Understanding credit card rewards can feel like studying for a university examination. There are so many options and an overwhelming number of terms and conditions to comprehend. However, once you understand how they work, credit card rewards are essentially free benefits that you should take advantage of. With this in mind, let’s learn how credit card rewards work in Singapore and how you can utilise them to your advantage.

Table of Contents:

- What are Credit Card Rewards

- Why Credit Card Rewards Matter

- Cashback Explained

- Miles Explained

- Reward Points Explained

- Building Your Own Credit Card Deck

Disclosure: This post on Credit Card Rewards contains referral links. Hence, I may receive some money for coffee when you use my referral link for the credit card application. But no, there is no additional cost to you. In fact, you will receive some cash or cash equivalent incentives too! In any case, I will only recommend products or services that meet my needs and expectations.

One Minute Summary:

- If you prefer simplicity, cashback cards are the most straightforward – spend, earn, and let the cashback offset your statement automatically.

- If you enjoy travelling, miles cards can stretch your dollar further when you redeem them wisely.

- If you want flexibility, reward points cards give you the best of both worlds – spend first, decide whether to convert them into cash rebate or miles later.

- Basic credit cards are best if you want a single hassle-free option.

- Advanced credit cards are best if you want to maximise the credit card rewards for your spending.

Part 1: What are Credit Card Rewards

Credit card rewards are incentives that banks or financial institutions offer you for using their credit cards. There are three types of rewards:

- Cashback: You earn a predefined percentage of cash back from your spending. Cashback is typically used to offset your upcoming credit card statement.

- Miles: You earn frequent-flyer miles from your spending. Miles can be used for flights, upgrades or even partner redemptions.

- Reward Points: You earn points from your spending. Reward points can be converted into cashback, miles or partner rewards.

Part 2: Why Credit Card Rewards Matter

Using a credit card enables you to stretch your payment terms by up to 25 days. This helps you manage your cash flow better. By earning credit card rewards, you maximise the value of your spending by not leaving “free money” on the table.

Let’s take the purchase of an item that costs $100 as an example. If you pay in cash, your net cost is $100. However, if you use a credit card that offers 5% cashback, your net cost becomes $95. Over time, these savings will accumulate into a larger amount.

In the next few sections, I will share how different types of credit card rewards work in Singapore.

Part 3: Cashback Explained

Cashback is probably the most straightforward type of credit card reward. After spending on your credit card, you will receive a cash rebate. Generally, this cashback will be used to offset the next month’s credit card statement.

Part 3.1: Basic Cashback Credit Card

A basic cashback credit card tends to offer between 1.5% and 1.7% cashback on your spending. These cards usually do not impose any minimum spending requirement or earning cap. As a result, many of us would find such cashback credit cards to be a hassle-free option.

Examples: American Express® True Cashback, Citi Cash Back+, OCBC Infinity Cashback, Standard Chartered Simply Cash, UOB Absolute Cashback

Let’s take the case of the UOB Absolute Cashback card. It boasts to offer the highest limitless cashback rate at 1.7%. There are no spend exclusions (though some categories earn a mere 0.3% cashback). If you use this card to pay for an item that costs $1,000, UOB will credit $17 into your next statement. Thereafter, this amount will automatically offset that statement.

Formula: $1,000 x 1.7% = $17

Part 3.2: Advanced Cashback Credit Card

Some credit cards promise a higher rate of cashback, e.g. up to 10% cashback. However, you must fulfil certain terms and conditions to unlock the higher earning rate.

Examples: Citi Cash Back, HSBC Live+, OCBC 365, Standard Chartered Smart, UOB One

Let’s take the case of the OCBC 365 credit card. By spending a minimum of $800 in a calendar month, you will enjoy the following cashback rates:

- 6% on petrol,

- 5% on dining,

- 3% on groceries,

- 3% on land transport,

- 3% at Watsons,

- 3% on streaming services,

- 3% for electric vehicle charging, and

- 3% on utilities.

If you spend less than $800 in a calendar month, you will earn a flat 0.25% cashback instead.

Part 3.3: When You will receive the Cashback

Most cashback credit cards issue the cashback into your next statement. As a result, the only way to utilise it is to spend it after your current billing cycle. Despite this common practice, American Express® True Cashback credits the cashback within the same statement month. This allows you to use the cashback to offset your current bill.

Part 4: Miles Explained

Miles credit cards are especially attractive to frequent flyers. After spending on the credit card, you will receive bank miles. Once you have accumulated sufficient miles, you can transfer them to your preferred airline loyalty programme as airline miles. Thereafter, you may use these airline miles to redeem air ticket or upgrade your seat.

Part 4.1: Basic Miles Credit Card

In general, a basic miles credit card will offer between 1.2 and 1.4 miles per dollar for your spending. Similar to basic cashback credit cards, they usually do not have any minimum spending requirements or earning caps. As a result, you will likely find such miles credit cards to be a hassle-free option as well.

Examples: Citi PremierMiles, HSBC TravelOne, OCBC 90N Mastercard, Standard Chartered Journey, UOB PRIV Miles Mastercard

Let’s take the case of the Citi PremierMiles card. It offers 1.2 Citi Miles for every dollar local spent. If you use this card to pay for an item that costs S$1,000, Citibank will credit 1,200 Citi Miles into your account.

