Launched in 2021, CPF’s Matched Retirement Savings Scheme (MRSS) enables senior Singapore Citizens with lower retirement savings to build a stronger foundation for retirement. This scheme offers a dollar-for-dollar government matching grant for eligible cash top-ups made to the Retirement Account. In this article, we examine the mechanics of the MRSS, how it works, and how it fits into your retirement planning.

🎥 Prefer watching? Check out the video version of this post.

Table of Contents:

- What is the Matched Retirement Savings Scheme (MRSS)

- How MRSS Works

- Benefits

- Limitations

- Eligibility Criteria

- Practical Examples

- MRSS vs RSTU

- Who This is Suitable For

- Final Thoughts

- Changelog

One Minute Summary:

- What It Is: A government scheme that matches eligible cash top-ups to your CPF Special or Retirement Account dollar for dollar.

- Key Eligibility Criteria: You must be a Singapore Citizen aged 55 or above, or below age 55 with disability status verified with Ministry of Social and Family Development

- The Benefit: You can receive matching grants of up to $2,000 per year (Lifetime cap of $20,000).

- The Trade-Off: Cash top-ups that receive the matching grant are not eligible for tax relief.

- No Application Needed: Eligibility is automatically assessed annually. If you qualify, the CPF Board will notify you via email or post.

Part 1: What is the Matched Retirement Savings Scheme (MRSS)

The Matched Retirement Savings Scheme (MRSS) is a targeted government initiative designed to help Singaporeans meet the Basic Retirement Sum (BRS).

In practical terms, the government will match every dollar of eligible cash top-up you make to your Special or Retirement Account, up to the stipulated limits. The intent is straightforward – to provide structured support to those whose retirement savings may otherwise fall short of covering basic living needs.

However, the Matched Retirement Savings Scheme should not replace your comprehensive retirement planning. It serves as an additional tool to bolster savings already allocated to the Central Provident Fund (CPF) system.

Part 2: How MRSS Works

The process is designed to be frictionless and largely automated.

Part 2.1: Eligibility Assessment

At the beginning of each year, the CPF Board (CPFB) automatically assesses your eligibility. You do not need to apply manually. If you qualify, CPF Board will notify you via email or post. Alternatively, you may also check your eligibility via your Retirement Dashboard.

Part 2.2: Making The Cash Top-Up

Once you are confirmed as eligible, your family members or you may make cash top-ups to your Special or Retirement Account under the Retirement Sum Topping-Up Scheme (RSTU) mechanism.

To qualify for the matching grant:

- The top-ups must be made in cash (CPF transfers do not qualify)

- Top-ups must be made by 31 December of the assessment year

- Contributions can be a lump sum or multiple smaller amounts throughout the year

Part 2.3: Receiving the Matching Grant

The Government will credit the matching grant automatically to your Special or Retirement Account at the start of the following year. For example, cash top-ups made in 2026 will receive the matching grants in early 2027.

Part 2.4: Interest Accumulation

Your top-ups begin earning interest immediately upon being credited. Both your cash contribution and the eventual government grant earn the risk-free CPF interest rate of at least 4% per annum. Over time, this compounding effect significantly increases the balance available to support higher monthly payouts under CPF LIFE.

Part 3: Benefits

Part 3.1: Government Matching

Under MRSS, the Government matches every dollar of eligible cash top-up made to your Special or Retirement Account. This is subject to

- An annual cap of $2,000

- A lifetime cap of $20,000.

For example, if you top up $2,000 in 2026, the Government will credit another $2,000 to your Retirement Account in early 2027. Mathematically, this represents a 100% return on capital before interest is even factored in.

