Singlife Dementia Cover boasts to be the first-in-market long-term care protection plan that provides up to $170,000 in payouts for cognitive decline and mental health conditions. Given that recent hype on mental health protection, I decided to conduct an in-depth analysis for this plan. Accordingly, here is my analysis of Singlife Dementia Cover (“the Plan”) and whether you should purchase it right away (no, you probably should not).

Table of Contents:

- What is Singlife Dementia Cover

- Potential Cost

- Insurance Coverage (Benefit)

- Case Study

- My Observations (Non-Exhaustive)

- Cost to Benefit Ratio

- Analysis 1

- Analysis 2

- My Thoughts

- Final Thoughts

One Minute Summary:

- To sum up, Singlife Dementia Cover will cost between about $60 to $4.6k annually. In detail, the exact insurance premium rate will depend on your entry age, gender, and the selected benefit amount.

- For this purpose, you may select a benefit amount that is between $200 and $2,000. To point out, the insurance payout amount will be 5 times the benefit amount, i.e. between $1,000 to $10,000. Depending on the claim benefit, this payout amount will be made either annually or as a single lump sum.

- Overall, the Cost-to-Benefit Ratio is between 0.0050 to 15.6579.

- Generally, there are other types of insurance policies that you should consider first. To clarify, this is before getting Singlife Dementia Cover.

Part 1: What is Singlife Dementia Cover

Basically, Singlife Dementia Cover is a long-term care insurance policy that provides you with a payout in the event of a mental disability. According to Singlife, this is a first-in-market long-term care protection plan that provides up to $170,000 in payouts for cognitive decline and mental health conditions. Moreover, Singlife Dementia Cover includes a lump-sum payout for dementia-related depressive or anxiety disorder and accidental burns or fractures. If you wish to learn more about Singlife Dementia Cover, then I will encourage you to check out this post – Singlife Dementia Cover Singapore: Get Insured for Dementia and Mental Health Conditions.

Part 2: Potential Cost

By and large, the cost of insurance depends on your entry age and gender. Additionally, it also depends on the benefit amount that you have chosen during the application phase. In general, the premium will range between about $60 to $4.6k annually.

Part 3: Insurance Coverage (Benefit)

In truth, I found the way Singlife designed the benefit amount and the actual insurance payout amount to be confusing. To explain, the benefit amount is a figure that you select at the point of submitting the insurance application. For this purpose, you may select a benefit amount that is between $200 to $2,000, adjusting by $100 each time.

On the other hand, the actual insurance claim payout works out to be five times the benefit amount. In detail, this claim payout is made either in a single lump sum or as an annual payout (over the stipulated period). Given that Singlife uses a fixed multiplier (of five times) for all its claim benefits, I found no meaning in using the term “Benefit Amount”. Instead, it is far more straightforward to introduce the insurance benefit as a Sum Insured of between $1,000 to $10,000. In this situation, it saves us from having to perform any unnecessary Mathematical calculations. Furthermore, it eliminates the use of redundant jargon by adopting a more universal language used in an insurance policy. For the most part, I’m confident that most of us will be more familiar with the term “Sum Insured” – referring to the actual insurance claim payout that you receive.

Part 4: Case Study

In order to understand how Singlife Dementia Cover works, let’s go through a series of case studies together.

Part 5: My Observations (Non-Exhaustive)

Based on the eight case studies that you have seen in the earlier section, here are some of my observations:

Part 5.1: Insurance Premium

Generally, the cost of insurance tends to be cheaper for a male life insured. This is as compared to a female life insured for the same benefit amount. Accordingly, this seems to suggest that females have a higher risk of being diagnosed with a mental health condition.

Not surprisingly, the higher the benefit amount, the higher the cost of the insurance premium. In like manner, the older the life insured, the higher the cost of insurance premium. Consequently, this also seems to suggest that the older you get, the higher the risk of being diagnosed with a mental health condition.

As a matter of fact, there isn’t much reason to attempt to save on the insurance premium by purchasing Singlife Dementia Cover at a later time. This is because when you are older, you will pay a higher insurance premium rate. In time to come, the higher cost will outweigh the initial savings. To illustrate, for a benefit amount of $200, the total premium outlay for a 31-year-old male life insured is $4,046.68. By comparison, the total premium outlay for a 65-year-old male life insured is $14,139.24.

