

- Child’s Personal Accident Insurance Policies that did not meet the criteria

One Minute Summary:

- Basically, a child’s personal accident insurance policy will include insurance benefits that cater to the child’s unique needs. These benefits may not be present in all the personal accident insurance policies.

- To sum up, my child’s personal accident insurance policy must include medical reimbursement for 1) an injury from an accident; 2) Dengue Fever; 3) food poisoning; 4) Hand, Foot, and Mouth Disease; and 5) insect bites.

- This is because I feel that such incidents have a high probability of occurrence. As a result, I’m unwilling to bear this financial risk on my own. Instead, I prefer to transfer the financial risk to the insurer so that I can enjoy a peace of mind.

- To determine the best personal accident insurance policy for a child, I reviewed the insurance contract of each policy to ensure that it can meet my specific needs.

- Thereafter, I calculated the Cost-to-Benefit Ratio to identify the personal accident insurance policy that offers the best value for money.

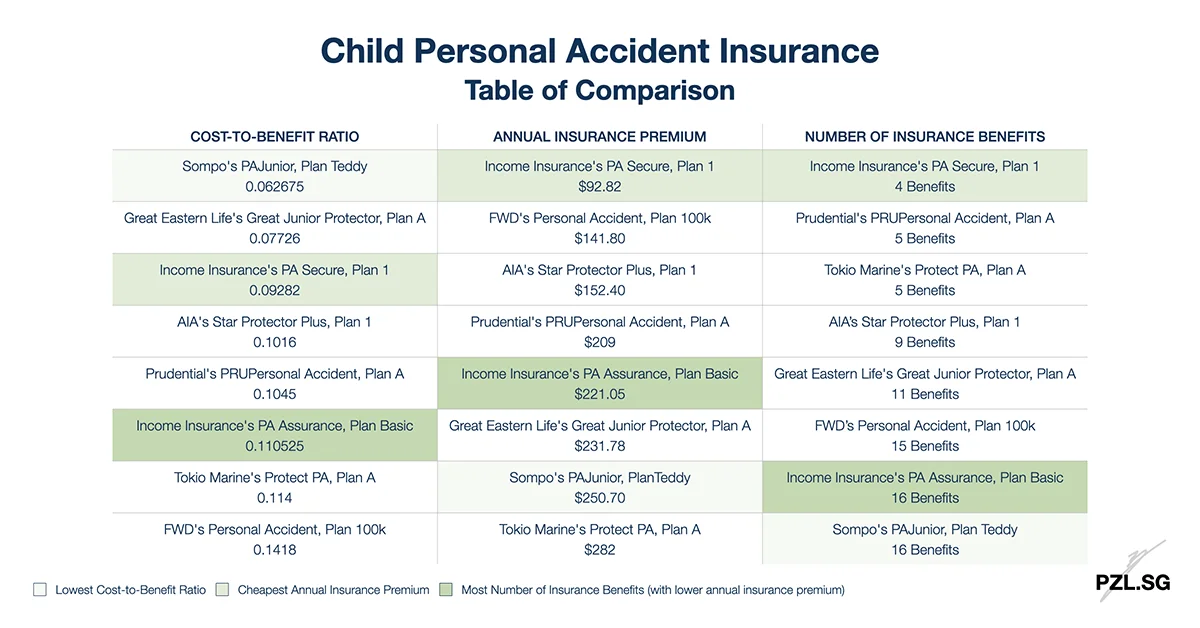

- If you prefer to have the plan with the lowest Cost-to-Benefit Ratio, then you may consider Sompo’s PAJunior’s Plan Teddy.

- If you prefer to have the with the cheapest annual insurance premium, then you may consider Income Insurance’s PA Secure.

- If you prefer to have the plan with the most number of insurance benefits, then you may consider Income Insurance’s PA Assurance.

Part 1: My Purpose of Purchasing a Child Personal Accident Insurance Policy

Before we begin, it is important to realise that we may have different requirements for our child’s personal accident insurance policy. As a result, we might use a different set of criteria to identify the most suitable plan for our child. With this in mind, I suggest using my analysis as a reference to conduct your own research. This approach ensures that you can find the most suitable personal accident insurance policy for your child.

