Over the past few years, I have been studying my spending pattern to determine the best credit card to pair with each expenditure. By and large, I tracked all this information with the hope of figuring out how I could maximise the credit card rewards for my expenditures. At this time, I am satisfied with the credit card deck that I have built to meet my own spending needs.

Similarly, if you are building up your credit card deck, then you may have wondered about the best credit card to use to suit your spending needs. Moreover, after owning a credit card, another question is to figure out how to make full use of that card to earn the most reward. If you have ever thought about these questions, then this post contains a detailed breakdown of how I maximise the credit card rewards in every spend category.

Table of Contents:

- Credit Card Rewards Explained

- My Approach

- Food

- Government Services

- Grocery

- Hospital

- Insurance

- Income Tax

- Internet Service

- Mobile Service

- Mortgage

- Online Shopping

- Subscription

- Transport

- Travel

- Utility

- Contactless Spending (General)

- Miscellaneous

- Tips and Tricks

- Sign Up Promotion

Disclosure: This post on Credit Card contains referral links. Hence, I may receive some money for coffee when you use my referral link for the credit card application. But no, there is no additional cost to you. In fact, you will receive some cash or cash equivalent incentives too! In any case, I will only recommend products or services that meet my needs and expectations.

One Minute Summary:

- The best credit card is the one that you know how to use in a way such that you can maximise the credit card reward every single time.

- If I have to choose one fuss-free credit card to use for all my expenditures, then I will use Citi PremierMiles.

- If I can choose two credit cards to use for most of my expenditure, then I will choose UOB Preferred Platinum Visa and Citi Rewards.

Part 1: Credit Card Rewards Explained

To begin with, let’s go through a quick summary of the three common types of credit card rewards – cashback, miles, and reward points.

Part 1.1: Cashback Explained

Firstly, cashback is the most common type of reward that a credit card can give. For this purpose, the credit card will give a predefined percentage of cashback for your spending. Generally, this cashback will be used to offset your next month’s credit card statement.

Part 1.2: Miles Explained

Secondly, miles are a popular type of reward among travellers. To explain, the credit card will give you a predefined factor of bank miles or points for your spending. After you have accumulated sufficient miles (with the card), you can transfer them over to your preferred airline loyalty programme as airline miles. Thereupon, you may use these air miles to exchange for a flight ticket to your dream destination.

Part 1.3: Reward Points Explained

Finally, rewards credit cards feel like a hybrid between cashback and miles. This is because you can use the reward points to offset your spending or to redeem them for airline miles.

Part 2: My Approach

In general, there are two ways to accumulate your credit card rewards.

Part 2.1: The “One”

Basically, you will disregard the types of transactions and charge all your expenses onto the same card, every single time. Since we will be using one card for all your expenditures, we will prefer to select the most straightforward card with the highest earning rate for credit card rewards. Moreover, we will select a fuss-free card, i.e. no minimum spend, and no earn cap.

With this purpose in mind, I will use Citi PremierMiles. This is because I get to earn 1.2 Citi Miles per dollar spent.

Part 2.2: The “Deck”

As can be seen from “The One”, its drawback is that there are various situations when you can earn more than double the credit card rewards by using a different card. To achieve this, there are two factors to take into account, 1) the type of expenditure (to be exact, the Merchant Category Code); and 2) the available credit card (that is in my deck). With this purpose in mind, the following sections contain a detailed breakdown of how I maximise the credit card rewards in each expenditure category.

Part 3: Food

On the whole, food is one of the most common expenditures that I have every month. For this purpose, we will look at two ways I get my food – either at a physical store or via a food delivery service.

Part 3.1: Purchasing Food at a Physical Store

Firstly, I will order my meals at either a hawker centre, a food court, a fast food restaurant, or a restaurant. For this purpose, this is my preferred order of payment method:

- FairPrice Group app (link to Citi Rewards);

- ShopBack QR (link to Citi Rewards);

- Fave app (link to Citi Rewards);

- Direct Payment (use UOB Preferred Platinum Visa);

- Cash (last resort).