Part 3.2: High Risk-Free Interest

Savings in the Special or Retirement Account earn a base risk-free interest rate of 4% per annum. Additionally, CPF pays extra interest on the first $60,000 of your combined balances.

| Age | Base Interest (p.a.) | Additional Interest (p.a.) | Total Interest (p.a.) |

|---|---|---|---|

| Below 55 | 4% | 1% on the first $60k combined balances, capped at $20k for OA | Up to 5% |

| 55 and above | 4% | 2% on the first $30k, and 1% on the next $30k combined balances, capped at $20k for OA | Up to 6% |

This is among the highest risk-free returns in Singapore. When combined with the matching grant, the long-term accumulation is even more substantial.

Part 3.3: Higher Retirement Payouts

The primary purpose of the Special or Retirement Account is to fund a CPF LIFE plan. By boosting your Special or Retirement Account balance today, you will receive higher monthly payouts from CPF LIFE in time to come. This provides a stronger safety net against inflation and longevity risk.

Part 3.4: Flexibility in Contribution

CPF top-ups may be made at any time during the year, either as a lump sum or spread across multiple months. Both approaches qualify for matching. This is as long as the total eligible amount does not exceed the annual cap.

That said, contributing earlier may be advantageous. This is because CPF calculates the interest on a monthly basis. A January top-up earns interest for almost the full year, whereas a December top-up earns substantially less interest in that year. This difference compounds over time.

Part 4: Limitations

While the benefits are clear, it is important to understand the constraints.

Part 4.1: Top-Up Limits

Only the first $2,000 of cash top-ups each year is eligible for matching.

For example, if you top up $8,000:

- The first $2,000 receives the matching grant.

- The remaining $6,000 does not.

There is also a lifetime matching cap of $20,000. Once reached, you will not receive further matching grants.

Part 4.2: No Tax Relief on Matched Amounts

Since 1 January 2025, cash top-ups that attract the MRSS matching grant are not eligible for tax relief under the Retirement Sum Topping-Up Scheme (RSTU).

However, top-ups beyond the MRSS-matched amount may still qualify for tax relief under the prevailing RSTU rules.

For example, if you top up $8,000:

- The first $2,000 receives MRSS matching (no income tax relief)

- The remaining $6,000 may qualify for income tax relief).

This structure prevents claiming both matching grants and tax relief on the same contribution.

Part 4.3: Liquidity Lock-In

Cash top-ups to your Special or Retirement Account are irreversible. Once you top up, you cannot

- Withdraw the top-ups as a lump sum

- Use them for other CPF schemes, e.g. housing, education, insurance, investment

- Transfer them to loved ones

These funds are permanently committed to funding your CPF LIFE payouts. This restriction exists because top-ups enjoy higher interest and tax benefits. Allowing withdrawals would defeat the purpose of the Retirement Sum Topping-Up Scheme.