In summary, for my child’s personal accident insurance policy, I wish to prioritise reimbursement for costly outpatient medical treatments. To explain, my view of a costly medical treatment is one that exceeds the insurance policy’s annual premium. Otherwise, I may be better off retaining the financial risk on my own. Secondly, these outpatient treatments should include insurance coverage for an injury due to an accident. In detail, amongst the other conditions, it should cover incidents such as an injury after an accidental fall, food poisoning, and insect bites. Additionally, the accident insurance policy should also provide insurance coverage for infectious diseases. For this purpose, I’m most concerned with Dengue Fever, and Hand, Foot, and Mouth Disease (HFMD).

Part 2: Child Personal Accident Insurance Policies that Meet My Criteria

In summary from Part 1, these are the two main criteria that I have for my child’s personal accident insurance policy:

- Firstly, the personal accident insurance policy must provide medical reimbursement benefits for 1) an injury from an accident; 2) food poisoning; 3) insect bites; 4) Dengue Fever; and 5) Hand, Foot, and Mouth Disease.

- Secondly, the insurance premium rate should be affordable. Since affordability is relative, we will use the Cost-to-Benefit Ratio to determine whether the cost of the personal accident insurance policy is reasonable (read Part 3).

Based on the above-mentioned criteria, these are the nine personal accident insurance policies that meet my criteria:

- AIA’s Star Protector Plus;

- FWD’s Personal Accident;

- Great Eastern Life’s Great Junior Protector;

- Income Insurance’s PA Assurance;

- Income Insurance’s PA Secure;

- Prudential’s PRUPersonal Accident;

- Sompo’s PAJunior;

- Tokio Marine’s Protect PA.

Part 3: Cost-to-Benefit Ratio

Part 3.1: Assumptions

Different insurers charge a different rate of insurance premium for their personal accident insurance policy. To determine whether the insurance premium rate is reasonable to meet my needs, I will conduct a Cost-to-Benefit Ratio check. For this purpose, I will calculate the Cost-to-Benefit Ratio based on the annual rate of insurance premiums and the medical reimbursement benefit. This is because these are the two key criteria that I look out for in my child’s personal accident insurance policy.

As a result of the factors that I have used in my Cost-to-Benefit Ratio, the outcome may be skewed. After all, I did not take the other insurance benefits and features into consideration. To sum up, the following are the assumptions that I have made to conduct this comparison:

- The personal accident insurance policy must include the relevant insurance coverage that I have listed in Part 2.

- To maintain affordability, I will select the cheapest personal accident insurance policy that can fulfil my criteria (Part 2).

- Although some of the personal accident insurance policies have a sub-limit for Infectious Diseases, I will use the broader Accident Medical Reimbursement benefit to conduct the Cost-to-Benefit Ratio check.

- Further to Point 3, you may read more about the personal accident insurance policy’s caveats (if any) in Part 6 of this post.

Part 3.2: The Comparison Results

All things considered, the following infographic summarises my comparison results.

Basically, the Cost to Benefit Ratio measures your cost outlay against the claim benefit that you (may) receive from the personal accident insurance policy. Generally, a lower ratio suggests that you have received a higher insurance claim benefit as compared to the insurance premium that you have paid. On the contrary, a higher ratio suggests that you have paid a higher insurance premium as compared to the insurance claim benefit that you have received. As compared to looking at the insurance premium rate alone, I feel that the Cost-to-Benefit Ratio is a more refined measurement.

Next, I have also ranked the personal accident insurance policies according to the number of insurance benefits that they provide. That being said, I’m unsure of whether there is any significance to this ranking. After all, it is not always true that the more the number of insurance benefits, the better the insurance policy is. Instead, what’s more important is still the relevancy of these insurance benefits to your child’s needs.

Part 4: Should You Get a Child Personal Accident Insurance Policy

Part 4.1: Cost to Benefit Ratio

In general, we can view insurance as a financial instrument to give you the financial leverage for the money that you need but do not have. In the case of a personal accident insurance policy, some of us may have $1,000 that we can use to meet our child’s medical needs. Consequently, it is possible to retain this financial risk on our own. Despite that, when we compare the Medical Reimbursement benefit against the insurance premium, most personal accident insurance policies have a relatively low Cost-to-Benefit Ratio. Consequently, this result suggests that there is a higher value in the insurance benefit (as compared to the insurance premium outlay).