Part 3.1.1: FairPrice Group app

Whenever I visit the Kopitiam at a shopping mall, I will use the FairPrice Group App to pay for my meals. By doing so, I get to save 10% off the final bill. In addition, I will also add Citi Rewards as the credit card in the payment method within the FairPrice Group app. This is because Citi Rewards offers 10X Points for every dollar spent. In time to come, we can convert the Citi reward points into either 2.27% cashback or 4 miles per dollar spent.

Part 3.1.2: ShopBack QR

By and large, ShopBack is currently one of my favourite apps when it comes to making a payment. This is because by adding Citi Rewards as the credit card in the payment method within the ShopBack app, I can earn 10X Points for every dollar spent.

Additionally, ShopBack ties up with certain merchants in a way such that you get to enjoy additional cashback when you patronise the merchant again. At this time, 7% cashback is one of the highest that I have seen. Summing up, the potential to earn close to 10% cashback makes ShopBack my first choice to pay for my meals.

🎁 If you are new to ShopBack, use my referral code A24Pyv to get $5 (when you spend $20 within 180 days of signing up).

Other Credit Cards that I can also use with ShopBack QR: HSBC Revolution (10X Reward Points), UOB Preferred Platinum Visa (UNI$10 per $5 spend), Citi PremierMiles (1.2 Citi Miles)

Part 3.1.3: Fave

Next, many merchants, including hawker stalls accept payment via the Fave app these days. In this situation, I will add Citi Rewards as the credit card in the payment method within the Fave app. Similar to ShopBack, I will earn 10X Points for every dollar spent via the Fave app.

Moreover, Fave may also give 5% cashback to offset the next transaction that I make through its app (for the same merchant). To sum up, I can save up to 7.27% by using the Fave app to pay for my meals.

🎁 If you are new to Fave, use my referral code FAVEZL47 to get $1 off your first purchase (minimum purchase of $20).

Other Credit Cards that I can also use with Fave: HSBC Revolution (10X Reward Points), UOB Preferred Platinum Visa (UNI$10 per $5 spend), Citi PremierMiles (1.2 Citi Miles)

Part 3.1.4: Direct Payment (Credit Card)

In the absence of a QR code, I will use UOB Preferred Platinum Visa via Apple Pay. For every $5 spent, I can earn UNI$10 (equivalent to 4 miles per dollar).

Other Credit Cards that I can also use for Direct Payment (Food): HSBC Revolution (10X Reward Points), Citi PremierMiles (1.2 Citi Miles)

Cards to avoid for Direct Payment (Food): Citi Rewards

Part 3.2: Food Delivery

At this time, Foodpanda is my preferred food delivery service. This is because I can earn 18% cash rebates with the DBS yuu card. Consequently, there is a possibility to make the net cost of my meal cheaper as compared to paying it at the store directly.

Meanwhile, if I use Deliveroo or Grab Food, then I will use Citi Rewards to earn 10X Points.

Other Credit Cards that I can also use for Food Delivery: UOB Preferred Platinum Visa (UNI$10 per $5 spend)

Cards to avoid for Food Delivery: HSBC Revolution (1X Reward Point)

Part 4: Government Services

Part 4.1: Immigration & Checkpoints Authority (“ICA”)

Most credit cards do not issue rewards for Government Services (MCC 9000 – 9999). To overcome this limitation, I will use the Chocolate Finance Visa to earn 1 Max Mile per $1 spend.

🎁 If you are new to Chocolate Finance, use my referral code to open your Chocolate Finance account today.

Cards to avoid for ICA: Citi PremierMiles, Citi Rewards, DBS Yuu, HSBC Revolution, UOB Preferred Platinum Visa

Part 4.2: Singapore Post

Similarly, for Singapore Post, I will also use the Chocolate Finance Visa.

Cards to avoid for Singapore Post: Citi PremierMiles, Citi Rewards, DBS Yuu, HSBC Revolution, UOB Preferred Platinum Visa

Part 5: Grocery

At present, I do most of my grocery shopping at either Giant or Cold Storage. As a result, DBS yuu is the best card in this category. This is because at the base level, I can earn 5% cash rebates for my grocery-related expenditures. Additionally, if I spend $800 in a calendar month at 4 different participating merchants, then I will earn 18% cash rebates instead. As a result, this is certainly one of the highest cash rebates that a credit card offers.