Part 4.2: Advanced Miles Credit Card

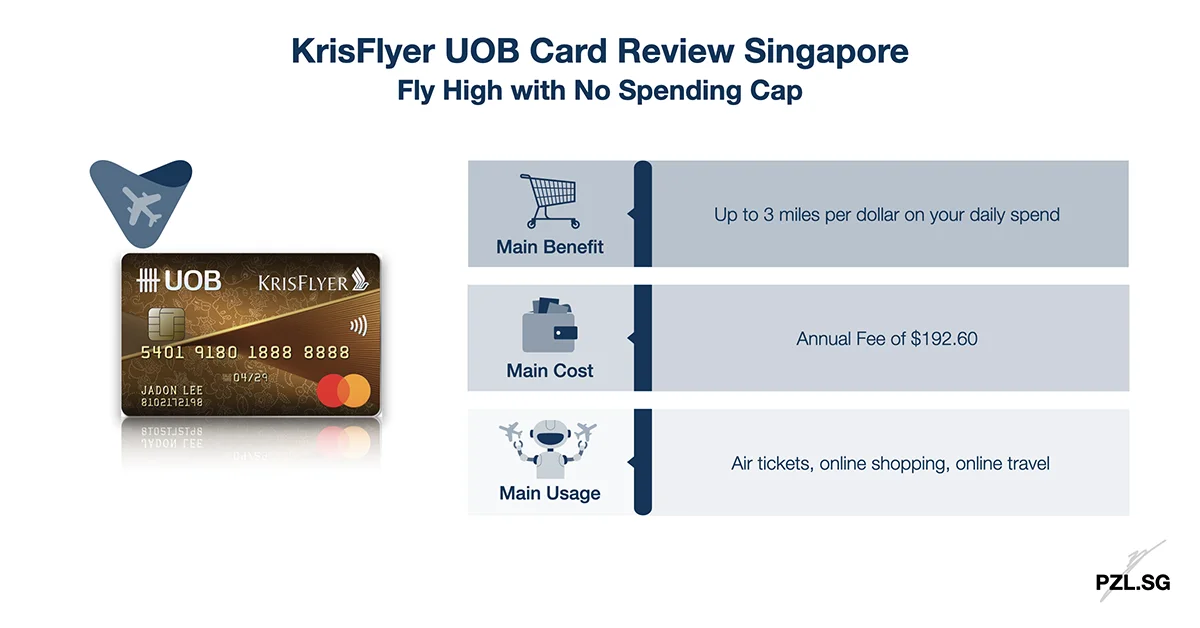

Some credit cards offer a higher rate, e.g. up to 3 miles per dollar spent. However, you must fulfil certain terms and conditions to unlock the higher miles earning rate.

Let’s take the case of the KrisFlyer UOB card. You can earn 3 KrisFlyer miles per dollar spend on Singapore Airlines, Scoot, KrisShop, Kris+ and Pelago purchases. Moreover, by spending at least $1,000 on Singapore Airlines Group related transactions within your card membership year, you will earn 2.4 miles per dollar spent on:

- Dining,

- Online Shopping,

- Online Travel, and

- Transport.

Part 4.3: When can You convert the Miles?

Most banks require you to accumulate at least 10,000 miles before converting. They also charge an administrative fee of $27.25 (inclusive of 9% GST) for each conversion. After the conversion, you can use the airline miles to redeem flights or seat upgrades via your airline loyalty programme.

Part 5: Reward Points Explained

If you cannot decide between cashback or miles, a reward points credit card may solve the problem. After spending on your credit card, you earn reward points. Once you accumulate sufficient reward points, you can

- Use the points to offset your spending,

- Convert the points into airline miles, or

- Exchange the points for gifts and vouchers.

Part 5.1: Reward Points System

Most reward points credit cards follow a two-tier system:

- The reward points credit card will give 1X reward point for all the eligible transactions.

- Paying selected merchant categories will trigger an additional 9X bonus points.

Generally, accumulating reward points becomes worthwhile only if you consistently earn 10X points. This is because it enables you to accumulate points much faster.

Part 5.2: Standard Reward Points Credit Card

Examples: Citi Rewards, HSBC Revolution, OCBC Rewards, UOB Preferred Platinum Visa

Let’s take the case of the Citi Rewards card. It offers 10X Points for online purchases and in-store shopping purchases. If you use this card to pay $1,000 for an item online, Citibank will credit 10,000 Points into your account.

Part 5.3: Converting the Reward Points

After accumulating sufficient reward points, you can use them as cash rebate or convert them into airline miles. Different banks may adopt different conversion rates. To illustrate, this is the conversion rate for Citi Rewards:

- Cashback: Convert 4,400 Points for a $10 cash rebate (equivalent to 2.27% cash rebate).

- Miles: Convert 25,000 Points into 10,000 airline miles (equivalent to 4 miles per dollar).

Part 6: Building Your Own Credit Card Deck

Credit card rewards allow you to get more out of your daily spending without changing your lifestyle. In fact, with payment terms stretching up to 25 days, your cash flow will definitely thank you later.

If you prefer simplicity, cashback cards are the most straightforward – spend, earn, and let the cashback offset your statement automatically. There is no fuss over any conversions.

If you enjoy travelling, miles cards can stretch your dollar further. When redeemed wisely, the value of a mile often outweighs what you gain from a basic cashback credit card.

If you want flexibility, reward points cards give you the best of both worlds – spend first, decide later. You can convert the reward points into either cash rebate or miles depending on your needs.

Want to learn how I build my own credit card deck? Check out: Which Credit Cards do I have Singapore: 2026 Edition

First Published: 15 May 2021

Last Updated: 16 November 2025

Leave a Reply