When you compare between the benefit amount of $200 and $2,000, the cost difference is about 10 times as well (with some minor rounding differences). To this end, this suggests that there is no marginal difference in the financial risk to the insurer (other than the higher benefit amount itself).

Part 5.2: Insurance Coverage

As the name of the plan suggests, Singlife Dementia Cover focuses on providing insurance coverage for mental health conditions, particularly for Dementia. Consequently, to receive the most payout, you will need to be diagnosed with Dementia. In detail, this will have to be done sequentially, i.e. from Early or Intermediate Dementia, and then to Late Dementia.

Moreover, it is important to realise that Singlife pays the Cognitive Care Benefit and Mental Care Benefit over a 10-year and a 5-year period respectively. As a result, to continue to receive the insurance claim payout, you will need to continue to meet the insurance policy’s claim condition. To illustrate, for Cognitive Care Benefit, if you recover from Late Dementia after two years, then Singlife will stop paying the rest of the Cognitive Care Benefit out to you.

Part 6: Cost to Benefit Ratio

Basically, the Cost to Benefit Ratio measures your cost outlay against the claim benefit that you (may) receive from the insurance policy. Generally, a lower ratio suggests that you have received a higher insurance claim benefit as compared to the insurance premium that you have paid. On the contrary, a higher ratio suggests that you have paid a higher insurance premium as compared to the insurance claim benefit that you have received.

On the whole, Singlife Dementia Cover can provide an insurance payout in various ways. For example, you could claim for both Mental Care Benefit and Emotional Resilience Benefit only. Under those circumstances, you can receive a maximum insurance payout of $60,000 (based on a benefit amount of $2,000). By comparison, in another example, you may claim for just two years of Mental Care Benefit and Emotional Resilience Benefit. In this situation, you will receive an insurance claim payout of $30,000 (based on a benefit amount of $2,000).

Given that large number of combinations and permutations, I will focus my analysis on two scenarios. Firstly, we will analyse the Plan based on the cheapest rate of insurance premium; i.e. for a 31-year-old male life insured who chooses a benefit amount of $200. Secondly, we will analyse the Plan based on the most expensive rate of insurance premium; i.e. for a 65-year-old female life insured who chooses a benefit amount of $2,000. In both cases, we will look at the Cost-to-Benefit Ratio when the Plan made a minimum claim payout, and the case when the Plan made the maximum claim payout. At the same time, we will also look at the Cost-to-Benefit Ratio for the highest insurance claim payout within the shortest time period.