Despite that, there are also occasions when I purchase groceries from NTUC FairPrice. In this situation, I will use Citi Rewards with the FairPrice Group app to earn 10X Points.

Other Credit Cards that I can also use for Grocery: UOB Preferred Platinum Visa (UNI$10 per $5 spend), Citi PremierMiles (1.2 Citi Miles)

Cards to avoid for Grocery: HSBC Revolution

Part 6: Hospital

Part 6.1: Public Hospitals

For public hospitals, I will use the Chocolate Finance Visa debit card to earn 1 Max Mile per $1 spend.

Cards to avoid for Public Hospitals: Citi PremierMiles, Citi Rewards, DBS Yuu, HSBC Revolution, UOB Preferred Platinum Visa

Part 6.2: Private Hospitals

For private hospitals, I will use UOB Preferred Platinum Visa as there is a possibility of earning UNI$10 per $5 spend.

Other Credit Cards that I can also use for Private Hospitals: Chocolate Finance Visa debit (1 Max Mile)

Part 7: Insurance

Most credit cards exclude the ability to earn credit card rewards for paying insurance premiums. To overcome this limitation, you will need to rely on a third-party service provider. By paying a one-time processing fee to the service provider, you will be able to earn credit card rewards for the otherwise excluded transaction. For this purpose, I will use Citi PremierMiles for the transaction.

If you wish to learn more about the various ways to pay your insurance premium and how to earn credit card rewards at the same time, then I will suggest you read this post: Best Way to pay Insurance Premium Singapore

Other Credit Cards that I can also use for Insurance: Chocolate Finance Visa debit (1 Max Mile)

Part 8: Income Tax

Similar to the case for insurance premiums, you will also need to rely on a third-party service provider to pay your income tax bill. For this purpose, I will use Citi PremierMiles for the transaction.

Other Credit Cards that I can also use for Income Tax: Chocolate Finance Visa debit (1 Max Mile)

Part 9: Internet Service

At present, I chose StarHub as my home’s internet service provider. On this occasion, I will pay the bill directly via StarHub’s portal with Citi Rewards. Thereupon, I would earn 10X Points for the transaction.

Other Credit Cards that I can also use to pay for Internet Service: HSBC Revolution (10X Reward Points)

Part 10: Mobile Service

For mobile service, I am using Giga’s 10GB plan at this time. I have written a review in detail on its pros and cons and how it fits into my needs well. To this end, I will use Citi Rewards as it gives 10X Points. It is important to realise that you will not get 10X Points if you set up the card for a recurring transaction. Instead, you will need to make a manual payment through Giga’s app – purchase a $10 gigaBucks pack to offset your next month’s bill.

🎁 If you are new to Giga, use my referral code er4cri to enjoy a $2 discount during your sign-up.

Other Credit Cards that I can also use to pay for Mobile Service: HSBC Revolution (10X Reward Points)

Part 11: Mortgage

Previously, I took a housing loan from the Housing Development Board (HDB) for my home. Consequently, I need to repay the loan instalment every month. To this end, there are two parts to how I earn credit card rewards for repaying my mortgage loan. To begin with, let’s learn about the third-party platform that I use for this purpose – CardUp.

In summary, CardUp is a third-party platform that allows you to use your credit card to perform various types of payment. For example, it can be to pay rent, an invoice, insurance premium, and even income tax. Through CardUp, you get credit card rewards for the otherwise excluded merchant category codes (MCC).

For this to work, I would need to submit the relevant mortgage-related documents to CardUp. Thereafter, I would use Citi PremierMiles.

After making the payment through CardUp, I would receive the funds in my bank account in time to come. Thereupon, I will simply wait for the bank to debit the repayment amount from my account on the last day of the month.