Moreover, all these personal accident insurance policies have more than one insurance benefit. As a result, this lowers the Cost-to-Benefit Ratio even further. Accordingly, this further suggests that we can enjoy a reasonable amount of insurance benefits from a personal accident insurance policy.

Part 4.2: Probability of Occurrence

Next, we may also evaluate the need for a personal accident insurance policy by looking at the probability of occurrence. In my case, my one-year-old child has started walking and is learning how to climb now. As a young learner, there tends to be a higher risk of accidental falls and injuries. Additionally, she likes to put all sorts of items into her mouth (risk of food poisoning). In a few months, we will enrol our child into a preschool (risk of Hand, Foot, and Mouth Disease, insect bites). With these considerations in mind, I feel that there is a relatively high probability of occurrence and I’m unwilling to bear these outpatient medical costs on my own.

Accordingly, this explains why I decided to purchase a personal accident insurance policy for my child. It is not just about purchasing any generic personal accident insurance policy off the shelf. To point out, this personal accident insurance policy must include insurance coverage for infectious diseases. In detail, it must include Hand, Foot, and Mouth Disease as one of the infectious diseases (apparently, not all insurers define Infectious Diseases the same way).

Part 4.3: A Peace of Mind

As I have mentioned earlier, the Accident Medical Reimbursement benefit (that includes infectious diseases) is the main reason why I got a personal accident insurance policy for my child. Based on the outcome of the Cost-to-Benefit Ratio check in Part 3, Sompo’s PAJunior’s Plan Teddy has the lowest Cost-to-Benefit of 0.0626. In detail, Sompo charges $250.70 a year for the Teddy Plan (its cheapest plan) and it covers up to $4,000 for Medical Expenses.

On the other hand, if I were to save $250.70 on my own every year, then it would take me almost 16 years to save up to $4,000. For one thing, that is a long time. Therefore, I feel that it makes sense for me to transfer the financial risk to the insurer instead.

Part 5: When to purchase a Child Personal Accident Insurance Policy

At this time, many insurers allow you to submit an insurance application as soon as your child is 15 days old. Accordingly, this is the earliest possible time for you to insure your newborn.

Although all newborns won’t be able to move around on their own yet, this does not mean that they are safe from danger all the time. For instance, with many cases of Dengue Fever in Singapore, this situation certainly poses a threat to our little ones. Moreover, it makes administration a breeze when you purchase both a child’s personal accident insurance policy and an integrated shield plan at the same time. This is as compared to having to remember different dates for your child’s insurance policy’s renewal.

Part 6: Caveat

AIA’s Star Protector Plus

It is uncertain whether this personal accident insurance policy will provide medical reimbursement for medical treatment for insect bites. This is because AIA did not specify this scope of insurance coverage in both its Product Brochure and its Product Summary. For the most part, this is unlike its counterpart, AIA Solitaire PA (II). For Solitaire PA (II), it clearly states that it will cover medical reimbursement for medical treatment for insect bites.

Given the ambiguity, I reached out to AIA’s backend team for clarification. Unfortunately, I received conflicting information from different representatives. One of them shared that we can submit a claim as an “accident”. Thereafter, AIA’s Claims Department will assess the claim to determine whether it is admissible. Conversely, another representative initially stated that Star Protector Plus does not cover insect bites. However, upon further inquiry, she clarified that this personal accident insurance policy does cover bodily injury from insect stings or animal bites, subject to terms and conditions.

FWD’s Personal Accident

There is a 90-day waiting period for insurance coverage for infectious diseases and food poisoning. Furthermore, although FWD considers the contracting of an infectious disease or food poisoning as an accident, it will only pay up to 50% of the relevant benefit limit. To illustrate, if the claim limit for medical expenses is $2,000, then you can only claim up to $1,000 for food poisoning. Thirdly, if the insured is a child, then FWD will only cover 50% of the benefit limit for Medical expenses. Consequently, if the claim limit for medical expenses is $2,000, then you can only claim up to $2,000 x 50% x 50% = $500 for food poisoning.