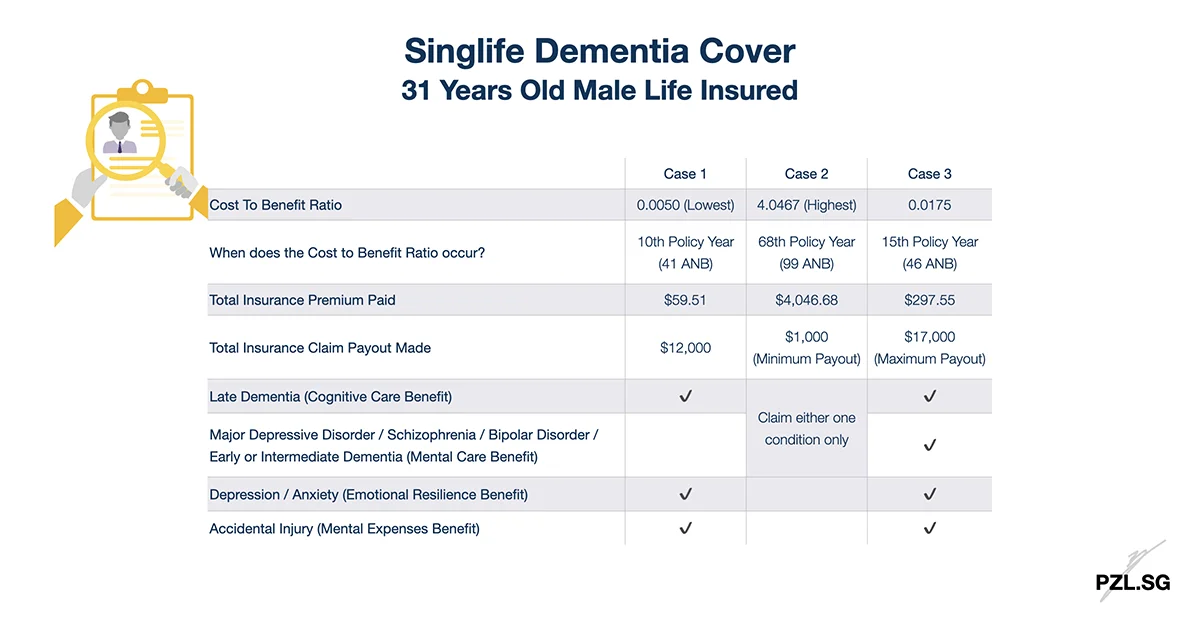

Part 7: Analysis 1 – 31 Years Old Male Life Insured, Benefit Amount of $200

To begin with, let’s study the case of a 31 years old male life insured who chooses a benefit amount of $200. In this case, the annual insurance premium is $59.51 and he will pay this insurance premium rate over the next 67 years. Summing up, the total insurance premium payable is $4,046.68 and the Cost to Benefit Ratio is between 0.0050 to 4.0467.

Part 7.1: Lowest Cost to Benefit Ratio

By and large, the lowest Cost to Benefit Ratio of 0.0050 will occur in the 10th policy year. In detail,

- Singlife needs to admit a claim under the Cognitive Care Benefit during the first policy year (after the 90-day Waiting Period).

- Upon the admission of a claim for the Cognitive Care Benefit, Singlife will waive the payment of insurance premium (so long as you continue to have Late Dementia).

- For this purpose, you will need to continue to have Late Dementia during the first 10 policy years.

- Additionally, you will also claim both the Emotional Resilience Benefit and the Mental Expenses Benefit.

To sum up, you have paid a total insurance premium of $59.51 and received an insurance claim payout of $12k. To put it another way, you paid the least amount of insurance premium and have received the highest insurance claim payout.

Part 7.2: Highest Cost to Benefit Ratio

On the other hand, a ratio of 4.0467 is the “next to nothing” scenario. In detail, this occurs when Singlife admits a claim for either the Cognitive Care Benefit or the Mental Care Benefit just before your 99th age next birthday. Under those circumstances, you overpaid your insurance policy by 4 times.

Part 7.3: Cost-to-Benefit Ratio for the Highest Payout (Shortest Period)

As a matter of fact, if you wish to receive the highest payout from Singlife Dementia Cover, your claims will need to follow a specific order. To begin with, Singlife will need to admit a claim under the Mental Care Benefit for 5 years. After Singlife has paid out the full benefit for the Mental Care Benefit, it will need to admit a claim for the Cognitive Care Benefit. During either period, Singlife will also admit a claim for both the Emotional Resilience Benefit and the Mental Expenses Benefit.

Summing up, you would have paid a total insurance premium of $297.55 and received an insurance claim payout of $17k. To this end, the Cost-to-Benefit Ratio is 0.0175.

Part 7.4: Retaining the Financial Risk

Next, let’s consider the case when you choose to retain the financial risk of (up to) $17k on your own. For this purpose, we shall invest $59.51 annually into a financial instrument that generates an effective yield of 4% per annum. To point out, I’m using an effective yield of 4% per annum as an arbitrary figure only. As a matter of fact, your planning return may be different from mine. This is because we may portray different risk appetite and investment horizon, amongst the other factors. With this in mind, the following calculation is merely to showcase my thought process. Thereafter, you should adjust the figures to suit your own unique needs.

Through investing, you will accumulate $1,029.04 by 43 years old; and this amount is similar to Singlife Dementia Cover’s minimum claim payout. And by the time you reach 65 years old, you will accumulate $4,558.37. To sum up, you will accumulate $17,494.06 when you reach 94 years old; and this amount is similar to the Plan’s maximum claim payout.

Meanwhile, let’s assume that you have a higher budget and can invest $243.36 annually over the next 34 years. Based on the same effective yield of 4% per annum, you will accumulate $17k by the time you reach 65 years old. As a matter of fact, studies show that dementia is more common among older adults over the age of 65. Consequently, you may be better off retaining the financial risk on your own in this case. In fact, if you continue to stay healthy, you can use this accumulated savings for other life purposes instead. Despite that, if you are concerned about developing a mental health condition before age 65, then you may still wish to consider getting insurance cover.