🎁 If you are new to CardUp, then consider signing up using my referral code, ZHELIANGP464. In effect, you get a $30 promo code for your first transaction. Thereupon, this will cover the platform fee for transactions of up to $1,153.

Part 12: Online Shopping

By and large, there are two types of merchants when you shop online. Firstly, the merchant is a local online store and charges for its goods and services in our local Singapore currency, SGD. For example, if you shop at Lazada, then the cost of the item will be in SGD. Secondly, the merchant is an overseas store and charges for its goods and services in its foreign currency. To illustrate, if you shop at Walmart, then the cost of the item will be in USD.

Part 12.1: Online Shopping – Local Spend

Summing up, for online shopping in SGD, I will use either Citi Rewards or HSBC Revolution. This is because either card will give 10X Reward Points for the transaction.

Part 12.2: Online Shopping – Foreign Spend

In contrast, for online shopping in a foreign currency, I will use Instarem’s amaze card (that I have paired with Citi Rewards). This is because the amaze card tends to give a more favourable exchange rate as compared to using a credit card directly. To this end, I will be able to earn 10X Points with Citi Rewards. Additionally, I will also earn 0.5 InstaPoint from the amaze card.

🎁 If you are new to Instarem, use my referral code qvt7lE to get 200 InstaPoints (worth $2.50) when you spend at least $10 with your amaze card.

Other Credit Cards that I can also use for Online Shopping: HSBC Revolution (10X Reward Points), UOB Preferred Platinum Visa (UNI$10 per $5 spend)

Part 13: Subscription

Part 13.1: Adobe Creative Cloud (MCC 5734)

As a Wedding Photographer at Le Vows Wedding Production, I use Adobe Lightroom and Photoshop frequently. To that end, I subscribe to Adobe Creative Cloud and pay for its subscription on an annual basis. For this purpose, I will use either Citi Rewards or HSBC Revolution. This is because either card will give 10X Reward Points for the transaction.

Part 13.2: Apple iCloud+

As an Apple user, I subscribe to iCloud+. At this time, I use the combination of the amaze card with Citi Rewards. This is because the latter will give 10X Points whenever Apple renews my iCloud+ plan. Moreover, the amaze card helps me to avoid the Dynamic Currency Conversion (DCC) fee that credit cards like to charge.

Part 14: Transport

Part 14.1: Public Transport

For public transport, I will use DBS yuu to earn up to 18% cash rebates every month.

Other Credit Cards that I can also use for Public Transport: UOB Preferred Platinum Visa (UNI$10 per $5 spend)

Cards to avoid for Public Transport: Citi PremierMiles, Citi Rewards, HSBC Revolution

Part 14.2: Private Hire

For the private hire service, I would prefer to book a ride via Gojek. This is because I can earn 5% cash rebates (and up to 18% cash rebates) with DBS yuu. Alternatively, I can also use Citi Rewards to earn 10X Points.

For rides with Grab, I will use Citi Rewards (10X Points).

Finally, for flag-down taxis, I will cry and pay cash to avoid paying a 10% administrative fee.

Other Credit Cards that I can also use for Private Hire: HBSC Revolution (10X Reward Points, between 1 July 2025 to 28 February 2026)