Great Eastern Life’s Great Junior Protector

For the Accidental Medical Expenses Reimbursement benefit, there is a sub-limit of $500 for Food Poisoning, Dengue Fever, Hand, Foot, and Mouth Disease, and Zika Virus.

Income Insurance’s PA Assurance

You will need to pay an additional insurance premium to get covered for infectious diseases.

Income Insurance’s PA Secure

From its Product Brochure and Policy Wording, it is uncertain whether Income Insurance’s PA Secure provides medical reimbursement for medical treatment for insect bites. This is unlike its counterpart, Income Insurance’s PA Assurance. For PA Assurance, it clearly states that it will cover medical reimbursement for medical treatment for insect bites.

Given the ambiguity, I reached out to Income Insurance’s backend team for clarification. Initially, I received conflicting responses. But eventually, I obtained an official confirmation that PA Secure covers both insect and animal bites. However, for infectious diseases resulting from these bites, the coverage is limited to the seven infectious diseases listed in PA Secure’s Policy Wording.

Sompo’s PAJunior

To be covered for infectious diseases, you will need to purchase the more expensive tier of its personal accident insurance policy. Additionally, there is a 14-day waiting period for insurance coverage for infectious diseases.

Part 7: Insurance Benefits That Are Not Essential (Opinion)

To sum up, most personal accident insurance policies have at least four different insurance benefits; some plans have as many as sixteen different insurance benefits. Despite that, not all of these insurance benefits are important for my consideration. For example, most personal accident insurance policies will provide a benefit payout in the event of the insured’s Accidental Death. To explain, Accidental Death refers to the death of the insured within twelve months from the date of the accident. Accordingly, to claim this insurance benefit, the death must occur as a result of an injury. On the other hand, the death benefit in a term life or whole life insurance policy tends to have a broader definition for a claim. Generally, this includes death due to natural causes or an illness. With this in mind, I won’t purchase a child personal accident insurance policy for this insurance benefit alone.

Similarly, some of the personal accident insurance policies include inpatient insurance benefits. In these situations, I would prefer to rely on the health insurance coverage from MediShield Life and a private integrated shield plan instead. This is because the latter tends to provide more comprehensive insurance coverage as compared to a personal accident insurance policy. Hence, such insurance coverage (from a child personal accident insurance policy) is secondary to me.

Part 8: Child’s Personal Accident Insurance Policies that did not meet the criteria

In case you are curious, the following personal accident insurance policies did not fulfil my need for a child’s personal accident insurance policy. Generally, these personal insurance policies do not cover infectious diseases. As for the two personal accident insurance policies that cover Hand, Foot, and Mouth Disease, the child needs to be hospitalised. However, this is not the scope of insurance coverage that I’m looking out for.

- AIG’s Sapphire Enhanced Choices: The “Accident Medical Reimbursement” benefit does not include infectious diseases. As for its “Infectious Diseases Recovery Cover” (an optional add-on), Hand, Foot, and Mouth Disease is not one of the listed diseases.

- Allianz’s Accident Protect Plus: The “Medical & Surgical Expenses” benefit does not include infectious diseases. Instead, the insurer will provide a lump sum payout under its “Infectious Disease Benefits”.

- China Taiping’s Panda Safe: The “Medical Expenses” benefit does not include infectious diseases. Meanwhile, under its “SARS / Bird Flu / Dengue Fever / Hand Foot Mouth Disease” benefit, the insured needs to be hospitalised to claim this insurance benefit.

- EQ Insurance’s Personal Accident: The insurance policy explicitly states that it does not cover any diseases.

- Etiqa’s Solitaire Protect: The “Outpatient Medical Expenses” benefit does not include infectious diseases. Meanwhile, under its “Inpatient Medical Expenses”, the insured needs to be hospitalised to claim this insurance benefit.

- Singlife’s Personal Accident: The insurance policy explicitly states that it does not cover any diseases.

- Tokio Marine TM PA: The “Medical Reimbursement” benefit does not include infectious diseases.

Leave a Reply