Income Insurance Care Secure Pro is a long-term care insurance policy that provides you with a monthly cash payout in the event of a disability. According to Income Insurance, it provides comprehensive coverage across different stages of disability, from mild to severe. With this in mind, let’s learn about Income Insurance Care Secure Pro (“the Plan”) in this post.

Table of Contents:

- What is Income Insurance Care Secure Pro

- Insurance Coverage (Benefits)

- Cash Value

- Insurance Premium (Cost)

- Limitations and Risks

- Claims

- Insurance Nomination

- Eligibility

- Target Audience

- Trivial

One Minute Summary:

- Type of Plan: Non-Participating

- Type of Coverage: Long-term care

- Main Benefits: Disability Benefit, Death Benefit

- Coverage Amount: Between $200 to $5,000

- Coverage Period: Lifetime

- Cash Value: Nil

- Premium Payment Period: Till age 67 or 99 last birthday (ALB)

Part 1: What is Income Insurance Care Secure Pro

Income Insurance’s Care Secure Pro is a non-participating long-term care insurance policy. This means you will not participate or share in the profits of the insurer’s participating fund. Instead, the insurance premium is used to pay for the insurance charges and the product’s distribution cost.

Part 2: Insurance Coverage (Benefits)

Before we begin, here are three terms that we will use throughout this post:

- Mild disability or mildly disabled: Inability to perform one of the Activities of Daily Living

- Moderate disability or moderately disabled: Inability to perform two of the Activities of Daily Living

- Severe disability or severely disabled: Inability to perform three or more Activities of Daily Living

In all three cases, this is even with the aid of special equipment and always requires the physical assistance of another person throughout the entire activity.

Part 2.1: Main Benefits

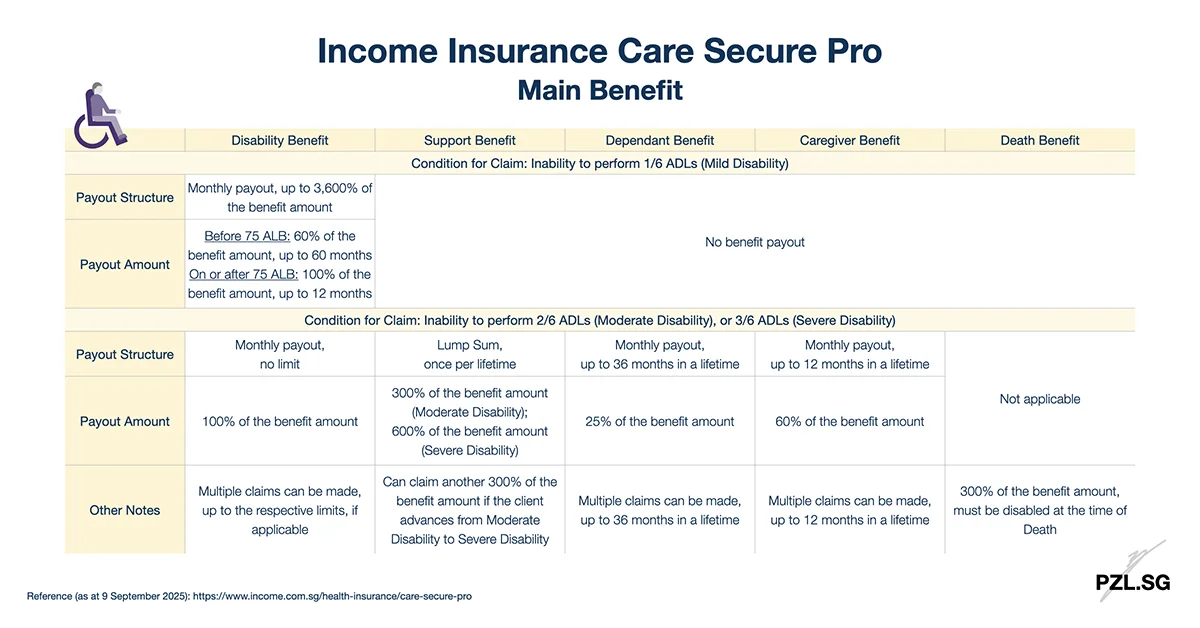

Income Insurance’s Care Secure Pro provides five main benefits, and I have summarised these benefits in the following table:

For the Disability Benefit, you are allowed to make multiple claims, up to the lifetime limit (if applicable). To illustrate, let’s assume that you are age 62 and unable to perform one of the Activities of Daily Living. After a claim period of 24 months, you recovered from the mild disability. Later on, if you become mildly disabled again, you may claim up to 36 months of the monthly Disability Benefit.