Part 15: Travel

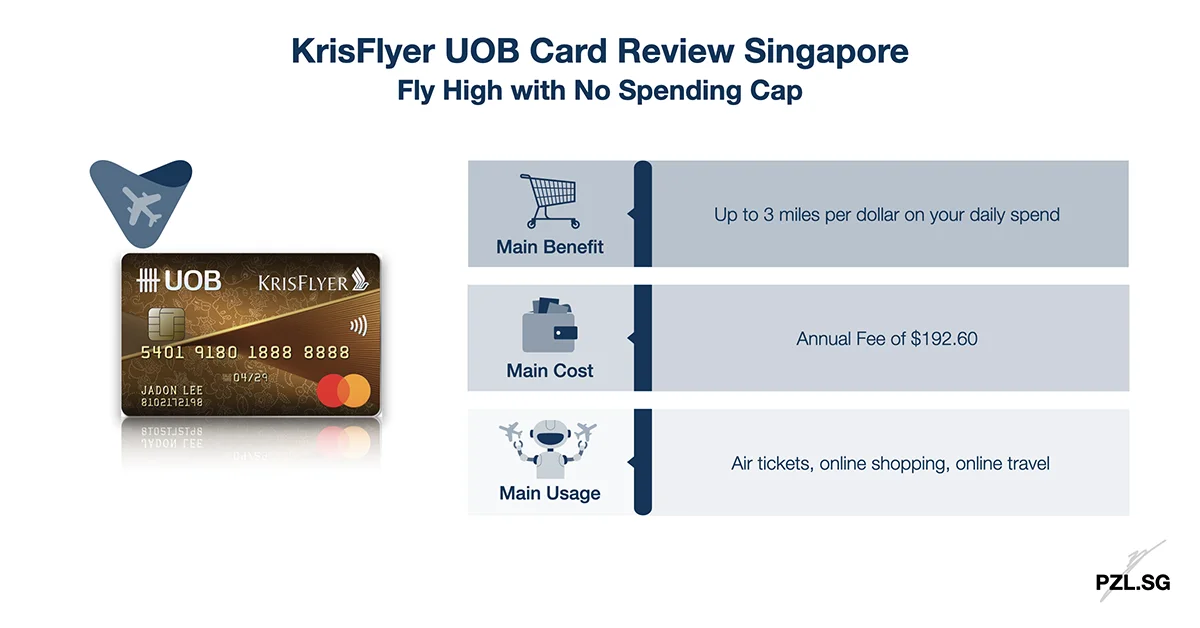

Part 15.1: Air Ticket (MCC 3000 to 3350, 4511)

At present, I will use HSBC Revolution to purchase a flight ticket. This is because I can still earn 10X Reward Points between 1 July 2025 and 28 February 2026. Thereafter, HSBC will no longer give 9X Bonus Reward Points for travel-related merchants. With this in mind, this is a “use it while I can” card for now.

Other Credit Cards that I can also use for Air Ticket: UOB Lady’s (UNI$10 per $5 spend by selecting Travel category), Citi PremierMiles (1.2 Citi Miles)

Cards to avoid for Air Ticket: Citi Rewards, UOB Preferred Platinum Visa

Part 15.2: Airbnb (MCC 7011)

For Airbnb, I will use HSBC Revolution to earn 10X Reward Points.

Other Credit Cards that I can also use for Airbnb: UOB Lady’s (UNI$10 per $5 spend by selecting Travel category), Citi PremierMiles (1.2 Citi Miles)

Cards to avoid for Airbnb: Citi Rewards, UOB Preferred Platinum Visa

Part 15.3: Hotel (MCC 3501 to 3999, 7011)

For bookings made directly with the hotel, I will use HSBC Revolution to earn 10X Reward Points.

Other Credit Cards that I can also use for Hotel: UOB Lady’s (UNI$10 per $5 spend by selecting Travel category), UOB Preferred Platinum Visa (UNI$10 per $5 spend), Citi PremierMiles (1.2 Citi Miles)

Part 15.4: Online Travel Agent (MCC 4722)

If I am booking and paying for the hotel through an online travel agent like Agoda, Kaligo, or Trip.com, the Merchant Category Code is 4722. In this case, I will use Citi PremierMiles to make my hotel booking through Kaligo. This is because Citibank has a promotion where I can earn an additional 8.8 Citi Miles for every dollar spent at Kaligo. To sum up, I can earn 1.2 Citi Miles + 8.8 Citi Miles = 10 Citi Miles for this transaction.

However, there may be situations when Kaligo does not provide the best hotel rates. In this situation, I will use Citi PremierMiles to make my hotel booking through Agoda. To point out, Citibank also has a promotion where I can earn a bonus of 5 Citi Miles for every dollar spent on hotel bookings through Agoda. Summing up, I can earn 1.2 Citi Miles + 5 Citi Miles = 6.2 Citi Miles (per dollar spent) for this transaction. If this transaction is categorised as an overseas spend, then I can earn 2 Citi Miles + 5 Citi Miles = 7 Citi Miles (per dollar spent).