Part 8: Analysis 2 – 65 Years Old Female Life Insured, Benefit Amount of $2,000

Secondly, let’s study the case of a 65-year-old female life insured who chooses a benefit amount of $2,000. In this case, the annual insurance premium is $4,605.25 and she will pay this insurance premium rate over the next 33 years. Summing up, the total insurance premium payable is $156,578.50 and the Cost to Benefit Ratio is between 0.0384 to 15.6579.

Part 8.1: Lowest Cost to Benefit Ratio

Similar to Analysis 1 in Part 7, the lowest Cost-to-Benefit Ratio of 0.0384 will occur on the 10th policy year. In detail,

- Singlife needs to admit a claim under the Cognitive Care Benefit during the first policy year (after the 90-day Waiting Period).

- Upon the admission of a claim for the Cognitive Care Benefit, Singlife will waive the payment of insurance premium (so long as you continue to have Late Dementia).

- For this purpose, you will need to continue to have Late Dementia during the first 10 policy years.

- Additionally, you will also claim both the Emotional Resilience Benefit and the Mental Expenses Benefit.

To sum up, you have paid a total insurance premium of $4,605.25 and received an insurance claim payout of $120k.

Part 8.2: Highest Cost to Benefit Ratio

On the other hand, a ratio of 15.6579 is the “next to nothing” scenario. In detail, this occurs when Singlife admits a claim for either the Cognitive Care Benefit or the Mental Care Benefit just before your 99th age next birthday. Under those circumstances, you overpaid your insurance policy by over 15 times.

Part 8.3: Cost-to-Benefit Ratio for the Highest Payout (Shortest Period)

In like fashion, if you wish to receive the highest payout from Singlife Dementia Cover, your claims will need to follow a specific order. To begin with, Singlife will need to admit a claim under the Mental Care Benefit for 5 years. After Singlife has paid out the full benefit for the Mental Care Benefit, it will need to admit a claim for the Cognitive Care Benefit. During either period, Singlife will also admit a claim for both the Emotional Resilience Benefit and the Mental Expenses Benefit.

Summing up, you would have paid a total insurance premium of $23,026.25 and received an insurance claim payout of $170k. To this end, the Cost-to-Benefit Ratio is 0.1354.

Part 8.4: Retaining the Financial Risk

Next, let’s consider the case when you choose to retain the financial risk of (up to) $170k on your own. For this purpose, we shall invest $4,605.25 annually into a financial instrument that also generates an effective yield of 4% per annum. Through investing, you will accumulate $14,950.78 within 3 years (i.e. 68 years old); and this amount is similar to Singlife Dementia Cover’s minimum claim payout. As you continue to invest, you will accumulate $175,379.91 when you reach 88 years old; and this amount is similar to the Plan’s maximum claim payout.

By comparison, as I have noted earlier, it takes at least 15 years (i.e. 80 years old) for you to receive the maximum claim payout from the insurance policy. Consequently, you need to evaluate whether the difference in timeframe poses a risk to your financial well-being. Moreover, similar to the earlier analysis, it is also questionable whether you can find a financial instrument that can generate a guaranteed yield of 4% per annum consistently.

Part 9: My Thoughts

As much as I tried to put all these numbers into an objective analysis, it is neither comprehensive nor robust enough to reach an affirmative outcome. In fact, no matter how much data and information I use in my analysis, it is never complete without taking one factor into account; that is, your health. Above all, everyone’s health condition is different and feel differently about their own body. To illustrate, if you have a strong genetic link to dementia, then you may be more emotionally inclined towards purchasing Singlife Dementia Cover. Nevertheless, I hope that this analysis brings about some objectivity to ensure that you don’t purchase an insurance product because of its novelty or promotional campaign.

On the whole, I feel that there will be a few groups of consumer who won’t consider Singlife Dementia Cover as their primary long-term care insurance policy. This is because its coverage may have an overlap with your existing insurance policies.

Part 9.1: Singlife Dementia Cover vs Early Critical Illness Insurance Cover

Firstly, let’s look at the core coverage of Singlife Dementia Cover, which is dementia itself. For this purpose, for Early or Intermediate Dementia, the maximum claim payout that you can receive is $50k (under Mental Care Benefit). In order to receive the maximum claim payout, you must have Early or Intermediate Dementia for 5 years. This is because the insurer pays this benefit on an annual basis, so long as you continue to fulfil the condition for a claim. To clarify, after you recover from (early or intermediate) dementia, the claim payout will stop.