Before topping up, consider whether you

- Need liquidity for emergencies or near-term expenses

- Expect to require a lump sum in retirement

- Want to preserve funds for legacy planning

- Have sufficient cash savings outside CPF

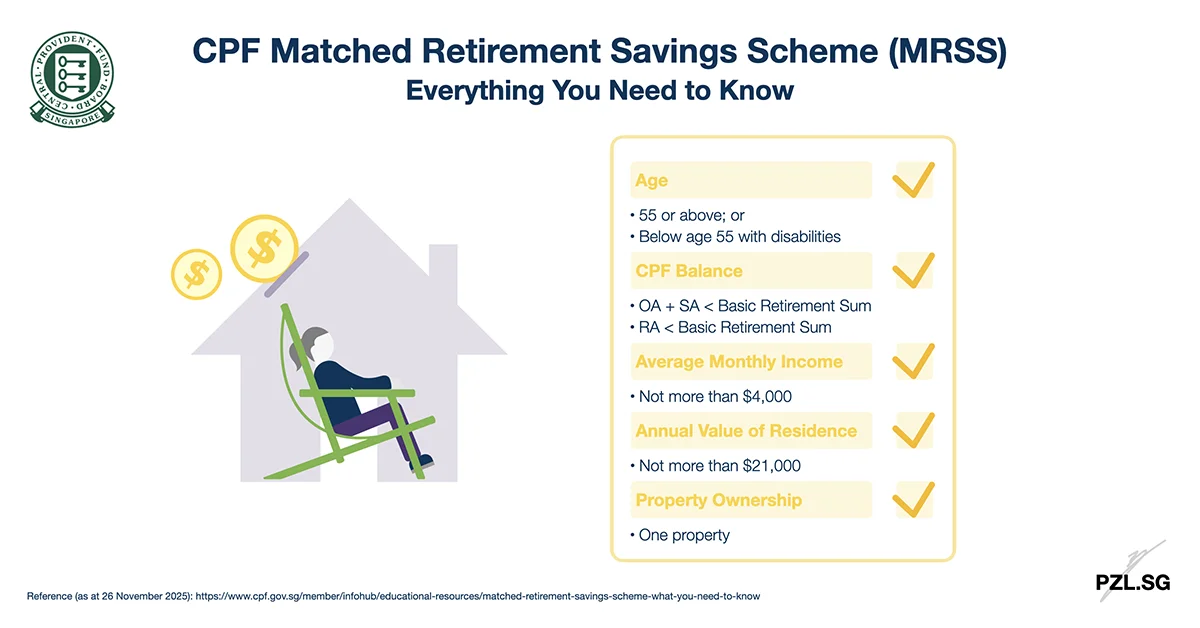

Part 5: Eligibility Criteria

To qualify for the MRSS, you must meet all the following criteria as of 31 December of the assessment year:

- Citizenship: Singapore Citizen

- Age: 55 or above, or below age 55 with disability status verified with Ministry of Social and Family Development

- Special or Retirement Account Balance: Less than $110,200 (prevailing Basic Retirement Sum in 2026)

- Income: Average monthly income of $4,000 or less

- Housing: Lives in a property with an Annual Value of $21,000 or less

- Property Ownership: Does not own more than one property

Part 6: Practical Examples

Let’s look at two scenarios to see how the math works in real life.

Part 6.1: Example 1

Profile of Member A:

- Singapore Citizen

- Age 60

- Retirement Account Balance: $84,000

- Average Monthly Income: $2,800

- Lives in a 4-room HDB flat (Annual Value is less than $21,000)

- Owns only 1 property

Member A (or his family members on his behalf) makes a cash top-up of $2,000 to his Retirement Account.

At the beginning of the following year,

- Government Matching Grant: The Government credits a matching grant of $2,000.

- Member B’s updated Retirement Account Balance: $88,000, before CPF interest.

- Tax Relief under the RSTU: First $2,000 contribution is not eligible for tax relief.

If Member A wishes to enjoy tax relief, he can top up an additional amount, say $3,000. In this case,

- The first $2,000 attracts MRSS matching (no tax relief).

- The additional $3,000 may qualify for tax relief under the RSTU rules.

Part 6.2: Example 2

Profile of Member B:

- Singapore Citizen

- Age 65

- Retirement Account Balance: $50,000

- Average Monthly Income: $2,000

- Lives in a 3-room HDB flat (Annual Value is less than $21,000)

- Owns only 1 property

Member B, or his family members, makes a monthly cash top-up of $200 to his Retirement Account for 12 months.

At the beginning of the following year,

- Government Matching Grant: The Government credits a matching grant of $2,000 (maximum).

- Member B’s updated Retirement Account Balance: $54,400, before CPF interest.

- Tax Relief under the RSTU: First $2,000 contribution is not eligible for tax relief. The remaining $400 contribution is eligible for tax relief under the RSTU.

Member B can perform additional cash top-ups if he wishes to enjoy even more tax relief under the RSTU.

Part 7: MRSS vs RSTU

The Matched Retirement Savings Scheme (MRSS) operates within the broader Retirement Sum Topping-Up Scheme (RSTU) framework. In both cases, you are making a cash top-up to your Special or Retirement Account. However, the objectives differ. Understanding these differences helps avoid confusion, especially around tax relief and contribution limits.