Other Credit Cards that I can also use for Online Travel Agent: UOB Lady’s (UNI$10 per $5 spend by selecting Travel category)

Cards to avoid for Online Travel Agent: Citi Rewards, HSBC Revolution, UOB Preferred Platinum Visa

Part 15.5: Overseas Spending

Like online shopping in a foreign currency, I will use Instarem’s amaze card. After I pair amaze card with Citi Rewards, the latter will give me 10X Points for my overseas spending. Additionally, I will also earn 0.5 InstaPoint from the amaze card.

🎁 If you are new to Instarem, use my referral code qvt7lE to get 200 InstaPoints (worth $2.50) when you spend at least $10 with your amaze card.

Other Credit Cards that I can also use for Overseas Spending: UOB Preferred Platinum Visa (UNI$10 per $5 spend), Citi PremierMiles (1.2 Citi Miles)

Part 16: Utility

Part 16.1: SP Services (MCC 4900)

By and large, SP Services is probably the default utility provider for many households. For this purpose, I will use Chocolate Finance Visa to earn 1 Max Mile.

🎁 If you are new to Chocolate Finance, use my referral code to open your Chocolate Finance account today.

Other Credit Cards that you can also use for SP Services: UOB Absolute Cashback (0.3% cashback)

Part 16.2: Senoko Energy

On the other hand, I purchase my home’s electricity through Senoko Energy. This is because of its lower fixed rate as compared to the prevailing electricity tariff. If you are keen to learn more about Senoko Energy and why I chose it, then you may read my full review here. Besides, you may also check out the latest comparison that I have done to help you determine which is the cheapest open electricity market retailer to select for your home. To this end, I use Chocolate Finance Visa to earn 1 Max Mile.

🎁 If you are new to Senoko Energy, use my referral code, LFSBFXNC and you will enjoy a $20 bill rebate for any electricity price plans that you sign up with Senoko Energy.

Other Credit Cards that you can also use for Senoko Energy: UOB Absolute Cashback (0.3% cashback)

Part 17: Contactless Spending (General)

If you have survived this post so far, then I wish to congratulate you. For the most part, this is probably one of the longest blog posts that I have written. Now, if I haven’t identified or categorised any other spending that I have, then it will be either contactless spending or ad-hoc miscellaneous spending.

Part 17.1: Mobile Contactless Spending that is less than $600

For contactless spending that is less than $600, the first choice will be to use UOB Preferred Platinum Visa.

Part 17.2: Contactless Spending that is more than $600

If the transaction is more than $600, then I will use Citi PremierMiles. This is because there is no earning cap on the credit card rewards.

Part 18: Miscellaneous

Similar to contactless spending, I will use either UOB Preferred Platinum Visa or Citi PremierMiles for any ad-hoc spending that I may have.

Part 19: Tips and Tricks

On the whole, you may be able to spot a pattern in how I maximise the credit card rewards in my credit card deck. That is, I tend to sign up and use credit cards that can maximise the credit card rewards in multiple spending categories. For example, I’m able to use Citi Rewards for food, internet service, online shopping, and much more. Summing up, this strategy allows me to accumulate more points within the same credit card. In time to come, I can convert more points into miles by paying just a single transfer fee. Furthermore, I reduce the risk of acquiring orphan miles (which usually occurs if I spread my spending across too many credit cards).

Now, if you wish to maximise your credit card reward in the same way as I do, here is what I would suggest for you to do. Firstly, track and list all your expenditures over a few months (I did mine for a couple of years). Next, categorise these expenditures and rank these categories according to how much you spend. By and large, you should consider credit cards that earn the highest reward for the amount that you spend the most each month.

Part 20: Sign Up Promotion

Finally, if you intend to sign up for any of the above-mentioned credit cards, then you may consider using my referral links (a collaboration with SingSaver). After fulfilling the sign-up terms and conditions, you will receive additional cash, gifts, and rewards. This is certainly one of the best deals ever!

First Published: 6 August 2021

Last Updated: 3 October 2025

Leave a Reply