For the Support Benefit, you can only claim under the moderate disability status once. If you become severely disabled later, you can make another claim for 300% of the Disability Benefit.

For the Dependant Benefit, dependants refer to your:

- Child (or children);

- Spouse;

- Parents; and

- Parents-in-law.

For the child, it refers to your biological child or stepchild, or legally adopted child, who has not reached the age of 21 years on the claim date. Let’s take the case where Care Secure Pro has started paying the Dependant Benefit. If the child is no longer considered a child (e.g., reached the age of 21), the Plan will continue to pay this benefit until your death or you recover from the disability. The payment will then end.

For the Death benefit, the date of death must be after the policy’s deferment period, and you must be disabled at the time of your death.

Part 2.2: Coverage Amount

You have the option to select a benefit amount that ranges from $200 to $5,000. In detail, you may make a $10 adjustment each time.

Income Insurance allows you to increase the disability benefit if the Plan is in force for less than one year. On the other hand, you may decrease the disability benefit anytime (though you won’t receive a pro-rated refund of the difference in premiums). When revising,

- The revised premium will be based on the entry age at policy inception;

- You will pay the revised premium from the next premium due date; and

- The revised benefit will be effective from the next premium due date.

Part 2.3: Coverage Period

Care Secure Pro is a yearly renewable insurance policy that covers you for life. While you are alive, Income Insurance guarantees that you will be able to renew this long-term care insurance policy every year. This is so long as you pay the insurance premium on time.

That being said, Care Secure Pro will terminate upon certain events, e.g. death of the life insured. Given that the list of events is relatively long, I will encourage you to read the Product Summary or the Insurance Policy Contract for the full list.

Part 3: Cash Value

As a non-participating health insurance policy, Care Secure Pro does not have any cash value. Accordingly, you won’t be able to terminate this Plan for a surrender value. Instead, you will receive a payout from the insurance policy only when a covered event is triggered.

Despite that, Care Secure Pro has a Paid-Up policy value feature. Accordingly, you can enjoy a reduced disability benefit if

- Your Plan has been in force for more than ten years; or

- You have reached 61 age last birthday,

whichever is later.

Part 4: Insurance Premium (Cost)

Part 4.1: Premium Determinants

Generally, the insurance premium is determined based on your entry age and gender. Additionally, it also depends on the coverage amount that you have chosen.

Part 4.2: Non-Guaranteed Level Premium Rates

Although the insurance premium rate is level, it is not guaranteed to remain the same throughout the entire policy period. In general, a level insurance premium means you will pay the same amount of money to the insurer every year. Despite that, Income Insurance reserves the right to revise the insurance premium rate for each age during the policy anniversary (by serving you a notice of revision at least 30 days in advance). Under those circumstances, the insurance premium rate will be adjusted. Hence, in this case, we say that the insurance premium rate is not guaranteed.

You are allowed to use up to $600 of savings in your CPF MediSave Account to pay for the insurance premium. This limit is based on per insured per calendar year for all the supplements.

Part 4.3: Premium Paying Period

Depending on your entry age, you may choose to pay premiums up to age 67 or 99 last birthday (ALB).

Part 4.4: Premium Waiver

If you are disabled on the date when the insurance premium is due, you do not need to pay the premium. However, if you are no longer disabled, then you will need to resume the premium payment.

Part 4.5: Distribution Cost

In general, distribution cost refers to the charges that arise from the marketing and sale of a product or service. To sum up, the total distribution cost for Care Secure Pro spreads across the first three policy years. In detail, the distribution cost for the respective three years is 108.9%, 41.1%, and 5.2%.

Part 5: Limitations and Risks

Part 5.1: Waiting Period

There is a 90-day Waiting Period from the cover start date or reinstatement date, whichever is later. During the Waiting Period, Income Insurance will not pay for any claims except claims resulting from an accident.