By comparison, if you have an early critical illness insurance policy, then it will likely cover Early or Intermediate Dementia as well. Upon the admission of such a claim, most early critical illness insurance policies will provide a lump sum payout. As a result, such a payout may ease your cash flow better as compared to receiving a smaller amount over half a decade.

Part 9.2: Singlife Dementia Cover vs Major Stage Critical Illness Insurance Cover

Next, for Late Dementia, the maximum claim payout that you can receive from Singlife Dementia Cover is $100k (under Cognitive Care Benefit). In order to receive the maximum claim payout, you must have Late Dementia for 10 years. Similar to the Mental Care Benefit, the insurer pays this benefit on an annual basis so long as you continue to fulfil the condition for a claim.

On the other hand, Late Dementia is one of the Critical Illnesses that is on the LIA Critical Illness Framework 2019. Consequently, most (if not all) of the insurers will cover this medical condition under their critical illness insurance policy. Once again, there is more predictability and assurance in receiving a lump sum payout as opposed to receiving a smaller amount over an entire decade.

Part 9.3: Limitation on how Singlife Dementia Cover’s Payout work

Moreover, if you are looking at getting the maximum claim payout from Singlife Dementia Cover, then you must be diagnosed with Early or Intermediate Dementia for at least 5 years first (i.e. admit a claim under the Mental Care Benefit). This is because, under the Cognitive Care Benefit, there is a clause that states that once Singlife admits a claim for the Cognitive Care Benefit, then the Mental Care Benefit will no longer be claimable. This is unlike a critical illness insurance policy where such a clause usually doesn’t exist.

Part 9.4: Singlife Dementia Cover vs Health Insurance Cover

Next, let’s look at the Emotional Resilience Benefit and the Mental Expenses Benefit. In general, MediShield Life and an integrated shield plan may provide medical reimbursement for some of the listed mental health conditions. Accordingly, you need to evaluate whether the lump sum payout of between $1k to $10k (depending on your chosen benefit amount) is meaningful enough to meet your additional long-term care needs.

Part 9.5: Singlife Dementia Cover vs Other Long-Term Care Insurance

In general, Singlife Dementia Cover is marketed as a long-term care protection plan. As a result, we must also consider the aspect whereby you are unable to perform certain Activities of Daily Living due to Dementia. For this purpose, all Singaporeans and Permanent Residents (30 years old and above) would have CareShield Life, our nation’s severe disability insurance scheme. Additionally, Singlife mandates that you must have an existing Singlife Long-Term Care insurance product before you become eligible to purchase Singlife Dementia Cover. Under those circumstances, you may be adequately covered for long-term care already.

Part 9.6: Getting Insured for Specific Mental Health Conditions

Summing up, you can see that there are many good alternatives that you can consider as opposed to signing up for Singlife Dementia Cover immediately. That being said, you may be concerned with a mental health condition that is not covered by your existing plans, e.g. Bipolar Disorder. If insurance is the only solution that can give you the financial assurance that you need, then you may consider Singlife Dementia Cover. Similarly, if budget is a constraint, then purchasing an insurance policy with a niche cover may be a more affordable option to go for.

Part 10: Final Thoughts

To conclude, I’m of the view that each of us works with a limited set of resources. As a result, I feel that you should spend your limited budget to purchase insurance policies that are essential first. Next, you may look into insurance policies that provide a wider scope of insurance coverage. This is because they are usually able to provide a better Cost-to-Benefit Ratio as compared to a niche product.

Overall, here is how I feel we should approach Singlife Dementia Cover (or any new insurance product). Rather than to focus on the insurance product, you should focus on your needs first. In order to do this, start by reviewing both your existing insurance policies and your finances. Next, conduct an analysis and a projection to determine whether there is any financial risk that you cannot bear on your own. If the probability of occurrence is low and the financial impact is small, then you may wish to retain this risk on your own. On the other hand, if the probability of occurrence is high, or if the financial impact is larger than what you can afford, then you may wish to transfer the risk to another party (such as an insurance company).

Leave a Reply