Part 7.1: Key Differences between MRSS and RSTU

| Feature | MRSS | RSTU |

|---|---|---|

| Primary Benefit | Government matching grant | Income tax relief |

| Who Provides the Benefit | Government | IRAS |

| Annual Cap | $2,000 | Up to the current year’s Enhanced Retirement Sum |

| Lifetime Cap | $20,000 | No lifetime cap, but annual ERS limit applies |

| Tax Relief | No | Yes, subject to RSTU rules |

| Eligibility Criteria | Strict | Broad |

| Top-Up Method | Cash only | Cash or CPF Transfer |

Part 7.2: How MRSS and RSTU Work Together

If you qualify for MRSS and make a cash top-up, the first $2,000 of eligible top-up falls under the MRSS. This portion

- Receives government matching, and

- Does not qualify for tax relief.

Any top-up beyond $2,000 falls under the standard RSTU. This portion

- Does not receive government matching, and

- May qualify for tax relief, subject to the usual RSTU rules.

MMSS and the standard MediSave-Up are complementary, but the same dollar cannot receive both benefits.

Part 7.3: When MRSS matters more

Generally, MRSS is more relevant if:

- You meet the strict eligibility criteria

- Your priority is to boost your retirement income

- You are comfortable with locking in your cash savings

If you qualify for MRSS, the matching grant will likely outweigh the value of tax relief. For the sake of this example, assume you are in the 24% tax bracket.

- $2,000 tax relief saves you $480 in taxes

- $2,000 MRSS matching adds $2,000 directly to your Retirement Account balance

Therefore, consider maximising the MRSS benefit first before making additional top-ups for tax relief purposes.

Part 7.4: When the regular RSTU matters more

Conversely, the regular RSTU is more relevant if you:

- Do not qualify for MRSS

- Are still accumulating CPF towards the ERS

- Place greater value on immediate tax relief

- Wish to also use CPF transfers

RSTU remains the primary CPF top-up mechanism for higher-income earners or those who have already exhausted the MRSS benefits.

Part 8: Who This is Suitable For

The Matched Retirement Savings Scheme is suitable for:

- Eligible individuals who have not met the Basic Retirement Sum yet

- Family members supporting parents or loved ones with modest retirement savings

- Part-time or gig workers or homemakers with limited CPF savings

However, MRSS is less suitable for those who

- Require short-term liquidity

- Prioritise tax optimisation over long-term retirement income

Part 9: Final Thoughts

The Matched Retirement Savings Scheme (MRSS) addresses a specific need: to encourage Singaporeans with lower retirement savings to build a stronger retirement income stream through CPF LIFE. This is done through structured government matching.

Topping up your Special or Retirement Account remains a risk-free and predictable way to boost your retirement savings. Together with matching grants from the government, it enables you to save more with less capital.

However, this represents a long-term commitment. You sacrifice liquidity in exchange for a risk-free 100% return and a permanently higher baseline for your lifelong income stream from CPF LIFE.

If you or your parents meet the MRSS criteria, not using this scheme means forgoing government support that could significantly boost retirement savings.

If you do not qualify, or if you have already maximised the MRSS benefits, you can continue to top up your Special or Retirement Account through the Retirement Sum Topping-Up Scheme.

Next Step: Log in to the CPF Board website using Singpass to check your eligibility status. If eligible, plan your cash flow to make the $2,000 top-up early in the year to maximise compounding interest!

Part 10: Changelog

From 1 January 2026:

- The scheme expands to include eligible persons with disabilities of all ages. For those who are under 55, top-ups would be made to the Special Account.

- For those below 55, your OA + SA savings must be less than $110,200 to qualify.

- For those 55 and above, your RA savings must be less than $110,200 to qualify.

From 1 January 2025:

- Annual matching cap increased from $600 to $2,000, with a $20,000 lifetime cap.

- Removal of the previous age cap of 70.

- Cash top-ups that attract MRSS grants no longer qualify for tax relief.

Reference: Matched Retirement Savings Scheme (MRSS) – what you need to know

Leave a Reply