Part 5.2: Deferment Period

Before Income Insurance makes the first benefit payment, there is a 90-day deferment period from the claim date. The claim date is the date on which you undergo the disability assessment and an approved assessor under the Relevant Act has certified your disability.

Let’s take the case when you have recovered from a disability. If you become disabled again from the same cause within 180 days, Income Insurance will not enforce the deferment period for the new claim.

On the other hand, let’s consider the case when you suffer a disability that arises from the same cause after the 180 days, or suffer a disability from a different cause. In this case, Income Insurance will apply the 90-day deferment period for the new claim.

Part 5.3: Free-Look Period

Income Insurance Care Secure Pro comes with a 60-day Free-Look Period. In detail, the Free-Look Period begins 7 days after Income Insurance sends the insurance policy contract out to you (be it by post or electronically). Accordingly, if you write to Income Insurance to cancel your insurance policy during this period, Income Insurance will refund the insurance premium that you have paid. It is important to realise that the refund will be made without interest. Additionally, Income Insurance will also deduct any expenses that they have incurred in assessing the risk under the policy and in issuing the insurance policy.

Part 5.4: Grace Period

Income Insurance allows a 75-day Grace Period for you to pay the insurance premium. During the grace period, your Care Secure Pro policy will remain in force. After the grace period, Income Insurance will check if your Plan has accumulated sufficient paid-up policy value. If so, your Plan will become paid-up. Otherwise, your Care Secure Pro policy will end immediately.

Part 5.5: Exclusion

There are certain conditions under whereby Care Secure Pro will not issue a payout for the policy benefits. Given that the list of exclusions is relatively long, I will encourage you to read the Product Summary or the Insurance Policy Contract for the full list of exclusions.

Part 6: Claims

There are two documents that you need to submit for the claim:

- A completed claim form; and

- A certification by an approved assessor under the Relevant Act.

For the first disability assessment, you will need to arrange and pay for the assessment. Upon the admission of the claim, Income Insurance will reimburse you for the disability assessment fee.

After the deferment period, if you are disabled on the date when the premium is due, Income Insurance will waive the premiums payable. Thereafter, you will resume the premium payment again after you are no longer disabled.

Part 7: Insurance Nomination

Based on the current Insurance Nomination Law, you are allowed to make a revocable nomination. On the other hand, you are not allowed to make a trust nomination.

Part 8: Eligibility

To apply for Income Insurance Care Secure Pro, you need to fulfil the following three criteria:

- Either a Singapore Citizen or Singapore Permanent Resident; and

- Age between 30 and 47 on last birthday (for premium term up to 67 ALB), or between 30 and 69 on last birthday (for premium term up to 99 ALB); with

- An existing CareShield Life or Basic ElderShield.

Part 9: Target Audience

According to the Ministry of Health in 2018, 1 in 2 Singaporeans who are healthy at age 65 could become severely disabled at some point in their lifetime and require long-term care support. Moreover, there is also an uncertainty about the duration a person remains severely disabled. Although the median duration of disability is four years, 30% of people could remain severely disabled for 10 years or more.

With this in mind, Care Secure Pro may be suitable for you if you want an additional payout above your existing Basic ElderShield or CareShield Life scheme. Moreover, Care Secure Pro adopts a broader claims definition as compared to CareShield Life; the latter requires you to be severely disabled.

Part 10: Trivial

Income Insurance Care Secure Pro was launched on 9 September 2025. On its launch, Income Insurance withdrew PrimeShield and Care Secure. Despite that, if you have an existing PrimeShield or Care Secure, your renewals will not be impacted.

Disclaimer:

This post contains a summary of Income Insurance Care Secure Pro, and it is for informational purposes only. Accordingly, you are advised to read the respective product summary for the full disclaimer and/or seek professional advice. Next, the views and opinions expressed in this publication are those of the author. Therefore, they do not reflect the official policy or position of any other agency, organisation, employer, or company. Assumptions made in the analysis are not reflective of the position of any other agency, organisation, employer, or company other than the author. This advertisement has not been reviewed by the Monetary Authority of Singapore. Information is correct as of 9 September 2025. Protected up to specified limits by SDIC.

Leave a Reply